In the wake of the 2008 Global Financial Crisis, the U.S. government was pulling all levers to try and stabilize the economy and get growth back on track. In addition to unprecedented bailout programs like TARP and liquidity-boosting schemes like QE1 and QE2, the Federal Reserve also effectively lowered interest rates to zero. In all, between 2008 and 2015, the Fed’s balance sheet soared from $900 billion to $4.5 trillion.1

As the U.S. economy started to recover and grow, a new consensus formed about what was likely to happen next: runaway inflation. Even with the benefit of hindsight, calling for higher levels of inflation seemed at the time like a very logical conclusion to draw. With the Fed essentially eliminating the cost of borrowing and injecting trillions of dollars into U.S. companies and the financial system, surely we’d see a surge in inflation to be reckoned with down the road…right?

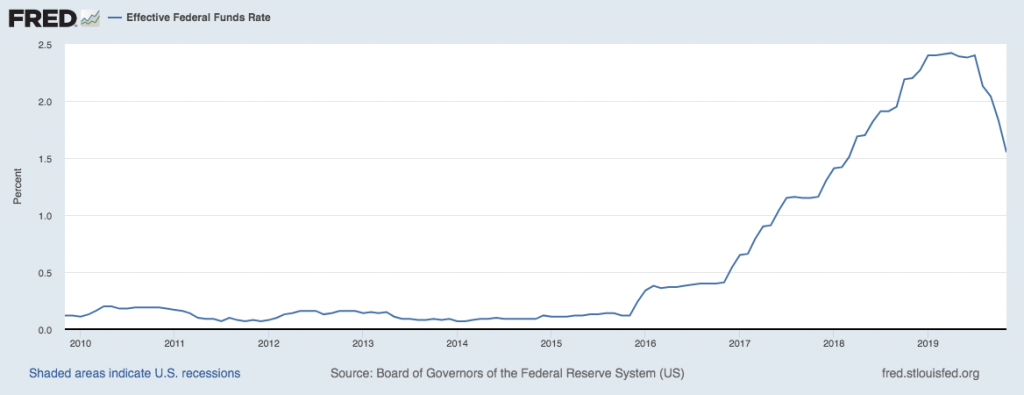

Yet here we are a decade later, with no signs of runaway inflation. There has been no inflation ‘reckoning,’ no systematic monetary policy tightening to try and stave off higher prices. In the months and years just after the financial crisis, consensus had largely been that the fed funds rate would be north of 4% by 2020. But with just a handful of days left in the year, the fed funds rate remains in a range of 1.5% to 1.75%, with the economy trudging along with below-target inflation and slower-than-average economic, wage, and productivity growth (but better-than-expected employment).2

_________________________________________________________________________

Base Your Investing Decisions on Hard Data!

In addition to inflation, I believe there are other important economic indicators to keep on eye on, especially as you start planning your investments for 2020.

To help

you do this, I am offering all readers a look into our just-released January

2020 Stock Market Outlook report.

This report will provide you with our forecasts along with additional factors

to consider:

- Should you stay bullish?

- What sectors show the best opportunity?

- What industries within those sectors most merit your attention?

- What produces U.S. optimism in the coming year?

- Year-end forecast for the S&P

- Small-cap vs. large-cap returns

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released January 2020 Stock Market Outlook3

_________________________________________________________________________

Even as the Fed has Kept Interest Rates “Lower for Longer,” Inflation Remains in Check

So, What Happened? Why Did Inflation Never Really Take Hold?

I’m not sure we’re at a point in history yet where it’s possible to look back at this decade and understand exactly why inflation remained so subdued, for so long. But there are a few working theories I’ll share with readers.

