Weekly credit and debit card spending at major U.S. retailers – Target, Walmart, Amazon, Best Buy, and Kohls – has been tracking higher since the beginning of the year. Steady spending comes in spite of record job losses and a pandemic that remains a public health and economic risk. Challenging times abound, but U.S. consumers remain resilient.

There have been a few key factors supporting spending. For one, the economic recession did not touch all sectors and industries. While some areas of the economy experienced sharp decline in activity (retail, hospitality, airlines, food services), others thrived (technology, consumer discretionary, home goods, consumer staples). The federal government was quick to respond to workers and families in the former category, and the $600/week additional unemployment benefit and stimulus checks proved a robust safety net. Personal incomes and the savings rate actually went up over the summer.1

To be fair, those stimulus tailwinds are fading, and economic growth momentum appears likely to slow down until more stimulus is passed and/or a vaccine is widely distributed. The timing of either outcome remains uncertain.

Even still, I believe the U.S. consumer remains an under-appreciated positive, and I think spending will hold up in the coming quarters better than most expect. Here are three reasons why.

_________________________________________________________________________

Hard Data & Economic Indicators You Should Keep an Eye On!

In addition to consumer spending data, there are additional data points and economic indicators that you should pay attention to in this turbulent time. To help you focus on the hard data and other factors that could impact your investments, I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- The economic effects of the COVID-19 pandemic

- U.S. returns expectations for 2020

- Background on the U.S. fiscal stimulus program

- Why you should be careful in determining what S&P 500 data to use

- Zacks Rank S&P 500 Sector Picks

- Status of global energy markets

- What produces 2020 optimism?

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released November 2020 Stock Market Outlook2

_________________________________________________________________________

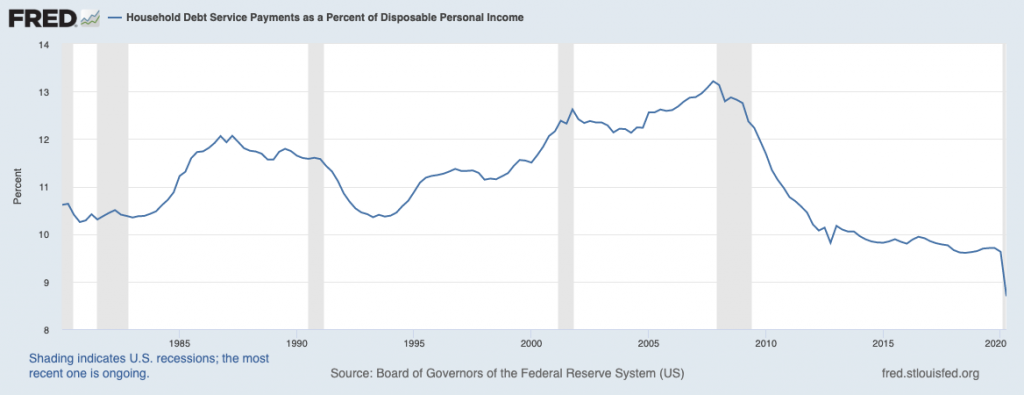

1. Households, Surprisingly, are in a Reasonably Strong Financial Position

One key measure for how well households are holding up is to look at debt payments as a percent of disposable personal income, which are now at a 30+ year low.

Household Debt Payments as a Percent of Income are Falling – A Good Sign

Source: Federal Reserve Bank of St. Louis3

Low interest rates are part of the equation. Many households have been able to refinance existing debt to make it more affordable, while others used the economic growth of the last decade to trim debt on balance sheets. While only about 50% of Americans own stocks, the market’s surge in the last bull market also boosted net worth and improved many households’ financial positions going into the pandemic. An economic rebound in the coming years – which I see as highly likely – should only add to this financial position and drive spending in the process.

