There is an interesting dynamic happening in the current environment, in my view: economic risks are falling, while market risks are rising. The two usually move in tandem.

Within the context of economic risks, I think we’re in an environment where risks are falling. I see many economic fundamentals pointing to “green shoots” and improving growth conditions, but below I’ll detail three largely underappreciated factors driving optimism.

1. The Job Market

The first is the jobs market1, which I believe could be substantially stronger than many currently believe. In the Federal Reserve’s recently published Beige Book – which is based on surveys from major cities – I noticed a common theme: employers across the country are reporting shortages of workers, and many are desperate to hire.

__________________________________________________________________________

Manage Rising Market Risks by Focusing on These Key Data Points Today!

With rising market risks and uncertainties in the market, it is essential to stay data-driven! To help you stay focused on key data points and fundamentals that that could impact your investments in the long term, I am offering all readers an exclusive look at our May Stock Market Outlook Report. This report contains some of our key forecasts to consider such as:

- Zacks Rank S&P 500 Sector Picks

- Economic expectations for the rest of the year

- Zacks April and May view on equity markets

- The Impact of Covid-19 vaccine

- U.S. returns expectations for 2021

- What produces 2021 optimism?

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released May 2021 Stock Market Outlook2

__________________________________________________________________________

The areas of the economy with the most acute shortages are part of the ‘reopening trade’, i.e., companies and industries that stand to benefit most from loosened and eventually removed restrictions. Think restaurant employees, drivers, child care workers, service industry jobs, and even jobs in information technology.

The labor force is estimated to be five million people smaller than it was before the pandemic, which gives the impression that the labor market is badly bruised. But it is also true that many people dropped out of the labor force for temporary reasons – people fearful of catching and spreading the virus, and/or those who are content living on expanded unemployment benefits. Those reasons may fade soon, and I think most people who want a job today can find one.

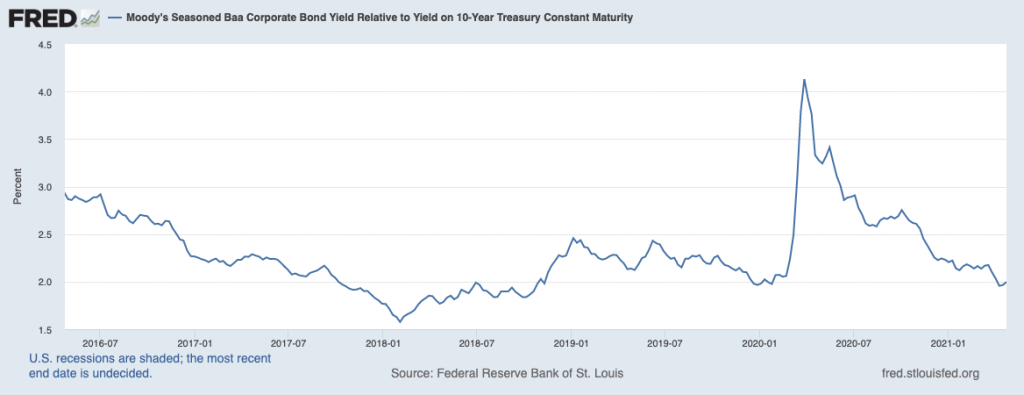

2. Corporate Bond Markets

Another economic fundamental pointing3 to falling risks can be found in the corporate bond markets. The spread between speculative-grade, high yield corporate bonds and the 10-year U.S. Treasury bond has fallen to multi-year lows, as seen in the chart below:

Indeed, the yields on low-rated corporate bonds sunk to a record low of 3.89% in February, indicating that companies can borrow cheaply in the current environment. Investors are the ones doing the lending, which tells us the market is not demanding much compensation for the level of perceived risk. Many would say this is a sign that investors are starved for yield, which I believe is true in part. But the other side of the story is investors may just be very confident in their outlook for the economy and see further signs of strength and improvement.

3. New Business Formation

A final indicator5 underscoring falling economic risks is new business formation. The pandemic devastated many businesses, no doubt. But the tides are turning – applications for new businesses hit nearly 1.4 million in Q1 2021, which marks the second-highest quarterly total in over 15 years. Applications for businesses that could employ multiple workers also approached their highest quarterly tally, indicating that entrepreneurs have been emboldened by what they see as an opportunity for new growth. In my view, it’s a clear sign the U.S. economy is pushing ahead, with innovators and new growth opportunities forming in the wake of a major recession.

Bottom Line for Investors

I’ve made the point that economic risks are falling. But what about market risks being on the rise? In my view, it depends on where you’re invested. I’m seeing a lot of froth in particular asset classes and some individual stocks, but I think an investor’s risk is tied to his/her portfolio exposure. Many investors are abandoning long-term, diversified approaches in favor of chasing ‘hot’ asset classes or stocks. That’s bad news, in my view.

At Zacks Investment Management, in addition to the qualitative screening of the fundamental characteristics of companies we invest in, we analyze their correlation with our existing portfolio and with the overall market. Doing so allows us to ascertain to what degree our portfolios will be affected by large shifts in the market, such as market corrections. In other words, we constantly prepare for episodes of market volatility, which in my view, may arrive sooner than later – even as the economy improves.

Instead of chasing the heat, I recommend staying focuses on what matters – key data points and economic indicators that could positively impact your investments.

To help you do this, I am offering all readers our Just-Released May 2021 Stock Market Outlook Report.

This report looks at several factors that are producing optimism right now and contains some of our key forecasts to consider such as:

- Zacks Rank S&P 500 Sector Picks

- Economic expectations for the rest of the year

- Zacks April and May view on equity markets

- A look at the Covid-19 vaccine tracker update

- A look at U.S. returns expectations for 2021

- What produces 2021 optimism?

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Wall Street Journal. April 22, 2021. https://www.wsj.com/articles/corporate-bond-gauge-signals-dwindling-economic-risk-11619083800?mod=markets_lead_pos4

4 Fred Economic Data. April 23, 2021. https://fred.stlouisfed.org/series/BAA10Y#0

5 Census. April 14, 2021. https://www.census.gov/econ/bfs/index.html

6 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

“The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.”