The U.S. Economy Accelerated in the Second Half of 2023

In a remarkable defiance of consensus expectations, the U.S. economy maintained a solid pace of growth as 2023 progressed—which was the exact opposite of what nearly every economist anticipated at the beginning of the year.1

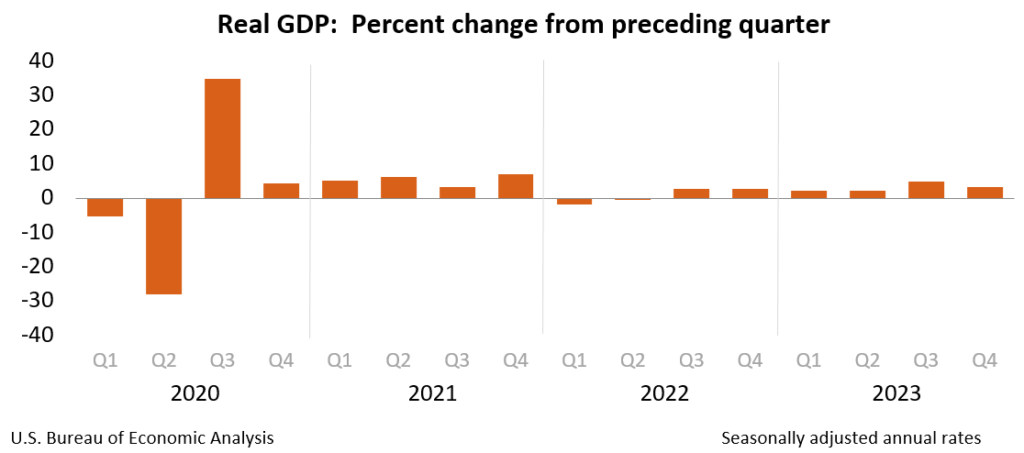

According to the Bureau of Economic Analysis “advance” estimate, U.S. real GDP grew at an annual rate of 3.3% in Q4, following a 4.9% increase in Q3. Now, to be fair, growth slowed from Q3 to Q4, and the “advance” estimate for Q4 is subject to change. But in my view, the exact data points here are less important than the high-level takeaway, which is that the U.S. economy performed better than nearly everyone expected last year.2

Learn How to Prepare Your Portfolio for Market Turbulence

Building a resilient investment portfolio is key to weathering market changes and uncertainties.

To help you do this, I recommend reading our free, just-released February 2024 Stock Market Outlook Report2. This report contains some of our key forecasts to consider such as:

• Zacks Rank S&P 500 sector picks

• Current asset allocation guidelines

• Zacks forecasts for the months ahead

• Zacks Rank industry tables

• Buy-side and sell-side consensus at a glance

• And much more!

If you have $500,000 or more to invest and want to take charge of your financial journey, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released February 2024 Stock Market Outlook4

The most prevalent concern heading into 2023 was that the U.S. economy was spiraling toward 1970s-style stagflation. Instead, we got about 2.5% full-year real GDP growth, with inflation falling from 5.5% in January 2023 to 2.6% in December 2023 (headline PCE price index). Again, virtually the exact opposite of what many feared.

There is no environment more supportive of stocks, in my view, than one where we see this level of disconnect between expectations and reality. Looking ahead, I think that means more good news for investors in 2024. Americans are still largely unhappy with the economy, and consumer sentiment has only recently rebounded from levels last seen during the 2008 Global Financial Crisis. The calls for a recession have abated, but I think we’re still far away from pessimism turning into optimism or euphoria. In other words, the wall of worry remains firmly intact.

Meanwhile, economic fundamentals within the latest batch of real GDP data look encouraging. We saw less inventory build-up and lower government spending contributions in Q4 relative to Q3. In addition, key components like consumer spending, nonresidential fixed investment (business investment), and residential fixed investment made positive contributions. Businesses spent more on intellectual property products, structures, and equipment.

In the critical consumer spending category, we saw increases across both goods and services. In the services realm, Americans traveled more, dined out, and spent more on health care. In the goods category, consumers bought more recreational goods, computer software, and pharmaceutical products. I think there’s a clear link connecting solid spending with rising wages and disposable incomes. Real disposable incomes increased 2.5% in Q4, and as seen in the chart below, wage growth continues to outpace inflation.

