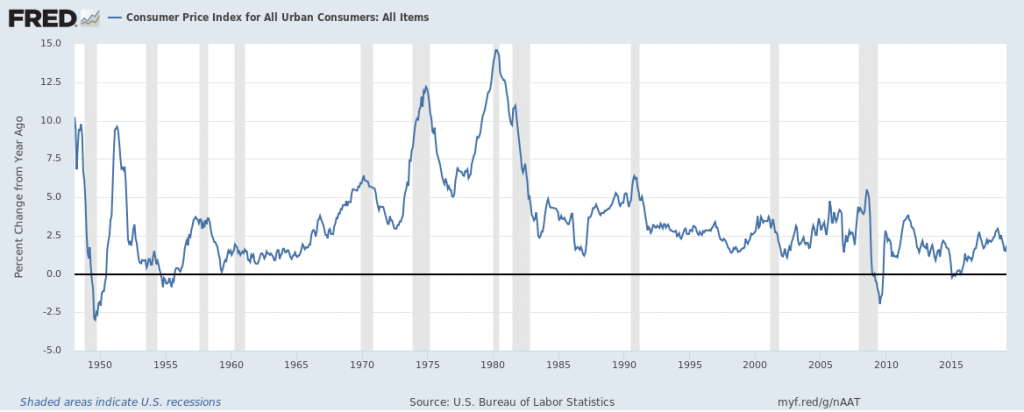

‘Inflation’ used to be a word that, when discussed in economic circles, often dealt in worrisome implications – fear of too much inflation or concern over not enough inflation (or at worst, deflation). Rarely have we seen inflation running at subdued, acceptable levels for long stretches of time, as we have arguably seen in the last decade or so:

Source: Federal Reserve Bank of St. Louis1

Indeed, from 1965 through the late 1980s, inflation posed a stubborn risk to U.S. economic health and growth. In the post-war boom with baby-boomers and women entering the workforce in droves, the Federal Reserve’s essential task was keeping inflation in check. So critical was the need to control inflation that in 1977, Congress mandated the Fed to “promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

The early 1990s saw the Fed’s inflation target land in the 1.5% to 2% range, and following the Great Recession, the Fed moved to make the official target 2%. As you can see from the chart above, much of the current economic expansion has featured inflation just under the Fed’s official target – even with the U.S. economy at full employment and interest rates near historic lows. The question is, why and how has inflation remained so low?2

__________________________________________________________________________

Focus on Fundamentals Instead of Inflation!

Inflation remaining at such subdued levels for so long can make many investors fear that it cannot last. But my recommendation would be not to let your emotions and fears get the best of you. Instead, stay focused on the fundamentals and other critical economic indicators.

To help you do just that, I am offering you our just-released Stock Market Outlook Report right now. This 22-page report is packed with some of our key forecasts and facts to consider such as:

- For how long will 2019 stay bullish?

- Zacks global markets’ outlook

- What sectors show the best opportunity?

- What industries within those sectors most merit your attention?

- Forecast for the S&P

- Small-cap vs. large-cap returns

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Stock Market Outlook Now3

__________________________________________________________________________

2 Reasons Inflation has not Responded to Low Interest Rates and Full Employment

So where did all the inflation go? I think you could point to two key drivers that are keeping prices in check, even without the Federal Reserve’s or other central bank’s involvement. They are: technological innovation and global supply chains.

On the technological innovation front, there is constant downward pressure on prices as technological innovation reduces the need for certain goods and services. Smartphones, for example, have reduced demand for cameras, which have driven prices lower. Technological innovation also puts pressure on its own prices, as new iterations of smartphones and other gadgets put downward pressure on the gadgets themselves. Finally, technological innovation has also increased labor productivity, thereby reducing unit labor costs. In a statistical analysis produced by the Federal Reserve Bank of St. Louis, the research found that an increase in labor productivity of three percentage points is associated with a reduction of inflation by about two percentage points.4

As long as this innovation persists and creates new efficiencies in the U.S. economy, I would argue that the downward pressure on prices is not likely to subside anytime soon, regardless of the monetary policy stance of the Fed.

The existence and increasing complexity of global supply chains is another factor I would cite as a key driver of low inflation. Although it seems as though protectionist rhetoric and policy is in vogue at the current economic moment, I do not think it’s likely to impact the already existing and rapidly growing supply chains across the world. As the cost of producing goods in other countries and the cost of moving the goods across the world lower with competition and innovation, so too will prices passed along to consumers.

Bottom Line for Investors

Looking back to the original question posed in the title of this week’s column, “Is Inflation No Longer a Threat to the U.S. Economy?”, I would argue that under the current circumstances – with technological innovation and global supply chains keeping downward pressure on prices even as unemployment is historically low – inflation is arguably pretty low on the list of concerns facing the U.S. economy (and is likely to remain that way throughout 2019).

One could even make the argument that when deciding the direction of monetary policy, the Fed would be better served turning their attention to other non-inflation indicators, especially given that the U.S. is more of a services-based economy today versus a goods-based economy (as it was when the Fed was originally given its mandate). An act of Congress may be required to shift this Fed mandate, which is to say, don’t plan on it happening anytime soon.

In the meantime, I recommend you also keep an eye on non-inflation indicators. To help you do this, you are invited to download our Just-Released Stock Market Outlook report.5

This Special Report is packed with our newly revised predictions the remainder of 2019 that we believe can help you base your next investment move on hard data.

For example, you’ll discover Zacks’ view on:

- For how long will 2019 stay bullish?

- Zacks global markets’ outlook

- What sectors show the best opportunity?

- What industries within those sectors most merit your attention?

- Forecast for the S&P

- Small-cap vs. large-cap returns

- And much more.

If

you have $500,000 or more to invest and want to learn more about these

forecasts, click on the link below to get your free report today!

Disclosure

2 BlackRock Blog, January 7, 2019. https://www.blackrockblog.com/2019/01/07/evolving-fed-inflation-mandate/

3 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

4 Federal Reserve Bank of St. Louis, April 3, 2018. https://www.stlouisfed.org/on-the-economy/2018/april/closer-look-reasons-low-inflation

5 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.