In today’s market, headlines move fast, but the data tells the real story. In this week’s Steady Investor, we break down what matters most for investors right now:

- Markets rally on two-week ceasefire deal

- Central banks repricing rate expectations

- Jobs data becoming less predictable

Markets Rally on Two-Week Ceasefire Deal – A two-week ceasefire between the U.S. and Iran sparked a broad relief rally across global markets, with equities rising and oil prices pulling back from recent highs. The agreement, which includes provisions tied to reopening the Strait of Hormuz, offered investors a temporary reprieve after weeks of escalating conflict that had disrupted energy markets and rattled sentiment. As many readers understand, the deal as it exists today is tenuous, and as we write, oil is not flowing freely through the Strait. But forward-looking traders and market participants are anticipating that the direction of travel is positive.

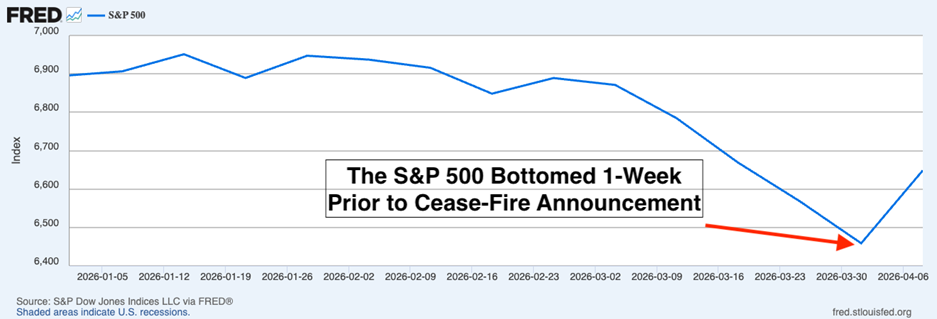

Indeed, the immediate reaction was swift. Oil prices dropped below $100 per barrel, which while still elevated relative to pre-war levels marks a notable step down from recent peaks. Stocks climbed across regions, which we think reflected optimism that the worst-case scenario for global energy supply may be avoided. A key takeaway for equity investors, however, actually took place last week. A closer look reveals that markets had already begun stabilizing before the ceasefire was formally announced (see chart below). A bounce off the bottom several days before the cease-fire suggests investors were increasingly looking past the most extreme outcomes, even as conditions on the ground remained uncertain. Reports of continued disruptions to shipping flows and lingering risks in the region did little to reverse the broader shift in asset prices, underscoring a key dynamic: markets tend to move ahead of definitive resolution.1

Source: Federal Reserve Bank of St. Louis2

2026 Tax Changes Could Impact Your Strategy

With 2025 taxes nearly behind us, now is the time to shift focus to 2026. Recent Federal legislation has introduced meaningful changes to the tax landscape, making proactive planning more important than ever for your long-term financial strategy.

To help, we’ve created our free guide, 10 Things to Know About Tax Planning in 20263. In this guide, you’ll get the key information you need about these updated tax rules to optimize your finance and tax decisions, including:

- New, higher Federal income tax brackets

- The increased standard deduction for 2026

- Increased 2026 retirement contribution limits

- New tax exemptions for tips and overtime

- Working Families Savings Accounts offer a new savings option

- Plus, many more Federal tax updates for 2026!

If you have $500,000 or more to invest and want to learn more, click on the link below to get your free copy:

Download 10 Things to Know About Tax Planning in 20263

That doesn’t mean risks have disappeared. The agreement is temporary, and key details, particularly around enforcement and shipping access, remain fluid. Energy prices are also likely to stay structurally higher than pre-conflict levels, reflecting ongoing supply concerns and precautionary stockpiling. We think the U.S. economy can sustain solid growth levels even with “higher for longer” crude prices, however, as evidenced by recent history and the fact that S&P 500 earnings estimates went up in Q1, not down.

