Is the U.S. Stock Market Rally Sustainable?

The stock market faced meaningful stress earlier this year, tied in part to the war in Iran and the surge in energy prices that followed. But the pressure didn’t last long.

As oil prices retreated, ceasefire talks advanced, and investors began looking beyond the worst-case scenarios, equities quickly recovered. But the pace of the recovery has unearthed the same question investors have been asking for years now: is this rally sustainable for much longer?

I understand the sentiment. Just about every investor probably experiences some degree of concern when stocks are near highs, because it can feel as though the market has less room to run and more room to fall.1

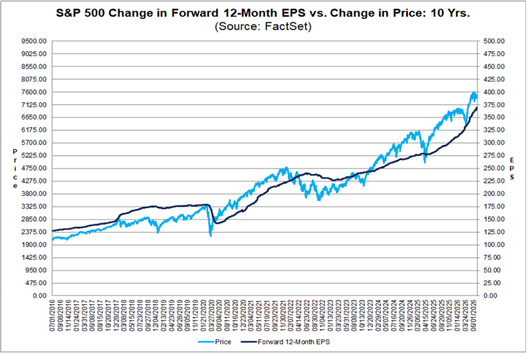

Fortunately, however, market history does not support the idea that new highs should be viewed skeptically. During long bull markets, all-time highs often lead to more all-time highs, especially when corporate earnings continue to exceed expectations. And on that front, U.S. corporations have been doing remarkably well.

To illustrate this point, the metric I’ll focus on this week is net profit margin. A company’s net profit margin measures how much profit it keeps from each dollar of revenue. If a company generates $100 in sales and keeps $15 after expenses, taxes, and other costs, its net profit margin is 15%. For the overall market, margins help investors understand whether companies are merely growing sales or actually turning those sales into bottom-line earnings.

On this metric, corporate America looks very strong, with the net profit margin for S&P 500 companies hitting 14.8% in the first quarter. That’s the highest level of profit margins in at least a decade, and in the second quarter it’s only expected to fall to 14.2%. If we reflect on the first half of the year, it’s margins that help explain the market’s resilience in the face of geopolitical, inflation, interest rate, and valuation concerns. Investors are seeing evidence that many companies have been able to protect profitability despite a difficult environment.

Contrary to many media narratives on the markets, this is not solely a technology story. Technology remains a major contributor, and AI-related infrastructure companies have delivered significant profit growth. But the margin strength has been broader than technology alone, with sectors such as financials and industrials also reporting margins above their five-year averages in the first quarter.

Of course, none of this means the rally is risk-free.

Valuations remain elevated, which means the market may have less room for disappointment. If earnings growth slows, profit margins compress, or interest rates move higher, stocks could become more vulnerable to volatility. AI-related spending is also worth watching. Some companies are earning enormous profits from the buildout, while others are spending heavily to keep pace. That balance may shift over time.

The broader point I want to make here, however, is that a market near highs is not automatically fragile. It becomes fragile when expectations rise faster than the earnings power needed to support them. In my view, expectations are currently being anchored by geopolitical and inflation concerns (amongst other concerns), while earnings continue to come in better than expected.

Bottom Line for Investors

Investors often look at a rising market and ask when it will stop. A better question is what is allowing it to rise in the first place. Right now, the answer is not just optimism or momentum, in my view. It has been the ability of companies to defend margins, grow profits, and absorb a tougher backdrop than many expected.

That being said, I’m not making the argument that investors should dismiss valuation risk or assume the market can rise uninterrupted. The more important question is whether profits continue to justify prices. For now, the earnings backdrop suggests the market’s recovery has more support than a ‘fear-of-heights’ narrative implies.

Disclosure

2 Factset. 2026.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

Questions posed are for demonstrative and informational purposes only and may not reflect the views of current clients or any one individual.