By April 18th, a record 12.4% of the US workforce was receiving unemployment benefits, with over 30 million submitting jobless claims. Estimates suggest that in the coming weeks, the unemployment rate could approach 20%, which would bring the economy closer to levels seen during the Great Depression. U.S. factory activity in April, as measured by the ISM production index, essentially ground to a halt, as did consumer purchases.1 The U.S. personal saving rate rose to its highest level since 1981, as consumers were either unwilling or unable to spend.

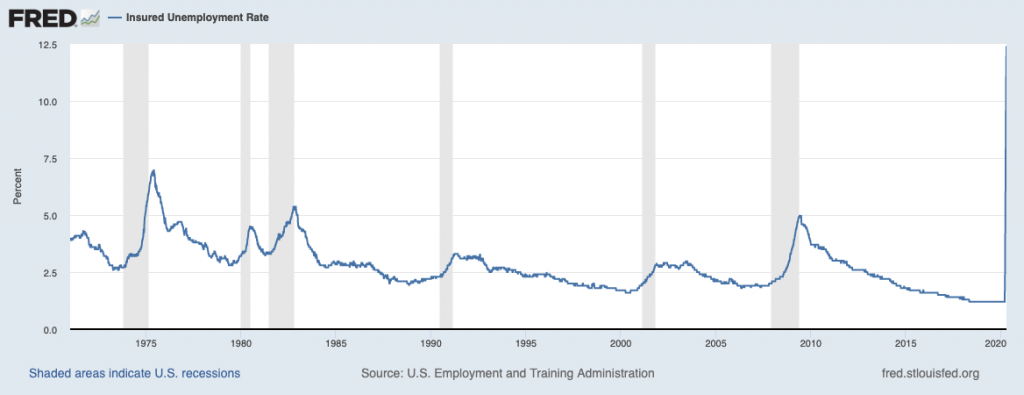

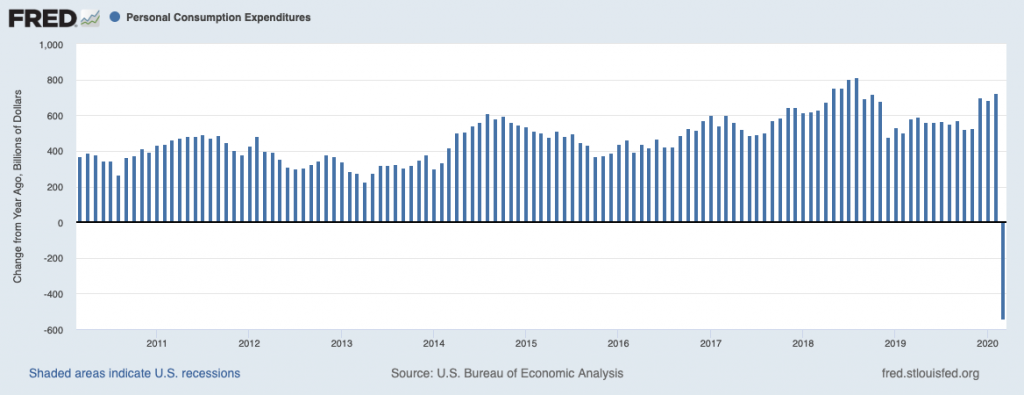

Many readers have likely seen charts like the ones below as it relates to the gravity of economic impact, with the unemployment rate dramatically spiking (top) and consumer spending falling off a cliff (bottom).

The Unemployment Rate Spiked Straight Upward

Source: Federal Reserve Bank of St. Louis2

While Consumer Spending Plummeted

As the dismal economic data was blanketing the airwaves and newspapers in April, the S&P 500 marched +12.7% higher, posting its best monthly performance in 33 years. 5 The disconnect between the economy telling one story and the stock market telling another understandably perplexes many investors. How can the stock market possibly do so well while economic conditions are so dire?

____________________________________________________________________________

Taking Cues from Headlines May Be Costly…Time to Focus on the Fundamentals

Instead of letting fearful headlines and media hysteria cause you to make knee-jerk responses, I recommend making decisions based on data and fundamentals. To help you do this, I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- 10 trends we are seeing in a COVID economy

- How will coronavirus continue to impact the markets?

- Inside unemployment rates

- Is it time to buy U.S. stocks?

