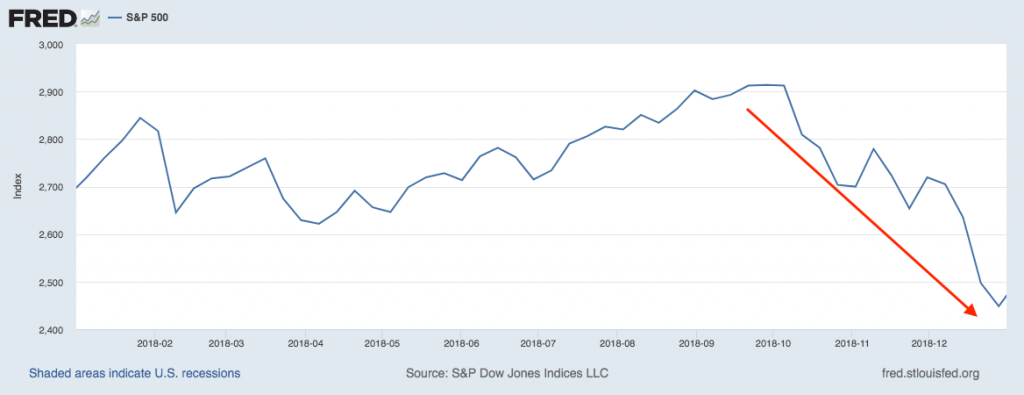

Many readers remember the sudden and sharp S&P 500 declines around this time last year. 2018’s fourth quarter was harsh, to say the least. From the S&P 500’s highs in early October through Christmas Eve, the index dipped into bear market territory with a near perfect -20% decline.1 Technical market watchers would rightfully label this decline a bear market, but throughout history the dangerous bear markets have tended to be the ones known for size and duration. Since last year’s Q4 ‘bear market’ only lasted a day, it likely won’t be remembered in the annals of stock market history.

The S&P 500 in 2018: A Sharp Q4 Correction

Source: Federal Reserve Bank of St. Louis2

In last year’s fourth quarter, trade uncertainty was rising, global economic growth was positive but slightly decelerating, and the Federal Reserve was raising interest rates. In the current quarter (Q4 2019), global growth remains in the same middling decelerating pattern, but the Fed has lowered interest rates three times and “Phase 1” of a potential trade deal is driving some optimism in the markets. In other words, conditions are quite different in 2019 than they were in 2018, and the S&P 500 has been trending modestly higher.

——————————————————————

Don’t Let Headlines Get in the Way of Your Investments!

Newsworthy headlines have a tendency of overshadowing truly

important events. So instead of getting caught up in the headlines, focus on

hard data and economic indicators that could drive the market. To help you do this, we are offering

all readers a first-look into our just-released December 2019 Stock Market

Outlook report.

This 22-page report contains some of our key forecasts to consider in 2019:

- Stock market returns expectations for 2019 and 2020?

- Forecast for the S&P

- What of slowing foreign growth?

- Can the U.S. stock market rally stick?

- Which sectors are hot and which are not?

- What industries within those sectors most merit your attention?

- Odds of recession

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released December 2019 Stock Market Outlook3

——————————————————————

The S&P 500 YTD 2019 Through October 31: A Smooth Start to Q4 (So Far)

Source: Federal Reserve Bank of St. Louis4

To be fair, however, we now have an environment where the global manufacturing sector is in recession, business investment is softening, and corporate earnings are on pace for their third straight quarter of declines. So, what has me convinced that the S&P 500 will finish 2019 in solidly positive territory? I’ll give you three reasons.

Reason #1: Positive Signs are Being Ignored

Regular readers know my opinion that markets love to climb the “wall of worry.” The wall of worry forms when investors get so latched onto the recession narrative that pessimism pervades the airwaves, and people prefer to cling to negative news while ignoring positive developments.

We see this happening quite a bit today, with significant positive news being overlooked, such as:

- The yield curve turned positive with few people noticing

- Solid and consistent gains in the labor markets continue apace

- Consumer spending continues to grow at a healthy clip

- The all-important ISM non-manufacturing index continues posting readings in solidly expansionary territory

- And so on down the line

Instead of the narrative being that the U.S. economy is charting a modest, but healthy growth path in-line with a long-term trend of 2%, the narrative is instead focused on a matter of when, not if, the U.S. will enter a recession. This disconnect between sentiment and reality is bullish, in my view.

Reason #2: Recession Risks are Already Deeply Discounted in the Markets

In a recent Barron’s poll, 27% of money managers said they had a bullish outlook on stocks, compared to a year ago when 56% of managers were bullish.5 Many managers – and investors – have shifted into defensive positions over the past year, with historically defensive sectors like Utilities and Consumer Staples leading the charge of market gains in 2019. These sectors now look fairly expensive relative to cyclicals, in my view, which I believe creates an opening for mean reversion.

Reason #3: Trade Uncertainty Will Start to Lift, Bringing Sentiment with It

This week has brought with it several developments on the trade war front, with China and the U.S. appearing to agree that tariffs will be reduced or even phased out as part of “Phase 1” of the trade deal. Part of the reason business investment – and arguably manufacturing – have been softening is because of uncertainty surrounding the trade war. I believe that as we inch closer to clarity and the prospects of early innings of a deal, some of this uncertainty will lift and we could see a bounce-back in fixed investment and factory activity.

Bottom Line for Investors

Since 1926, the S&P 500 has entered the fourth quarter with double-digit gains on 42 occasions. In 35 of those years, the index continued its ascent through year-end, posting an average gain of +4.5%. In the post-World War II era, the S&P 500 has averaged a +3.8% return in the fourth quarter.6

These metrics are reassuring, and history can be useful in helping us assign probabilities to outcomes. But my real point in sharing those metrics is to demonstrate that last year’s dreadful Q4 was an anomaly in history. At the end of the day, stocks have gone up more than they have gone down, and I’ve got three reasons to believe this year’s Q4 will fit this historical pattern.

The takeaway for investors: remember to look past the headlines and focus on the fundamentals.

To help you do this, I invite you to download our Just-Released December 2019 Stock Market Outlook Report >>

This Special Report is packed with newly revised predictions for the remainder of 2019 and 2020 that can help you base your next investment move on hard data. For example, you’ll discover Zacks’ view on:

- Stock market returns expectations for 2019 and 2020?

- Forecast for the S&P

- What of slowing foreign growth?

- Can the U.S. stock market rally stick?

- Which sectors are hot and which are not?

- What industries within those sectors most merit your attention?

- Odds of recession

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!7

Disclosure

2 S&P Dow Jones Indices LLC, S&P 500 [SP500], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/SP500, November 11, 2019.

3 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

4 S&P Dow Jones Indices LLC, S&P 500 [SP500], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/SP500, November 11, 2019.

5 Barron’s, October 26, 2019. https://www.barrons.com/topics/big-money-poll

6 Silverlight Asset Management, LLC. October 2019. https://www.silverlightinvest.com/blog/sp-500-should-hang-there-through-fourth-quarter

7 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.