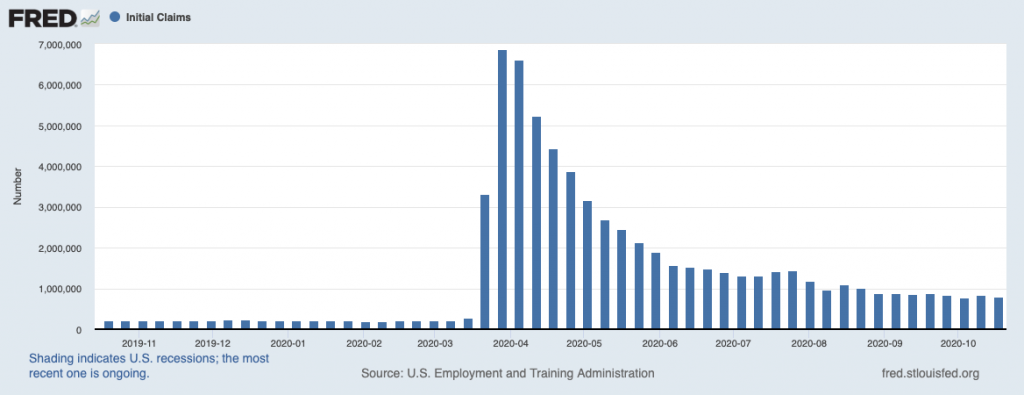

2. Steady Rebound in the Labor Markets

Early in the pandemic, some economists were predicting an unemployment rate north of 20%, but the labor market proved more resilient than expected. After reaching a peak of 14.7% in June, the unemployment rate fell back to 7.9% in September. Initial jobless claims – a key indicator of labor market health and improvement – has also been steadily declining, suggesting the number of layoffs is easing:

Source: Federal Reserve Bank of St. Louis4

I expect the jobs market to continue along this path, with modest improvements through Q1 2021. But I am also in the camp of seeing a surge in hiring once the pandemic risk fades, which I believe is likely to arrive sometime early-to-mid next year. Improvements to the job markets should correspond fairly tightly to gains in spending.

3. Downstream Effects of Housing Market Strength

Sales of previously-owned homes rose to a 14-year high in September, continuing a bullish trend for housing that has persisted all year. Interestingly, much of the new growth is being driven by millennials, who previously had been reluctant to enter the housing market as family formation lagged and as they favored renting. For the first time, millennials accounted for over 50% of new home loans. Many are migrating out of cities and into the suburbs—with more space for home offices.

Downstream effects of the housing boom have been evident in consumer spending on furniture, appliances, and home improvement, which has outperformed spending across most other sectors – a trend I expect to continue.

Bottom Line for Investors

Year-to-date, Consumer Discretionary stocks are up +23.4%, while Technology stocks are up +28.7%. No other sector has posted a return greater than +9% for the year, and the S&P 500 is up +5.6% (through September 30). The U.S. consumer remains resilient.

Gains in Consumer Discretionary have largely been led by e-commerce companies, but we have also seen marked strength in home improvement, home goods, electronics, general merchandise retailers, and home builders. With more economic growth ahead (in my view), slow and steady improvements to the labor market, and more fiscal stimulus in the pipeline, I’m staying bullish on the U.S. consumer.

To help you focus confidently on hard data and

key economic indicators that can help guide your investments throughout the

rest of this year and into 2021, I am offering all readers our Just-Released

November 2020 Stock Market Outlook Report.

This report looks at several factors that are

producing optimism right now and contains some of our key forecasts to consider

such as:

- A look at potential Covid-19 vaccines

- What produces 2021 optimism?

- What of U.S. GDP growth?

- What should you think about Covid-19 era jobs data?

- An update on U.S. fiscal stimulus

- Zacks Rank S&P 500 sector picks

- International update on key global regions

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Fred Economic Data. October 5, 2020. https://fred.stlouisfed.org/series/ICSA#0

4 Fred Economic Data. October 22, 2020. https://fred.stlouisfed.org/series/ICSA#0

5 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.