The IPO Market Is Heating Up This Summer, But Investors Should Stay Cool

The past couple of years have been relatively a quiet stretch for new public equity offerings, but that’s set to change this summer.

Readers have almost certainly encountered commentary about SpaceX and Anthropic’s expected $1+ trillion valuations, with OpenAI in the wings preparing filings as well. In fact, SpaceX’s expected $75+ billion capital raise is poised to be the largest in history—by a long shot.

This moment in economic and U.S. corporate history is no doubt fascinating. We’ve got companies launching satellites in space, with plans to colonize Mars, and enterprises developing a transformative new technology in artificial intelligence that many believe will fundamentally change the way we do business and create economic value.1

These are interesting and exciting times, which is actually the precise reason I think investors should proceed with caution.

The idea of investing early in a transformative company is one of the most attractive stories about investing. But the decision to buy can also be unduly influenced by emotion versus fundamentals. This is not to say that IPOs are universally bad investments. Some newly public companies go on to become extraordinary long-term winners. The examples I listed above could do just that.

The issue is that investors often encounter IPOs when excitement, publicity, and valuation are all peaking at the same time. SpaceX is a useful example. At an expected $1.75 trillion valuation, the stock is set to potentially start trading at nearly 100 times historical sales. That is not merely an expensive multiple, it is a multiple that assumes years of rapid growth, expanding margins, and strong execution are already on the way.

None of this is a comment on the company’s long-term potential. SpaceX may ultimately become one of the most important companies in the world, which would arguably be great for the U.S. and global economies. But investing is not just about identifying great businesses. It is about the price paid for future cash flows. A company can be exceptional and still offer a poor risk/reward tradeoff if the public-market valuation already capitalizes a decade of good news.

History supports this level of caution. University of Florida professor Jay Ritter has studied IPO performance for decades, and his data consistently show that first-day enthusiasm does not guarantee strong long-term returns. One especially relevant finding was that among sizable IPOs with more than $100 million in sales and price-to-sales ratios above 40 at the offer price, most underperformed the market over the following three years when bought at the first closing price. A price-to-sales ratio near 100 would be more than double that already elevated threshold.2

Recent IPO history tells a similar story. A Reuters analysis of the 50 highest-valued IPOs over the past five years found that investors gained an average of 27%, compared with a 53% gain for the S&P 500 over the same period, assuming access at the IPO price. Investors buying after the first-day pop generally fared worse.3 That’s one of the problems with chasing heat—by the time ordinary investors can buy, a great deal of optimism may already be reflected in the stock price. I’ll be publishing more research on this topic next week.

The broader point I want to make this week, however, is that most investors don’t need to ride the wave of one or a few companies’ transformative growth and stock performance to reach long-term goals. Why take that level of risk when we know a diversified approach to equity ownership has historically generated consistent and attractive risk-adjusted annualized returns?

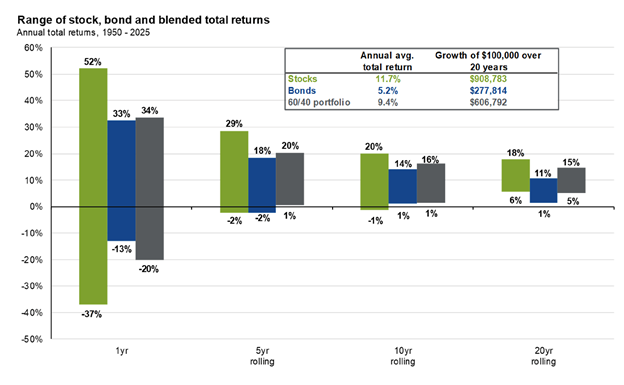

A single stock’s return profile can look like the 1-year range of outcomes in the chart below. As seen by the green bar representing the S&P 500 over the past 75 years, the range of potential outcomes went as high as +52% in a single year to as low as -37%. Diversifying to a 60/40 portfolio narrows that range of outcomes substantially, such that there was not a single 5-year period in that time with a negative return. If you zoom out to 20-year periods, the lowest annual total return for the S&P 500 was +6%. Diversification and time can generate solid returns with controlled volatility.

My overarching point is that investors do not need to identify the next great IPO to build wealth. You do not need perfect timing, special access, or a concentrated bet on the company dominating the headlines. For many investors, the path to meeting long-term goals is more likely to come from disciplined, long-term participation in broad markets—not an IPO.

Bottom Line for Investors

None of what I’ve written above is meant to discourage investors from studying new public companies and potentially investing. IPOs can introduce innovative businesses to the market, and some will become important companies in the years and perhaps decades ahead.

But the decision to invest should be based on fundamentals, valuation, risk, and fit within a portfolio, not a fear of missing out. In next week’s column, I will elaborate more on this point by digging deeper into the performance of IPOs in the very short term versus many years out.

At the end of the day, a diversified, long-term portfolio may not generate the same excitement as a headline IPO, but history suggests it offers something much more valuable, in my view: a disciplined path for building wealth over time.

Disclosure

2 Warrington College of Business. 2026. https://site.warrington.ufl.edu/ritter/ipo-data/

3 Reuters. March 25, 2026. https://www.reuters.com/legal/transactional/spacex-debut-draws-crowd-few-recent-hot-ipos-outpace-market-2026-05-26

4 J.P. Morgan. May 29, 2026. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security's U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities. An investor cannot invest directly in an index.