Market conditions are changing rapidly. This issue of Steady Investor covers the three trends investors can’t ignore:

- Oil drives inflation uncertainty

- Payroll drop, income steady

- China trade shows global resilience

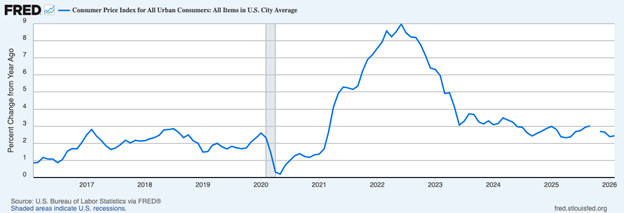

February’s Inflation Report was Just Released, but It’s Already Old News – The inflation story got better in February. According to the Bureau of Labor Statistics, consumer prices rose 2.4% from a year earlier and core inflation held at 2.5%.1

On its own, that would normally be welcome news for investors hoping the Federal Reserve is getting closer to cutting interest rates. But markets are already looking past that report.The reason, of course, is oil prices. In other words, the inflation print was less of a fresh read on where inflation is going, and more a snapshot of where it stood pre-energy shock. Oil prices trickle through to transportation costs, shipping, air travel, plastics, chemicals, fertilizers, and a wide range of goods and services across the economy. If oil prices move up sharply but then fall back quickly, the inflation impact may prove limited. We’ve seen a lot of price volatility like that to date. But if prices stay elevated for weeks or months, the risk is that higher energy costs start feeding more broadly into consumer prices and business expenses. Enter the Federal Reserve. The February inflation numbers, coupled with a weak jobs report (see below), set the stage for another rate cut perhaps this spring. That picture is complicated now. Markets are trying to determine whether this is a temporary commodity spike or the start of something bigger. In our view, markets appear to be pricing in the latter, i.e., a supply shock with a longer tail that keeps prices elevated for a long stretch of time. While that outcome is certainly possible, it also sets the markets’ base case as the worst-case scenario—meaning that even a slightly better-than-expected outcome can send prices sharply in the opposite direction.

Is Your Retirement Plan Ready for the Unexpected?

Most retirement plans assume life follows a straight path, but market swings, health issues, and inflation can quickly disrupt it.

To help you prepare for uncertainty, we’re offering a free Crisis-Proof Retirement Guide3. It outlines practical steps to help build a retirement strategy resilient enough to handle life’s detours, including:

- How to diversify across time, tax treatment, and income sources

- Which overlooked risks pose the greatest threat to long-term security

- How to build flexibility into your withdrawal and investment approach

- Why annual reviews are essential for staying on course

- How a research-driven advisor can help reinforce durability

- And more…

If you have $500,000+ to invest, download our free guide to discover strategies and help protect your retirement against market shocks and life’s unexpected events.

Get our FREE guide: How to Build a Retirement Plan Designed for Uncertainty3

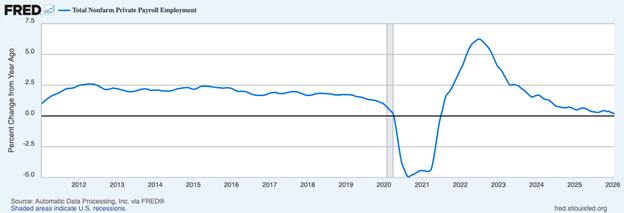

A Weak February Jobs Report Puts Labor Markets Back in Focus – February’s jobs report raised a few eyebrows. The Bureau of Labor Statistics reported that the U.S. lost 92,000 jobs for the month, with the unemployment rate ticking slightly higher to 4.4%. Revisions to previous months also meant trimming payrolls by a combined 69,000, which together solidified the narrative that the jobs market is weakening.4

But the details suggest investors should be careful about overreading a single payroll report. Some of February’s weakness appears tied to factors that may not prove durable, including strike-related losses in health care and continued reductions in federal payrolls. Health care employment fell by 28,000 in February, with physicians’ offices alone losing 37,000 jobs due primarily to strike activity. Federal government employment fell another 10,000 and is now down 330,000 from its October 2024 peak. More importantly, payroll growth is only one way to look at the labor market’s economic impact. Household spending depends less on one month’s hiring number than on whether income continues to grow. On that front, the picture is firmer than the payroll headline implies. Average hourly earnings rose 0.4% in February and were up 3.8% from a year earlier, while the aggregate weekly payrolls index for total private workers was up about 4.4% over the past year. In other words, even with payroll growth choppy, total labor income is still moving higher, and that’s key for consumer spending—the main engine of the U.S. economy.

China’s Trade Surge is Another Sign Global Growth Has Held Up – China’s latest trade data were stronger than expected, with exports rising 21.8% in January and February from a year earlier and imports climbing 19.8%, pushing the country’s trade surplus to about $213.6 billion. Some of that strength may reflect Lunar New Year timing, since the holiday shifts between January and February each year. But the broader message, in our view, is that China’s trade engine is still running strongly despite tariffs, weaker trade with the U.S., and widespread skepticism about the country’s economic outlook. The regional details make that picture even more interesting. Exports to the U.S. fell 11% from a year earlier, but that weakness was offset by strong gains elsewhere, including nearly 28% growth in exports to the European Union, 16% growth to Latin America, and solid gains across the rest of Asia, including Japan and India. That suggests China’s export sector remains highly adaptable, finding demand across a broad global customer base.In our view, this report tells us just as much about the global economy as it does China. It is another sign that the global economy has remained more resilient than many expected.6

Prepare Your Retirement for the Unexpected – Life rarely goes as planned. Market drops, inflation spikes, or unexpected health events can throw your retirement off track.

Our free Crisis-Proof Retirement Guide7 from Zacks tax experts help you build a plan designed to withstand uncertainty. Inside includes:

- How to diversify across time, tax treatment, and income sources

- Which overlooked risks pose the greatest threat to long-term security

- How to build flexibility into your withdrawal and investment approach

- Why annual reviews are essential for staying on course

- How a research-driven advisor can help reinforce durability

- And more…

If you have $500,000+ to invest, download our free guide to discover strategies and help protect your retirement against market shocks and life’s unexpected events.

Disclosure

2 Fred Economic Data. 2026. https://fred.stlouisfed.org/series/CPIAUCSL

3 Zacks Investment Management reserves the right to amend the terms or rescind the free How to Build a Retirement Plan Designed to Withstand Uncertainty offer at any time and for any reason at its discretion.

4 Wall Street Journal. March 6, 2026. https://www.wsj.com/economy/jobs/february-jobs-report-unemployment-1d7d1a9b?mod=economy_feat5_jobs_pos2

5 Fred Economic Data. March 4, 2026. https://fred.stlouisfed.org/series/ADPWNUSNERSA

6 Wall Street Journal. March 10, 2026. https://www.wsj.com/economy/trade/chinas-exports-surge-in-first-two-months-of-year-96ab6abb?mod=economy_lead_pos2

7 Zacks Investment Management reserves the right to amend the terms or rescind the free How to Build a Retirement Plan Designed to Withstand Uncertainty offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.