3-Month Moving Average of Hourly Wage Growth

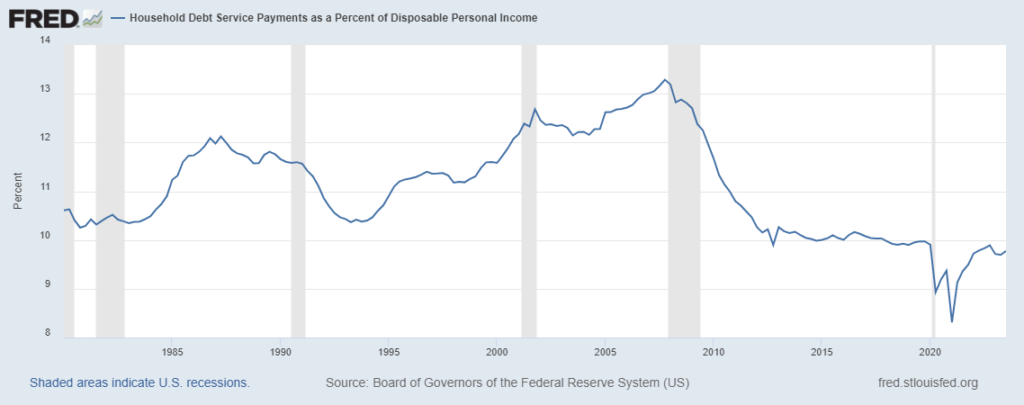

A narrative I saw appear throughout last year was that the U.S. consumer was on the brink of being “tapped out,” with stimulus savings gone and the return of student loan repayments serving as a headwind. But this story has yet to show up in the data. As referenced above, wages are growing more quickly than inflation, the unemployment rate remains below 4%, and debt service payments as a percent of disposable personal income are at multi-decade lows (chart below). You wouldn’t know it based on most media reporting and sentiment indicators, but American households are arguably better off than they have been in decades.

Bottom Line for Investors

Even though most economists have backed off of recession forecasts, expectations for economic growth in 2024 are low. This sets up a relatively low hurdle for the U.S. economy to clear, in my view, and should bolster stock prices if economic growth continues on a better-than-expected track. I see economic outperformance as a distinct possibility as businesses are coming into 2024 leaner than they were in 2023, and with an earnings rebound in the offing. And consumers simply are not as tapped out as many expect them to be. They continue to benefit from higher wages, near full employment, and softening inflation.

And I didn’t even mention rate cuts.

Beyond these factors, I urge investors to broaden their perspective and consider additional influential market forces at play. So today, I am offering all Mitch on the Market readers exclusive access to our Just-Released February 2024 Stock Market Outlook Report7.

This report looks at several factors that are producing optimism right now and contains some of our key forecasts to consider, such as:

• Zacks Rank S&P 500 sector picks

• Current asset allocation guidelines

• Zacks forecasts for the months ahead

• Zacks Rank industry tables

• Buy-side and sell-side consensus at a glance

• And much more!

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 A Wealth of Common Sense. January 26, 2024. https://awealthofcommonsense.com/2024/01/this-is-the-best-u-s-economy-since-the-1990s/

3 BEA. 2024. https://www.bea.gov/news/2024/gross-domestic-product-fourth-quarter-and-year-2023-advance-estimate

4 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

5 Fred Economic Data. January 10, 2024. https://fred.stlouisfed.org/series/FRBATLWGT3MMAUMHWGO#

6 Fred Economic Data. December 15, 2023. https://fred.stlouisfed.org/series/TDSP#

7 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI ACWI ex U.S. Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global equity opportunity set outside the U.S. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The S&P Mid Cap 400 provides investors with a benchmark for mid-sized companies. The index, which is distinct from the large-cap S&P 500, is designed to measure the performance of 400 mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment.

The S&P 500 Pure Value index is a style-concentrated index designed to track the performance of stocks that exhibit the strongest value characteristics by using a style-attractiveness-weighting scheme. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.