Markets are shifting again. This issue of Steady Investor highlights the three themes investors should watch now.

- Fed signals mortgage market shift

- Beef prices reflect structural shortage

- Commercial real estate faces reset

- Private equity faces reality check

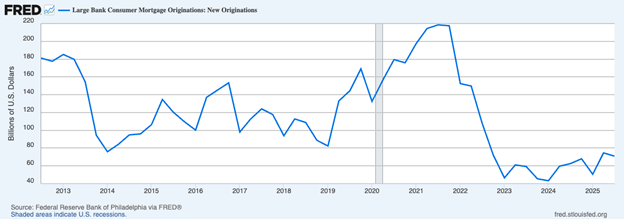

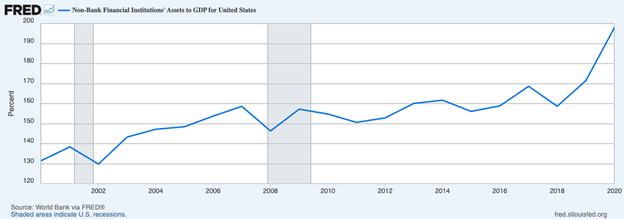

Fed Proposal Could Reshape the Mortgage Market – A shift may be coming to the U.S. mortgage market. In the years following the 2008 financial crisis, major banks such as JPMorgan Chase and Wells Fargo stepped back from home lending, constrained by tighter capital requirements tied to Dodd-Frank and other new regulation.1

Consumer Mortgage Originations by Large Banks

To fill the gap, nonbank lenders like Rocket Mortgage stepped in, and now originate the majority of U.S. mortgages.

Nonbank Assets Relative to GDP

Is Your Retirement Portfolio on Track in Today’s Market?

Market uncertainty challenges investors, and staying on track for retirement takes more than hope—it requires clear goals, smart investment choices, and disciplined portfolio management.

To help you take control of your retirement plan, we’re offering a free Ultimate Retirement Portfolio Guide3, which includes actionable steps to build a portfolio designed for your needs, including:

- Accurately forecasting your retirement income needs

- The two phases of determining your asset allocation

- Developing an investment discipline that allows you to get good results over time

- Avoiding self-sabotage—what you need to know

- Plus, our views on key steps to create and maintain the ultimate retirement portfolio

If you have $500,000 or more to invest, get this guide and explore strategies to potentially secure your long-term financial future.

Get our FREE guide: 7 Secrets to Building the Ultimate DIY Retirement Portfolio4

The Federal Reserve wants the pendulum to swing back. Federal Reserve Vice Chair Michelle Bowman has proposed easing certain capital rules, particularly around larger down payments and mortgage-servicing rights. The goal is to make it more attractive for banks to reenter the space. Mortgage rates remain stuck near 6%, which is limiting activity in the housing market as would-be sellers don’t want to trade a lower mortgage rate for a higher one, and as buyers balk at higher financing costs. However, if large banks regain market share, competition could theoretically increase, which may put downward pressure on rates. For consumers, that may eventually mean more options, and for lenders, it signals a potential reshuffling of a market that has looked very different since the financial crisis.

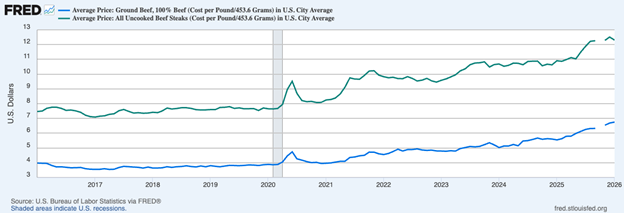

Beef Prices Stay Elevated as Supply Lags Demand – High beef prices in the U.S. are increasingly looking less like a short-term spike and more like a structural shift. The U.S. cattle herd is at its lowest level in roughly 75 years, according to USDA data, after years of drought and pandemic-era financial strain prompted ranchers to shrink herds.At the same time, demand hasn’t wavered. Ground-beef prices were up 17% year over year in January, far outpacing broader grocery inflation. Many consumers continue to pay up, reinforcing beef’s status as a “premium protein.”The problem for prices, however, is that rebuilding herds takes time, and ranchers remain broadly cautious. Expanding too quickly risks overproduction, a problem that has pressured crop markets in recent years. Industry estimates suggest meaningful herd growth may not arrive until 2028. For restaurants, grocers, and consumers, that means higher beef prices may persist, reflecting a classic imbalance of tight supply meeting resilient demand.5