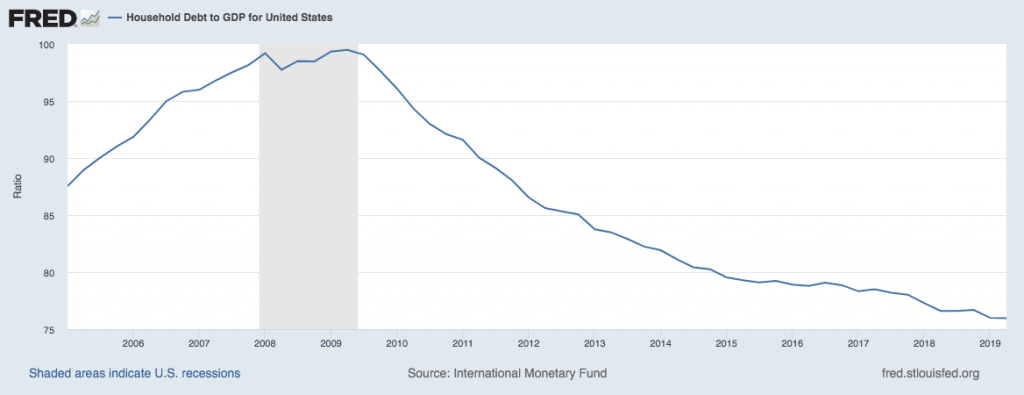

First – the return of the savers. In the wake of a financial crisis – particularly one that profoundly affected nearly every American – we tend to see households, businesses, and banks de-risk and take steps to improve balance sheets. Regulation forced banks to make such changes, and households followed suit and paid down debt in the ensuing years. These actions generally mean less borrowing, investing, and risk-taking, which keeps a lid on growth, inflation, and interest rates. As you can see from the chart below, household debt to GDP fell significantly in the years following the recession.

Household Debt-to-GDP Ratio in the US, 2005 – Current

A second possible cause for weak inflation is technology, which has actually been a deflationary force since the 1990’s, in my view. I also believe in the possibility that technology’s cost-reduction results in a multiplier effect, which results in various deflationary linkages throughout the economy.

There are myriad ways to think about how technology has reduced the cost of goods and the cost of doing business. Think about household goods and retail. The massive shift to buying goods via e-commerce (online shopping, Amazon) versus a trip to a brick-and-mortar store may increase the cost of physical delivery, but it reduces or eliminates cost of real estate, utilities, requires few workers, lowers inventory carrying costs, and uses data to target consumers with precision ads – which are far more effective than traditional marketing methods. In all, technology has driven efficiency, which has kept a lid on costs and prices.

Finally, a third possible explanation for subdued inflation over the last ten years is spare capacity in the U.S. economy. The ‘Great Recession’ led to such a dramatic decline in output, job losses, and wealth destruction that it created a substantial amount of spare capacity in the economy that we’re only now starting to reach. It would make sense, then, that price pressures would remain tepid so long as that spare capacity existed.

Bottom Line for Investors

Even with weaker-than-expected inflation – or perhaps because of it – the U.S. economy has managed to deliver its longest economic expansion on record, with unemployment at a 50-year low and the stock market at all-time highs. In other words, this head-scratching bout of low inflation has not resulted in any material adverse impact for investors, businesses, or consumers.

As we move forward from here, my cautionary advice to investors would be that just as everyone starts to ignore or write-off inflation for good, that’s when you should perk up and watch for rising inflation and rising interest rates. It could happen sooner than many think.

To help you keep an eye on inflation as well as other key economic factors, I am offering all readers our Just-Released January 2020 Stock Market Outlook Report.

This Special Report is packed with newly revised predictions to consider for 2020 that can help you base your next investment move on hard data. For example, you’ll discover Zacks’ view on:

- Why you should stay bullish?

- What sectors show the best opportunity?

- What industries within those sectors most merit your attention?

- What produces U.S. optimism in the coming year?

- Year-end forecast for the S&P

- Small-cap vs. large-cap returns

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!6

Disclosure

2 The Wall Street Journal, December 12, 2019. https://www.wsj.com/articles/economists-got-the-decade-all-wrong-theyre-trying-to-figure-out-why-11576346400

3 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

4 Board of Governors of the Federal Reserve System (US), Effective Federal Funds Rate [FEDFUNDS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FEDFUNDS, December 19, 2019.

5 International Monetary Fund, Household Debt to GDP for United States [HDTGPDUSQ163N], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/HDTGPDUSQ163N, December 20, 2019.

6 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.