- What of US GDP growth?

- U.S. returns expectations for 2020

- What produces 2020 optimism?

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released May 2020 Stock Market Outlook4

____________________________________________________________________________

Some may argue that the market rally has everything to do with the Federal Reserve. Virtually unlimited monetary stimulus and liquidity are making its way into the stock market. Others may cite the $2.4 trillion package of government spending ‘propping up’ the economy and markets. I fully acknowledge (and support) the role that fiscal and monetary stimulus plays in stabilizing the economy and markets, but my response to the ‘disconnect’ between the economy and the stock market is much simpler: stocks have a long history of rallying in the midst of terrible news.

Take the 2007-2009 bear market, for example. When the S&P 500 hit its low on March 9, 2009, jobless claims were still rising. Jobless claims eventually peaked at the end of the month but stayed high basically until the following year (2010). The unemployment rate also kept going up throughout 2009, with a falling labor-force participation rate and a general sense that the U.S. economy was doomed. But by the end of March 2009, the S&P 500 had soared +18.1% off the low, and by the end of the year stocks had rallied +67.8%.6 The stock market was telling one story, while the economy and sentiment were telling another.

Taking your cues from the economic headlines of the day can be a costly mistake. For example, if a person had invested $100,000 in the S&P 500 on March 9, 2009, they would have accumulated $630,000 by the time the market peaked in February 2020. But if the investor had waited just three more months to invest (June 2009, when the economic headlines were slightly better but still bad), the same $100,000 would have only grown to $450,000.7 We can find examples of this type of outcome throughout history. Stocks rarely wait for good news to arrive.

One Note About Unemployment in the U.S.

As dire employment data continues in the coming weeks and months, there is a silver lining I think investors should keep in mind.

A key differentiator between this recession and past recessions is that a significant number of employers are using furloughs rather than outright layoffs to trim the workforce. In theory, this means that re-starting the economy could be less stressful than after a structural recession (like 2008). When employees are asked to return to work, there’s no need for training, recruitment, job search, background checks, ‘onboarding,’ etc., all of which are costly and time-consuming. Workers can return to their jobs and immediately be productive.

Time will tell what the economy looks like in the coming months, and whether or how soon many workers will be asked to return. But I’m hopeful it will be relatively soon.

Bottom Line for Investors

Is the stock market’s rally in the face of bad news an indication that the bear market is over and the coast is clear? Simply put, the answer to that question is no – and I expect more bouts of downside volatility before this is over.

The overarching message I want to drive home here, however, is that investors should not expect the stock market to reflect what you’re reading and seeing in economic news. The stock market does not respond to what’s happening or already happened in the economy. The stock market is forward-looking, a discounter of future economic conditions. Since 1929, the S&P 500 has bottomed an average of four months before a recession officially ends.8 If you’re waiting for good news before investing in stocks, you’re almost certain to be too late.

So instead of waiting on the news, I recommend focusing on the hard data and fundamentals. To help you do this, I am offering all readers our Just-Released May 2020 Stock Market Outlook Report.

This Special Report is packed with newly revised predictions that can help you base your next investment move on hard data. For example, you’ll discover Zacks’ view on:

- 10 trends we are seeing in a COVID economy

- How will coronavirus continue to impact the markets?

- Inside unemployment rates

- Is it time to buy U.S. stocks?

- What of US GDP growth?

- U.S. returns expectations for 2020

- What produces 2020 optimism?

- And much more.

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!9

Disclosure

2 U.S. Employment and Training Administration, Insured Unemployment Rate [IURSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/IURSA, May 4, 2020

3 U.S. Bureau of Economic Analysis, Personal Consumption Expenditures [PCE], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/PCE, May 4, 2020.

4 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

5 U.S. News, May 5, 2020. https://www.usnews.com/news/business/articles/2020-05-04/markets-drop-in-asia-on-rising-china-us-tensions-over-virus

6 The Wall Street Journal, April 30, 2020. https://www.wsj.com/articles/stock-market-surge-isnt-as-crazy-as-it-seems-11588249144?mod=djem10point

7 The Wall Street Journal, April 30, 2020. https://www.wsj.com/articles/stock-market-surge-isnt-as-crazy-as-it-seems-11588249144?mod=djem10point

8 Strategas, Quarterly Review in Charts, April 3, 2020.

9 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.