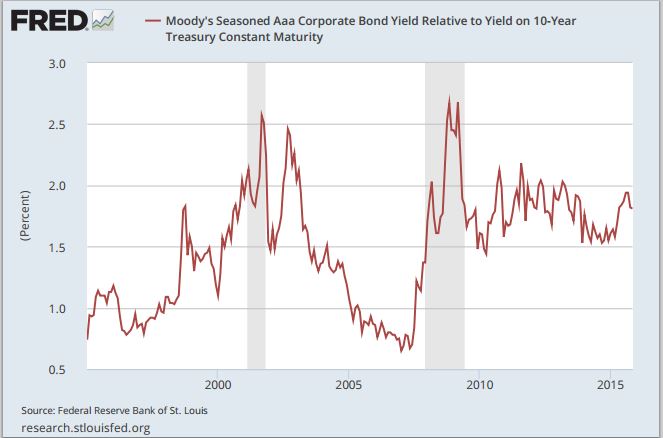

There was a tinge of nervousness in corporate debt markets toward the end of September when investment-grade companies sold just $105 billion of new debt. Sounds like a big number, but it marked a 20%+ decline from a year earlier and was the weakest September in four years (September is historically a strong month for bond issuance).

To make matters shakier, credit spreads widened over the same period that issuance fell materially. Looked at in a vacuum, it created the eerie feeling that the credit cycle might be nearing an end, which in many cases portends an economic recession.

High and Rising Credit Spreads Have Signaled Recession in the Past

October Changed the Story Line

October’s stout month in the investment grade debt markets allayed fears that might have materialized in September’s wake. Investment grade corporate debt issuance hit $103 billion, an all-time high for the month, and spreads narrowed back to attractive levels. Lower spreads mean that the market does not need a big premium over U.S. Treasuries, which implies that investors perceive a low risk of default.

Thinking about this another way, low corporate yields and spreads also imply investors are confident economic conditions are ripe for corporations to perform well. Confidence in the economy and corporate America, both quantitatively and qualitatively, is also a strong signal for confidence in equities.

Many don’t appreciate this, but it’s a unique time in the history of bond yields – both corporate and U.S. Treasuries. It’s easy to forget that there was a time in the late 1970’s and early 1980’s when double digit inflation was a concern and investment grade corporations had to pay well over 10% interest to borrow money in the capital markets.

Compare yields in the 1980’s and 1990’s with Microsoft’s October bond sale of $13 billion (in various maturities), none of which were priced at greater than 2% to comparable U.S. Treasuries. Top-tier corporations are essentially able to access capital markets for borrowed money at the risk-free rate! It’s no wonder that strong corporations are taking little issue with borrowing, even if it’s ultimately returned to shareholders in the form of share buybacks or acquisitions. The return on capital borrowed does not have to be very high at all to keep up with interest payments down the road, and I expect this to be the case going forward for some time. Borrow away.

Bottom Line for Investors

2015 is on pace to be yet another record-breaking year for corporate bond issuance. Instead of looking at it as “debt-crazed corporations”, it’s wiser to see these corporate treasurers as being opportunistic in a low interest rate environment. The fact that the market is not demanding higher premiums (as reflected through low yields) is a sign of investor confidence in steady economic growth conditions, which should lead to a favorable environment for corporations in the near to medium term.

The signal for investors here is to see the corporate bond market as an indicator for U.S. equities – the health of one generally corresponds tightly with the health of the other.

Disclosure

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. The information contained herein has been obtained from sources believed to be reliable but we do not guarantee accuracy or completeness. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.