The S&P 500 notched a stout +7.2% gain in the third quarter, in spite of bubbling trade disputes, rising interest rates, and concerns about currency and debt in the Emerging Markets. Q3 marked the S&P 500’s best quarterly performance in nearly five years (Q4 2013).1

In my view, the bullish outlook for stocks – and U.S. stocks in particular – remains the base case. But as optimism builds in the markets with rising stock prices and a strong economy, vulnerabilities also tend to become more viable, in my view.

It’s been my experience that big declines in the market often come just as investors fully and confidently embrace the ‘booming’ economy and the soaring stock market. It’s an unfortunate reality, but just as things start to feel really good on all fronts, that’s precisely the time when we should be looking over our shoulders for the bear.

With that in mind, this week I want to take a look at a few risks that are circling the markets today, what I deem a ‘triple threat’ to rising stock prices.

______________________________________________________________________________________________________________

How Will You Prepare for a Market Downturn?

This is now the longest bull market in American history, and many investors are wondering how much longer it could last. The S&P 500 was up +7.2% in the 3rd quarter alone. Is the end of the bull market approaching?

See what Zacks predicts for the remainder of the year with our just-released Stock Market Outlook Report. This 22-page report contains some of our key forecasts to consider:

- S&P500 Earnings Outlooks

- What of U.S. GDP growth?

- Small-cap and large-cap outlook

- Which sectors are hot and which are not?

- What industries within those sectors most merit your attention?

- And much more.

IT’S FREE. Download the Just-Released Stock Market Outlook2 >>

______________________________________________________________________________________________________________

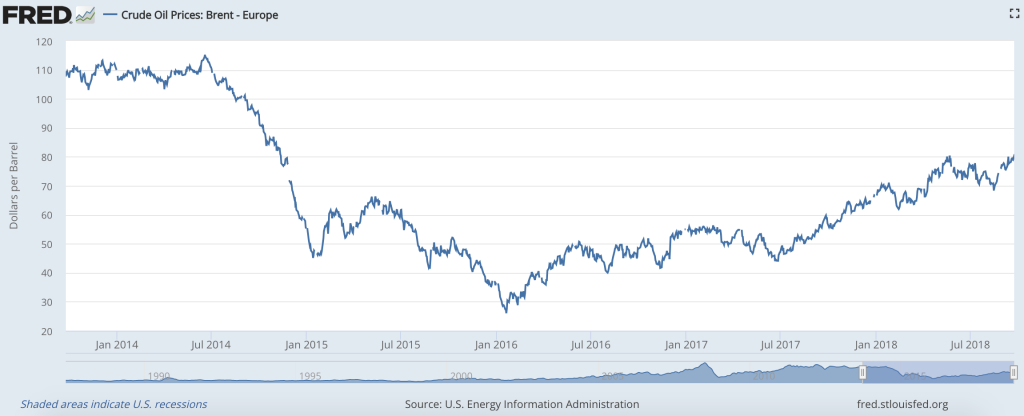

Threat #1: Rising Crude Oil Prices

Rising oil prices have just started to gain attention in the media narrative, but still remain off the radar screens of many investors. Perhaps it’s time to pay a bit more attention – Brent Crude oil prices crossed into multi-year high territory last week, and traders seem to be betting that U.S. sanctions on Iran and lower output from embattled countries like Venezuela and Libya will lead to supply shortages. The question of whether Saudi Arabia can fill the supply gaps seems uncertain at best, and is perhaps the catalyst for global oil prices being up some 25% on the year3:

Source: Federal Reserve Bank of St. Louis

Meanwhile, demand has remained fairly firm as global economic growth has continued apace, in spite of the supposed negative impacts from tariffs and trade disputes. That leaves prices vulnerable to the upside, in my view, should further supply disruptions take hold.4

Threat #2: Tightening Monetary Policy

The Federal Reserve raised interest rates in their September meeting and most market participants expect another in December. While I wouldn’t necessarily refer to this tightening as fully hawkish given the Fed’s gradual and smooth approach, it certainly moves in the direction of tightening financial conditions which could result in more saving, less housing activity, and perhaps a plateauing of fixed private investment on the corporate side. Taken together, these are the types of macro events that can put the brakes on fast growth.

As interest rates rise, investors should pay attention to rotation trends amongst asset classes. Already, we’ve seen rate-sensitive sectors like Consumer Staples and Utilities underperforming, while government bonds have done better.5

The question at the center of tightening monetary policy is “will the Fed go too fast,” which we’ll have to answer almost surely in the coming year or next.

Threat #3: Too Much Optimism

U.S. consumer confidence is at an 18-year high, the stock market is hovering around all-time highs, and corporate profits have been soaring all year.6 There are plenty of reasons for optimism about the economy and equities markets.

But that’s also what worries me. A tell-tale sign of a frothy market, in my view, are high and rising stock prices accompanied by enthusiastic and confident investors. I like it more when the “wall of worry” is present in the media narrative, which is largely missing today save for tariffs.

A case-in-point was made earlier this week, when University of Florida professor Jay Ritter pointed out that roughly 83% of U.S.-listed IPOs in 2018 (year-to-date) lost money in the 12 months leading up to their offering. That’s higher than the 81% of unprofitable companies issuing IPOs in 2000, and is actually the highest on record going back to 1980. Investors are getting too cozy with risk, in my view. “Buyer beware.” 7

Bottom Line for Investors

I don’t worry so much today about threats #1 and #2, because those are two stories that are fairly widely discussed and that the market (I believe) has largely priced-in already. A shock in oil prices from an unexpected supply disruption and a surge in interest rates unexpectedly would likely alter my view, but I don’t see either as likely.

Optimism worries me the most. Corporate earnings are strong and the economy is chugging along nicely. Valuations have also stayed in check due to some sideways movement in the market while earnings climbed. But as optimism grows alongside rising stock prices, the risk of paying too high a premium to own risk assets becomes more acute. Investors start to ignore risk because they think the economy is bulletproof and stocks are the only place to be. Optimism becomes euphoria, and as the famed investor John Templeton once said, “bull markets die on euphoria.”8

Curious what produces 2018 optimism? Get this info and much more with our Just-released Stock Market Outlook report.

This 22-page report contains some of our key forecasts to consider

- What produces U.S. optimism?

- S&P500 Earnings Outlooks

- What of U.S. GDP growth?

- Small-cap and large-cap outlook in 2018

- Which sectors are hot and which are not?

- What industries within those sectors most merit your attention?

- And much more.

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook Report at any time and for any reason at its discretion.

3 The Wall Street Journal. October 1, 2018, https://www.wsj.com/articles/crude-extends-gains-as-supply-risks-linger-1538388939

4 The Wall Street Journal. October 1, 2018, https://www.wsj.com/articles/crude-extends-gains-as-supply-risks-linger-1538388939

5 The Wall Street Journal. September 30, 2018, https://www.wsj.com/articles/u-s-stocks-open-fourth-quarter-near-record-highs-but-face-hurdles-1538316001?mod=djem10point

6 Reuters. August 28, 2018. https://www.reuters.com/article/us-usa-economy/u-s-consumer-confidence-races-to-near-18-year-high-idUSKCN1LD201

7 The Wall Street Journal. October 1, 2018, https://www.wsj.com/articles/red-ink-floods-ipo-market-1538388000?mod=djem10point

8 CNBC. December 13, 2017. https://www.cnbc.com/2017/12/13/cramer-bull-markets-die-on-euphoria-and-were-one-step-away.html

9 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook Report at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.