How Global Central Banks are Responding to the War’s Second Order Effects – As readers have noticed in financial news and first-hand at the gas pump, rising energy prices have flowed through to costs for oil-related products like gasoline and fertilizer. This sharp rise in global energy prices—which we argued above may be sustained for some time—has triggered a rapid repricing across interest rate markets, with investors now anticipating a far more aggressive response from central banks than previously expected. In the U.S., expectations have swung dramatically. At the end of February, markets were pricing in roughly 2.4 rate cuts from the Federal Reserve in 2026. Today, that has flipped to a small net expectation of rate hikes by year-end. Similar shifts have taken hold in Europe, where expectations for modest easing have turned into multiple hikes priced for both the European Central Bank and Bank of England. This would be a net negative for markets, in our view, because of the implications on liquidity. But the market’s reaction may also be getting a little ahead of itself.While higher oil and gas prices can push inflation higher in the short term, central banks tend to look through energy-driven shocks unless they begin to influence longer-term inflation expectations. So far, that hasn’t happened. Market-based measures like the 5-year, 5-year forward inflation rate remain near ~2.1%, well below the peaks seen during the 2022 inflation surge. And looking historically, the Fed has generally avoided raising rates in response to energy shocks, often leaning the other direction if growth risks intensify. What we’re left with is rate markets pricing a sustained inflation problem, while underlying inflation expectations remain relatively anchored. We think the central bank response will prove more benign than markets currently appear to fear, and we’re still expecting a rate cut by the Fed later this year.4

Why Wall Street Economists Keep Getting Jobs Forecasts Wrong – Economists have been dead wrong in making payroll data predictions lately. Through the first three months of 2026, forecasts for monthly job creation have missed actual results by an average of 112,000 jobs, which marks a nearly 200% increase in wrongness from the previous year.In fairness to economists, however, the disconnect reflects a labor market that has become far more volatile and harder to model.Several factors are at play. Slower population growth tied to immigration policy is lowering the underlying pace of job creation, meaning monthly gains can now swing more easily above or below zero. At the same time, temporary disruptions like severe winter weather and large-scale strikes have created unusual month-to-month swings in hiring.

There are also more technical challenges. Government surveys are seeing lower response rates, making early estimates less representative, while recent changes to statistical models have increased short-term variability in the initial data. In the first two months of the year alone, these modeling adjustments contributed to swings of roughly 100,000 jobs more than usual. For markets, the takeaway is to keep in mind that individual data releases may carry more noise than usual. As a result, it’s likely wise to look through short-term reactions to headline numbers.5

How 2026 Tax Changes Could Impact You – Tax rules don’t just change; they create new opportunities and potential blind spots. Heading into 2026, understanding what’s different could make a meaningful impact on how much you keep and how effectively you plan.

Our free guide, 10 Things to Know About Tax Planning in 20266, is built to help you identify what matters most this year and how to adjust your strategy accordingly. Inside includes information regarding:

- New, higher Federal income tax brackets

- The increased standard deduction for 2026

- Increased 2026 retirement contribution limits

- New tax exemptions for tips and overtime

- Working Families Savings Accounts offer a new savings option

- Plus, many more Federal tax updates for 2026!

Disclosure

2 Fred Economic Data. April 9, 2026. https://www.cnbc.com/2026/04/08/us-iran-war-ceasefire-middle-east-strait-of-hormuz-oil-markets.html

3 ZIM may amend or rescind the “10 Things to Know About Tax Planning in 2026” guide for any reason and at ZIM’s discretion.

4 J. P. Morgan. March 27, 2026. https://www.jpmorgan.com/insights/markets-and-economy/top-market-takeaways/tmt-the-global-rates-repricing-will-central-banks-actually-hike

5 Wall Street Journal. April 8, 2026. https://www.wsj.com/economy/jobs/wall-street-prognosticators-struggle-in-whipsawing-jobs-market-5fade369?mod=economy_lead_pos5

6 ZIM may amend or rescind the “10 Things to Know About Tax Planning in 2026” guide for any reason and at ZIM’s discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.