10 years ago last week, on September 15, 2008, Lehman Brothers filed for bankruptcy. At the time, few investors, analysts, or investment professionals fully understood the extent of damage the Lehman event would ultimately cause.

The S&P 500 fell by -28% in just 22 days, and the index ended up losing more than half its value through the trough of the bear (March 2009). The unemployment rate in America went from around 5% in January 2008 to 9.8% in January 2010. Millions of Americans lost their jobs and their homes, and the United States entered one of the deepest recessions it’s ever experienced. At one point, GDP fell by -8.9% in a single quarter (Q4 2008), its worst decline in 50 years. Home mortgage defaults soared from 3.66% to 11.54%.1

Today, ten years on, the equities markets have recovered and have reached new all-time highs. Corporate America, along with the global economy, continue to expand. On balance, the world has indeed recovered from the 2008 crisis.

_________________________________________________________________

We Will Experience Another Crisis, the Question is When?

Anticipation for another crisis can be a scary thought. But, instead of getting caught up in fears of what’s to come, the key is to focus on the long-term and on key economic indicators that can help you stay level-headed. To help you do this, we are offering all readers an exclusive look into our just-released Stock Market Outlook report.

This report will provide you with our forecasts along with additional factors to consider:

- What produces U.S. optimism?

- Forecast for the S&P

- Small-cap vs. large-cap returns

- Which sectors are hot and which are not?

- What industries within those sectors most merit your attention?

- Odds of recession

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released Stock Market Outlook2 >>

________________________________________________________________________

In my view, if there’s one immutable lesson/takeaway we can apply to this experience in hindsight, it’s that even the darkest of days eventually come to an end. Just when pessimism and doubt are running at their highest, the economy can and has recovered. Brighter days follow the dark ones.

For investors, surviving the financial crisis often meant not believing the most severe of doomsday scenarios about the U.S. economy. It also meant enduring some pain to remain patient. As we know today with the benefit of hindsight, it would have been better to have faith that the U.S. economy and stock markets would not only recover, but reach new heights. Throughout history, they have, and I believe this time around is no exception.

There are several lessons and takeaways that Zacks Investment Management took from the financial crisis, which we apply in our investment approach to this day. But this week, I want to highlight four that I think are the most important.

Takeaway #1: Most People Still Get the Cause of the Crisis Wrong

The scapegoats for the financial crisis are almost always ‘greedy Wall Street bankers.’ While there is certainly fault in abhorrent risk management and over-leverage, blaming Wall Street for the entire crisis misses the full picture, in my view.

Mortgage originators share in the blame. Homeowners and folks who bought two and three houses they couldn’t afford are to blame. And perhaps more importantly, bad regulation is to blame.

Excess was building up in the capital markets and housing markets with subprime mortgages and banks owning too many mortgage-backed securities. Chances are, the bubble would have burst on its own. But in my opinion, the event that tipped the market into a frenzy – and made matters far worse than they had to be – was the issuance of accounting regulation FAS 157 on November 15, 2007 (days away from the peak of the market).

In short, FAS 157 required banks to use mark-to-market accounting to account for mortgage-backed securities, which essentially deemed these securities worthless overnight. Balance sheets collapsed, and the credit markets froze. It happened in the blink of an eye.3

Former Federal Reserve Chairman, Ben Bernanke, released a new research paper stating that it was this credit-market panic and the runs on credit markets – not the housing bust – that better explains the crisis.4

Takeaway #2: Regulation Isn’t Inherently Good or Bad – It Just ‘Is’

In the case of FAS 157, I’d say regulation was bad. But not all regulations are bad or inhibitive to economic progress. In many cases, regulations are just a fact of life that businesses have to deal with and oftentimes work around.

Following the financial crisis, there was a rush to regulate in an effort to prevent the crisis from happening again. There was Basel III, which was a global financial reform effort to boost major banks’ capital positions across the world. In the U.S., there was the Dodd-Frank regulation, which set requirements for how much tiered capital banks needed to keep on balance sheets, established “stress tests” for the nation’s biggest banks, and created the Financial Stability Oversight Council aimed at identifying and mitigating systemic risks.5

Were all of these new regulations necessary and/or helpful? I’d say yes and no, and that some regulations are working while others aren’t. Again, regulations just are what they are. They may hamstring growth and risk-taking, but they may also serve to prevent a repeat.

