In today’s Steady Investor, we break down the forces shaping the market right now and highlight what investors should be watching next, including:

- The disconnect in U.S. manufacturing

- Business borrowing outpaces consumers

- Private credit faces scrutiny

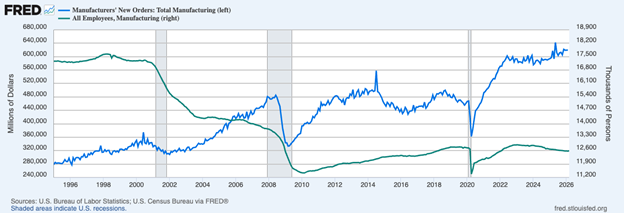

The Disconnect in U.S. Manufacturing: Jobs vs. Output – U.S. manufacturing is showing signs of life.Since early 2025, U.S. manufacturing output has risen by approximately 2.3%, with shipments climbing even faster. The U.S. is producing more of what the world currently needs, particularly in areas tied to artificial intelligence and aerospace. In fact, in several high-growth sectors, domestic production and imports are rising together, not competing. That’s a sign of growing demand and expansion, not necessarily ‘reshoring.’ Some may argue that what we’re seeing in this data is a sign that tariffs are working. But that’s not actually what’s happening. In tariff-protected industries like autos and furniture, both imports and domestic output have declined. Meanwhile, sectors aligned with long-term demand trends—semiconductors, data center infrastructure, aerospace—are seeing meaningful growth, largely independent of trade policy. Underlying economic forces and trends are driving the growth, not policy. What confuses the manufacturing revival narrative even further is the labor market. Since early 2025, manufacturing jobs have fallen by roughly 100,000, reinforcing the narrative of industrial decline. The chart below illustrates the disconnect, as readers can see steadily declining manufacturing employment (green line, right axis) versus steadily improving manufacturing output (blue line, left axis).1

Take a Closer Look at Your Strategy in Today’s Market

Growth is not moving in sync. Business investment is strong, but consumer demand is slowing, and risks are building beneath the surface. For retirees, the challenge is not just volatility. It is staying properly positioned as conditions shift.

To stay prepared, download our free guide, How Solid Is Your Retirement Strategy?2, to learn:

- The importance of flexible portfolio allocation

- Why keeping some liquid assets can potentially help you preserve more wealth

- Understanding your risk tolerance in case of a market downturn

- Plus, more strategies to help you protect your retirement assets

If you have $500,000 or more to invest, get our free guide by clicking on the link below.

Get our FREE guide: How Solid Is Your Retirement Strategy?3

More recently, employment data has begun to stabilize, suggesting the gap between jobs and output may be narrowing.But again, the driver of job stabilization would not be policy. It would be capital, innovation, and end-market demand.

Business Borrowing Is Sending a More Encouraging Signal Than Consumer Credit – With Q1 2026 earnings season underway, we’ve received insights from the first block of big companies to report: banks. One of the key takeaways we’ve seen so far in early reports is that business borrowing remains strong. Several of the largest U.S. banks reported robust commercial loan growth in the first quarter, with increases ranging from roughly 9% to over 18% year-over-year. Bank of America posted more than 12% growth in commercial loans, while Wells Fargo reported a 16.4% jump. JPMorgan Chase, the largest U.S. lender, saw its commercial loan book rise about 18% to $872.7 billion. Corporations are surely taking advantage of tight spreads, but it also indicates that quality companies are investing, strengthening their balance sheets, or both. On the other side of the ledger, however, consumer borrowing has been far more subdued. Consumer loan balances at major banks grew in the low single digits—around 3% to 4% in many cases—and in some instances were flat or declining. From a macro perspective, business lending is the more economically sensitive driver. Loans to companies typically fund capital investment, inventory builds, hiring, and expansion, all of which contribute directly to economic growth and corporate earnings. To be fair, some firms may be pulling forward financing amid uncertainty around interest rates, particularly as inflation tied to energy shocks complicates the policy outlook. Still, the scale of the increase suggests that businesses are not retreating.4

Yet Another Test for Private Credit – It’s been a challenging year for private credit, and the industry is facing yet another test. This time, it’s from the U.S. government. According to reports, the SEC has opened several enforcement investigations into large private-credit managers, while the Treasury Department and bank regulators are seeking more information on leverage, valuations, and links to the broader financial system. The scrutiny comes as investors requested to withdraw more than $20 billion from certain private-credit funds in the first quarter, though only about $11 billion was actually redeemed, highlighting both rising caution and the limits built into these semi-liquid vehicles. This story should not signal to investors that regulators see an immediate systemic crisis. But they do appear increasingly focused on a few key fault lines: how private loans are valued, whether managers are following disclosed policies, and how much exposure banks and insurers may ultimately have to the sector. One recent government estimate put bank and nonbank lending exposure to private credit at roughly $410 billion to $540 billion. For investors, this is a cautionary tale of a market built on limited transparency, infrequent pricing, and constrained liquidity, which is now being tested by slower inflows, higher withdrawals, and tougher oversight. As long as credit losses remain contained, the sector may weather the pressure. But this is a reminder that in private markets, stability can look abundant, right up until investors start asking for their money back.5

Download Our Retirement Strategy Overview Built for Today’s Markets – Markets are changing, and small missteps can have a bigger impact. Staying properly positioned is key to protecting what you’ve built.

Download our free guide, How Solid Is Your Retirement Strategy?6, for insights to help you stay on track, including:

- The importance of flexible portfolio allocation

- Why keeping some liquid assets can potentially help you preserve more wealth

- Understanding your risk tolerance in case of a market downturn

- Plus, more strategies to help you protect your retirement assets

If you have $500,000 or more to invest, get our free guide today!

Disclosure

2 Fred Economic Data. April 10, 2026. https://fred.stlouisfed.org/series/AMTMNO

3 ZIM may amend or rescind the guide “How Solid Is Your Retirement Strategy?” for any reason and at ZIM’s discretion.

4 U.S. News. April 20, 2026. https://money.usnews.com/investing/news/articles/2026-04-20/robust-us-commercial-loan-growth-eases-worries-of-economic-slowdown

5 Wall Street Journal. April 22, 2026. https://www.wsj.com/finance/regulation/u-s-officials-try-to-get-a-grip-on-risks-bubbling-inside-private-credit-31d0e199?mod=finance_lead_pos3

6 ZIM may amend or rescind the guide “How Solid Is Your Retirement Strategy?” for any reason and at ZIM’s discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

Questions posed are for demonstrative and informational purposes only and may not reflect the views of current clients or any one individual.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.