The just-passed $1.9 trillion stimulus plan—combined with the $3.3 trillion in government spending that came before it—have been key factors driving the inflation conversation.

Fears of rising inflation are not unwarranted. Much of the Covid-19 stimulus has been direct payments to American businesses and households, and M2 money supply is growing at a 25% year-over-year pace.1 Commodity prices are on the move. Supply chain bottlenecks are putting pressure on factory input costs.

Inflation concerns are legitimate, but I think the widespread concern may be slightly overdone. For one, investors should be wary any time there is such clear market consensus about something like inflation. At Zacks Investment Management, we lean on our own proprietary research to make decisions – not on what is being widely reported in financial media.

Second, I think some key, under-appreciated forces at work could neutralize inflation pressure in the years to come. I detail four of these forces below.

__________________________________________________________________________

What to Do When Inflation is Worrying You – Focus on Key Data and Fundamentals!

This past month, we’ve witnessed the acceleration of what most investors fear – inflation. In a very volatile market, concerns of rising inflation will always be an unsettling topic when it comes to making financial decisions. The pressures of the media may cause you to make these decisions immediately, and often, without fully doing your research. In times like these, remember to not panic and don’t time the market! Now is the time to focus on fundamentals, hard data, and quality that can positively impact your investments in the long term.

To help you do this, I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- Zacks April and May view on equity markets

- A look at the Covid-19 vaccine tracker update

- A look at U.S. returns expectations for 2021

- Zacks Rank S&P 500 Sector Picks

- What produces 2021 optimism?

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released May 2021 Stock Market Outlook2

__________________________________________________________________________

- Demographics

About 10,000 baby boomers turn 65 every day. This means a significant portion of the workforce is marching towards retirement. The pandemic has accelerated the trend as baby boomers have not returned to the workforce as the economy reopens at nearly the pace of younger workers.

On the other end of the spectrum, the Brookings Institution estimates there will be 300,000 fewer births in the U.S. in 2021 than there would have been absent the pandemic and economic recession. Couple that data point with a 2016 landmark study published by the Federal Reserve, which found that sharp drops in fertility in the 1960s and 1970s were the biggest factor responsible for falling growth rates and interest rates after 1980.

At the end of the day, economic output (GDP growth) is driven by total workers in the economy multiplied by how productive each worker is. With demographic trends pointing to fewer total workers in coming years and decades, I think there could be some secular deflationary forces at work.3

- Technological Investment and Worker Productivity

Over the last year, companies across every sector of the economy invested in productivity-enhancing technology. Business investment in consumer equipment and software rose by 17% and 6% in Q4, respectively, even as GDP fell -2.4%. Companies also invested more in automation, videoconferencing software, and enterprise cloud services. In my view, this type of investment will continue scaling up in future years.

Investing in technology puts downward pressure on input prices and in many cases, increases productivity per worker – two deflationary forces.4

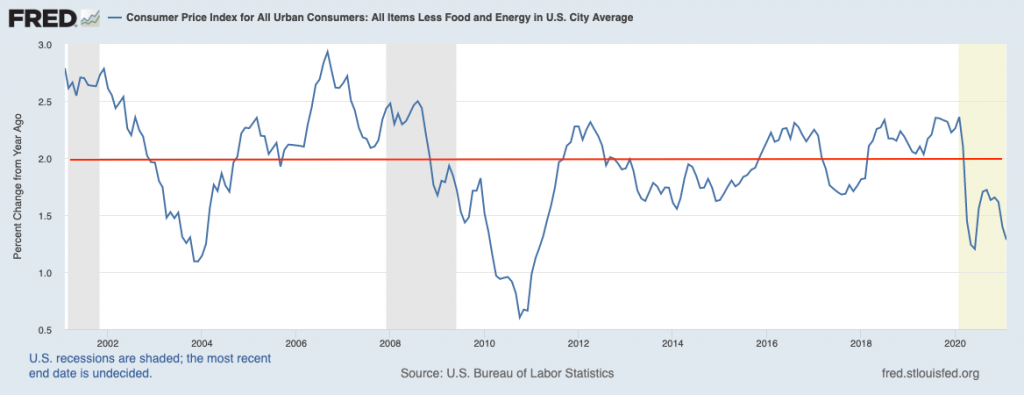

- Two Decades of Low Inflation

The issue over the last 20+ years in the U.S. has been not enough inflation. In the chart below, the red line shows the target 2% rate of inflation, which readers can see has been met only about half the time.

That’s why I think seeing inflation run above-target for a few quarters could be a good outcome, and it should not necessarily sound alarm bells at first. Inflation can be pernicious if unchecked, but a healthy amount of inflation is also good for the economy.

- The Federal Reserve Has Tools to Fight Inflation

If inflation becomes a concern down the road, the Federal Reserve has tools to push back. Among the primary tools available to the Fed, they could raise the interest rate paid to banks on excess reserves, reduce or end bond purchases, or raise the federal funds rate. One concern for many investors is that Fed action to tighten monetary policy and fight inflation automatically means selloffs and/or the end of the bull market. But bear markets usually start after the last Fed rate hike, not the first one.

Bottom Line for Investors

My point here is not to say that inflation will be unimportant or even modest in the quarters and years to come. But I do think the narratives currently surrounding inflation are painting it as an inevitable killer of economic growth and the bull market, which I think is overdone. There are economic forces at work that could neutralize inflation over time, and the Fed has tools to keep it in check.

Don’t let inflation cause you worry and act right away on your investment decisions. I recommend focusing on key data points and economic indicators that could positively impact your investments in the future. Here at Zacks, we manage client portfolios based on investment goals, and we drive our decision-making process based on research.

To help you focus on fundamentals, I am offering all readers our Just-Released May 2021 Stock Market Outlook Report.

This report looks at several factors that are producing optimism right now and contains some of our key forecasts to consider such as:

- Zacks April and May view on equity markets

- A look at the Covid-19 vaccine tracker update

- A look at U.S. returns expectations for 2021

- Zacks Rank S&P 500 Sector Picks

- What produces 2021 optimism?

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Wall Street Journal. December 3, 2020. https://www.wsj.com/articles/covid-shrinks-the-labor-market-pushing-out-women-and-baby-boomers-11607022074

4 Wall Street Journal. April 4, 2021. https://www.wsj.com/articles/u-s-s-long-drought-in-worker-productivity-could-be-ending-11617530401

5 Fred Economic Data. April 13, 2021. https://fred.stlouisfed.org/series/CPILFESL#0

6 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Returns for each strategy and the corresponding Morningstar Universe reflect the annualized returns for the periods indicated. The Morningstar Universes used for comparative analysis are constructed by Morningstar (median performance) and data is provided to Zacks by Zephyr Style Advisor. The percentile ranking for each Zacks Strategy is based on the gross comparison for Zacks Strategies vs. the indicated universe rounded up to the nearest whole percentile. Other managers included in universe by Morningstar may exhibit style drift when compared to Zacks Investment Management portfolio. Neither Zacks Investment Management nor Zacks Investment Research has any affiliation with Morningstar. Neither Zacks Investment Management nor Zacks Investment Research had any influence of the process Morningstar used to determine this ranking.

The Russell 1000 Value Index is a well-known, unmanaged index of the prices of 1000 large-company value common stocks selected by Russell. The Russell 1000 Value Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.