Takeaway #3: From a Debt Perspective, Americans are Better Off

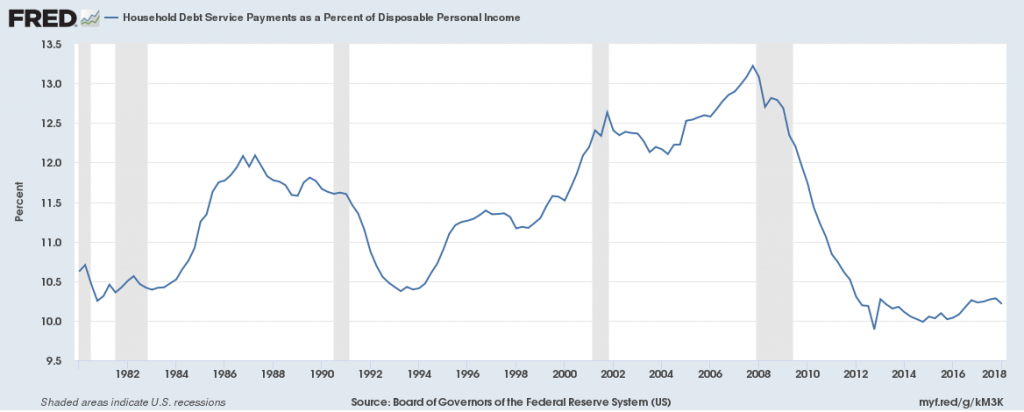

American households appear to have learned our lesson from the crisis. Leading up to the crisis, Americans debt service payments as a percent of disposable income was too high, nearing 14%. Today that number is down to a little over 10%, signaling that households are far less leveraged than they were pre-crisis. One item to note (and to keep an eye on), however, is that while households and banks have cut back on leverage, corporations and the U.S. government have gone the other way.6

Source: Federal Reserve Bank of St. Louis

Takeaway #4: Crises and/or Bear Markets Usually End When Circumstances are Still Dire

When the bear market ended in March 2009, economic conditions were awful, and investors were completely fatigued. Economic data at the time showed that Real GDP had declined -6.3% in Q4 2008, and that capacity utilization had dropped to 69% in March (2009), a record low going back to 1967.7 It felt like a time to throw in the towel if you hadn’t quit the market already.

But as we know today, it was at this seemingly darkest hour that the economy and the stock market were poised to start the 10-year long economic expansion and bull market that continues to this day, as I write. The lesson we remember here is that it is often when things feel the worst that they are about to get a lot better.

Bottom Line for Investors

I believe with confidence that we will experience another crisis in the future. I cannot say when or how severe, just that I believe it will occur.

But I also believe that the U.S. economy will bounce back, the U.S. stock market will bounce back, and that American workers will live through it. Our skills as a nation won’t go away, our innovative spirits won’t go away, and our ability to create great companies and great products won’t go away. I’d argue they will only get stronger. And for long-term investors, that’s the bottom line.

In the meantime, I’d encourage investors to stay focused on the fundamentals. And to help you do just that, I invite you to download our Just-Released Stock Market Outlook Report >>8

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook Report at any time and for any reason at its discretion.

3 Silverlight Asset Management, September 19, 2018, http://www.silverlightinvest.com/blog/lessons-lehma

4 The Wall Street Journal, September 13, 2018, https://www.wsj.com/articles/ben-bernanke-says-credit-freeze-more-to-blame-than-housing-bust-in-latest-recession-1536868914

5 Axios, September 15, 2018, https://www.axios.com/newsletters/axios-deep-dives-e9ec5933-4529-49ff-bbbe-f8a460d1971c.html

6 Axios, September 15, 2018, https://www.axios.com/newsletters/axios-deep-dives-e9ec5933-4529-49ff-bbbe-f8a460d1971c.html

7 Silverlight Asset Management, September 19, 2018, http://www.silverlightinvest.com/blog/lessons-lehma

8 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook Report at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.