Average Price of Ground Beef (blue line) and Uncooked Beef Steaks (green line)

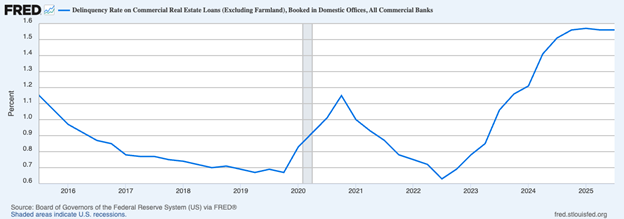

Commercial Real Estate Stress Moves into a New Phase – The long-running “extend and pretend” phase in commercial real estate appears to be ending. After years of loan extensions, lenders are increasingly forcing resolutions on troubled properties, especially in the office sector.

The delinquency rate for office loans in commercial mortgage-backed securities has climbed to a record 12.34%, according to research firm Trepp.7

Delinquency Rates on Commercial Real Estate Loans

Meanwhile, more than half of the roughly $100 billion in commercial mortgage-backed securities (CMBS) loans maturing this year are unlikely to repay at maturity. With interest rates far above pandemic-era lows and hybrid work reducing structural demand for office space, many borrowers are struggling—and will continue to struggle—to refinance. For investors, it’s a reminder that illiquid assets can face prolonged adjustments when underlying fundamentals shift, often unexpectedly.

Elite Endowments Re-Evaluate Their Private Equity Allocations – Some of the nation’s most sophisticated investors are rethinking private equity. Princeton University recently lowered its long-term return expectations, citing weaker private-market performance. Yale University trimmed its leveraged buyout exposure for the first time in a decade, while Harvard University has turned to the secondary market to sell private holdings early.Over the three years ended June 30, private capital returned 7.4% annually, according to Cambridge Associates, well below the 19.7% annual gain in the S&P 500. Meanwhile, unsold portfolio companies sit near multi-decade highs, and higher interest rates have slowed dealmaking and exits.And yet, private equity still accounts for more than 40% of assets at some Ivy endowments. This dynamic underscores a broader reality, in our view, that illiquidity and complexity in private markets do not guarantee outperformance.9

Building a Resilient Retirement Portfolio in Today’s Market – With markets shifting, economic data evolving, and investor sentiment changing quickly, now is a smart time to revisit your retirement strategy. Periods of uncertainty can test long-term plans, but they can also create opportunities for disciplined investors who stay focused on fundamentals.

Download our updated guide, 7 Secrets to Building the Ultimate DIY Retirement Portfolio10, for a clear, step-by-step framework to design a portfolio built for long-term goals, even in an uncertain market.

This guide offers actionable insights on:

- Accurately forecasting your retirement income needs

- The two phases of determining your asset allocation

- Developing an investment discipline that allows you to get good results over time

- Avoiding self-sabotage—what you need to know

- Plus, our views on key steps to create and maintain the ultimate retirement portfolio

If you have $500,000 or more to invest, get this guide to learn our ideas on the step-by-step process of building and maintaining a retirement portfolio that will potentially help you reach your goals and enjoy a secure retirement.

Disclosure

2 Fred Economic Data. January 21, 2026. https://fred.stlouisfed.org/series/RCMFLOORIG

3 May 7, 2024. https://fred.stlouisfed.org/series/DDDI03USA156NWDB

4 ZIM may amend or rescind the “7 Secrets to Building the Ultimate DIY Retirement Portfolio” guide for any reason and at ZIM’s discretion.

5 Wall Street Journal. February 19, 2026. https://www.wsj.com/business/beef-prices-higher-cattle-2e0a9b65?mod=economy_lead_story

6 Fred Economic Data. February 13, 2026. https://fred.stlouisfed.org/series/APU0000703112

7 Fred Economic Data. February 17, 2026. https://fred.stlouisfed.org/series/APU0000703112

8 Fred Economic Data. November 21, 2025. https://fred.stlouisfed.org/series/DRCRELEXFACBS

9 Wall Street Journal. February 15, 2026. https://www.wsj.com/finance/investing/the-ivies-are-having-second-thoughts-about-investing-in-private-equity-de04e52a?mod=djemMarketsAM

10 ZIM may amend or rescind the “7 Secrets to Building the Ultimate DIY Retirement Portfolio” guide for any reason and at ZIM’s discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.