Macroeconomic headwinds started to build throughout the summer, which was also when the surge of the highly contagious Delta variant started to take a toll. Many businesses reluctantly delayed office re-openings and in some parts of the country, indoor capacity restrictions were reinstated. The travel and hospitality industry largely reported that bookings hit a soft patch.

Meanwhile, supply chains have not helped – product shortages, ballooning shipping costs, and backups at U.S. ports have hampered inventory restocks and snarled production at factories globally. Everything from cars to toys to Christmas decorations is in tight supply and starting to experience price pressures.

The effect on U.S. growth was palpable – consumers trimmed spending on hospitality services and travel in July, and supply constraints led many economists to trim GDP growth estimates for Q3. In one notable recalibration, the forecasting firm IHS Markit lowered their Q3 GDP forecast from 7.8% in July to 3.6% by late September.1

______________________________________________________________________________

Are We Headed for Another Economic Rebound? Protect Your Investments in the Meantime!

With questions surrounding the economy and whether a rebound is around the corner, do you know that there are things you can do now to navigate through these turbulent times?

No matter the state of the market – if you focus on the fundamentals instead of fear and media hysteria, you can protect your investments for the long term. To help you navigate this market, we are offering an exclusive look into our just-released October Stock Market Outlook Report.

This report contains some of our key forecasts to consider such as:

- Zacks rank S&P 500 sector picks

- Zacks view on equity markets

- What produces 2021 optimism?

- Zacks forecasts for the remainder of the year

- Zacks ranks industry tables

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released October 2021 Stock Market Outlook2

______________________________________________________________________________

Taken together, the persistent pressures on the global economy have led many investors to increase inflation expectations while lowering growth expectations, and for some, the outlook for the U.S. economic expansion has soured. I’ve even noticed the more frequent use of the term “stagflation” in the news lately, which describes the scenario of high inflation and low or negative growth. I think these worries are overblown.

Households have a record $142 trillion in net worth, wages are on the rise, and there are still roughly as many job openings as there are unemployed Americans. Consumers are paring spending on big-ticket items, like vehicles and furniture, but they are spending more in areas like retail and services. According to one estimate, households have still only spent about 25% of 2021’s stimulus payments.

In a sign that spending and growth remain in an upward trend, personal outlays on goods and services rose 0.8% in August compared to July, according to the Commerce Department. As you can see in the chart below, U.S. consumer spending has not missed a beat.

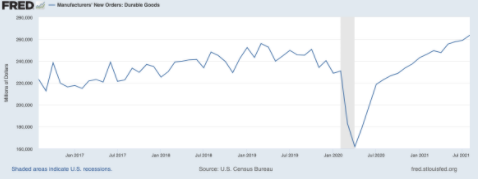

August also saw companies report a strong increase in new orders for durable goods, such as appliances, computers, TVs, and home furnishings. Even though a late-summer lull may have seen consumers hit the ‘pause’ button on economic activity, businesses are still largely reporting a struggle to meet demand in the marketplace.

Finally, I remain optimistic about the economic expansion because of further labor market improvements I see in the coming months. September was the first month that the expanded federal unemployment benefits expired, and school re-openings should pull some workers off the sidelines. There is, of course, no shortage of jobs waiting for those who re-enter the workforce – as I mentioned previously, the number of job openings in the U.S. roughly equals the number of unemployed Americans. Wages are also higher.

Bottom Line for Investors

If there is one thing I’ve learned about economic expansions over the years, it is that analysts are always looking for reasons to doubt the expansion’s resilience. July’s weak retail spending, which showed sales at retailers and restaurants falling -1.1%, was enough for many to start calling into question whether growth would last. A short period of weak growth coupled with largely expected high inflation readings was enough to declare stagflation.

I disagree. In addition to the fundamentals detailed above, I would also point out that the economic drag from the latest Covid-19 surge was far more tempered than previous surges, which to me indicates the economy and businesses have learned and are adapting. In my view, aggregate demand and future growth were not lost as a result of the Delta surge but were merely delayed by a few months. I’m adjusting my growth expectations higher for Q4 2021 and 2022, accordingly.

In the meantime, I recommend that you focus on the fundamentals and facts that can positively impact your investments in the long term. Make the most out of this market!

Our Just-Released October 2021 Stock Market Outlook Report5, will help you do just that. This report is packed with newly revised predictions that can help you base your next investment move on hard data. For example, you’ll discover Zacks’ view on:

- Zacks rank S&P 500 sector picks

- Zacks view on equity markets

- What produces 2021 optimism?

- Zacks forecasts for the remainder of the year

- Zacks ranks industry tables

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Fred Economic Data. October 1, 2021. https://fred.stlouisfed.org/series/PCE#0

4 Fred Economic Data. October 4, 2021. https://fred.stlouisfed.org/series/DGORDER

5 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The MSCI ACWI captures large and mid-cap representation across 23 Developed Markets (DM) and 27 Emerging Markets (EM) countries. With 2,986 constituents, the index covers approximately 85% of the global investable equity opportunity set. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI UK All Cap Index captures large, mid, small and micro-cap representation of the UK market. With 819 constituents, the index is comprehensive, covering approximately 99% of the UK equity universe. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 1000 Value Index is a well-known, unmanaged index of the prices of 1000 large-company value common stocks selected by Russell. The Russell 1000 Value Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.