Understanding Market Behavior in Times of Conflict

As I write, the cease fire between the U.S. and Iran has been extended, as the world waits to see how peace talks and negotiations between the two countries will unfold. It is perfectly fair to say, however, that this conflict is probably far from over, and uncertainty will be the prevailing sentiment for weeks or months to come.

The stock market has been rallying anyway.

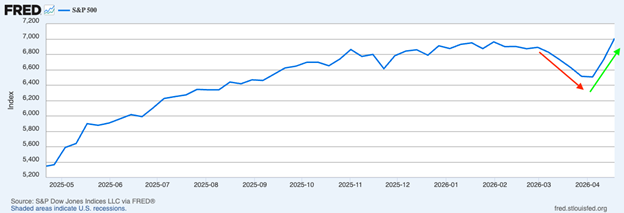

The S&P 500 is currently trading around all-time highs, having completed a “v-shaped” bounce. The strong performance comes even as several indicators are worse than they were pre-conflict. Oil prices are roughly 40% higher, the 10-year Treasury bond yield has climbed from around 3.96% to roughly 4.25%, and expectations for Federal Reserve rate cuts have largely been priced out of the market.

Don’t Miss What’s Changing Under the Surface – Download Our Latest Outlook

Stocks are climbing despite ongoing geopolitical risk. But performance is becoming more selective as rates rise and earnings expectations shift.

Our latest April Stock Market Outlook Report2 outlines what’s changing, and how investors may want to adjust. Inside, you’ll learn:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

IT’S FREE. Download our latest April Stock Market Outlook Report2

This seeming disconnect may look puzzling to some, or it may register as a sign that the markets are acting irrationally. I see it as the market behaving as it does during times of conflict.

Indeed, one of the more consistent patterns in market history is that stocks tend to bottom and begin recovering well before geopolitical conflicts are resolved. This doesn’t happen because markets can predict outcomes with certainty. It happens because markets price probabilities and expectations, and once a range of outcomes is priced in, the incremental impact of ongoing uncertainty tends to diminish over time. I think that’s what we’re seeing now.

The S&P 500 fell nearly 9% from its late-January highs in the weeks following the onset of the conflict, as worst-case scenarios were priced. Many investors shifted quickly into defensive positioning—hedging activity, reducing exposure, and making short bets. But when more information became available, and conditions stabilized even modestly, those defensive positions could unwind quickly, creating a powerful rebound driven as much by flows and positioning as by fundamentals.

The S&P 500’s “V-Shaped” Bounce in April 2026

We’ve seen this pattern throughout history. One study of past wars found that markets typically bottom roughly 10% of the way into the total duration of the conflict. Even in a prolonged event like World War II, which lasted six years, the market reached its trough roughly 10 months into the conflict.

In the current environment, we’ve seen a dramatic rise in oil prices and higher long duration interest rates. But we’ve also seen strong Q1 earnings results and rising forward earnings expectations. S&P 500 companies are now expected to grow earnings by approximately 19% in 2026, up from about 15% before the conflict began. The stock market placed a lot of immediate focus on the war in its early days, but these earnings fundamentals appear to be driving the rebound.

Periods like this also tend to bring a familiar set of narratives. Higher oil prices are often framed as unequivocally negative for markets. While they can pressure consumers and certain businesses, energy spending is still economic activity, and the U.S. economy is far less dependent on oil today than it was two decades ago. More importantly, absent a surge in money supply or broad-based demand pressures, higher energy costs tend to lead to substitution, reducing spending elsewhere, rather than fueling sustained inflation.

Even the shift in Federal Reserve expectations, from anticipating multiple rate cuts to pricing in little or no easing, is likely less consequential than it appears. Stocks have historically performed across a wide range of policy environments, and rate cuts themselves are not a prerequisite for equity gains. With the fed funds rate currently at 3.5% to 3.75%, policy is not exactly restrictive, and I’m not convinced a 25-basis point cut would move the needle very much.

The overarching takeaway here is a reminder that markets don’t wait for resolution before moving on. Investors often assume that a lack of clarity should keep stocks under pressure. But for markets, it’s more about when the range of plausible outcomes narrows, and whether the fundamental backdrop is improving or worsening. And on the latter point, investors need only look at Q1 earnings reports and transcripts to see that they’re improving.

Bottom Line for Investors

Market recoveries during periods of conflict often feel premature. It’s usually because investors are looking for improving headlines, while markets are looking for stabilization in expectations. It may feel a bit illogical, but stocks do not need resolution to resume an upward trajectory. They need conditions to stop deteriorating faster than anticipated.

I think that’s what we’re seeing here. Despite higher oil prices, higher long-term interest rates, and fewer expected Fed cuts, the market has been supported by stronger-than-expected earnings and forward estimates. The latter matters more than the former.

This is not to say that geopolitical risk can now safely be ignored, and the volatile patch related to the Iran conflict is now over. Negative surprises are always possible. But investors should keep in mind the fact that market resilience in the face of uncertainty is not unusual, and it often tells us more about expectations than complacency. As long as fundamentals hold up, stocks can move higher even while the news remains uncomfortable.

For investors, the takeaway is not to ignore uncertainty, but to better understand what the market is actually responding to.

Our latest April Stock Market Outlook Report4 breaks down the key forces shaping this environment and how to think about them going forward. Inside, you’ll learn:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

3 Fred Economic Data. April 22, 2026. https://www.wsj.com/finance/stocks/iran-war-stock-market-588f5a22?mod=finance_lead_pos5

4 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security's U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities. An investor cannot invest directly in an index.