In a typical recession, households lose employment, disposable income levels fall or plateau, consumer spending declines, credit markets tighten up, and banks issue fewer loans. The result is that demand falls across the economy, with less money going towards goods and services.

We see the opposite happening today.

In the U.S., the unemployment rate is hovering around 5%, disposable incomes are higher, and households are sitting on roughly $1.6 trillion in savings. That’s because the pandemic was not a typical recession, nor did it trigger a credit event, a financial crisis, or damage to household balance sheets. In fact, U.S. households are largely better off today than they have been at any point in history.1

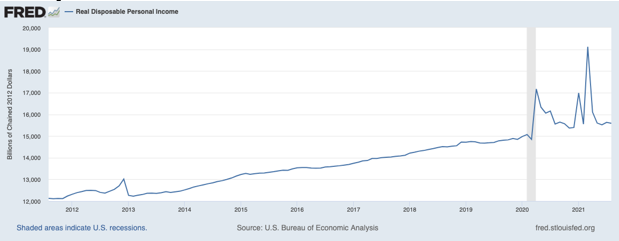

Allow me to offer a quick analysis in charts. First, real disposable incomes (adjusted for inflation) are close to $16 trillion in the U.S., which has been driven higher by direct transfers from the federal government through stimulus programs but also via higher wages. There have been many reports of labor shortages in the U.S., but it is also true that many workers are finding they can easily switch jobs for higher wages. Desperate to fill positions, many employers have been raising wages as a result. According to the Labor Department, private-sector hourly wages were up 4.6% year-over-year in September.

____________________________________________________________________________

How Long Can High Demand Last?

While high demand may mean the economy is currently in a strong position, it is still important to prepare for the long-term and for times when this may not be the case. To help you do this, I recommend focusing on key economic indicators and hard data that can positively impact your financial goals in the future.

I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- Zacks Rank S&P 500 sector picks

- Zacks view on equity markets

- What produces 2021 optimism?

- Zacks forecasts for the remainder of the year

- Zacks Rank industry tables

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released November 2021 Stock Market Outlook2

____________________________________________________________________________

Real Disposable Personal Income

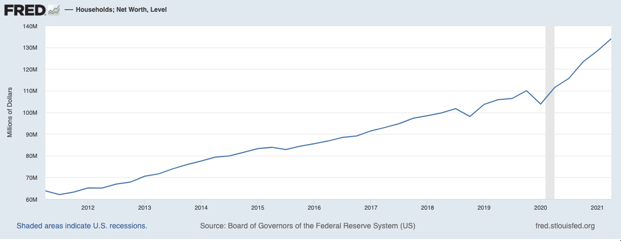

These higher wages, combined with accumulated savings, a rising stock market, and the strongest housing market in over a decade have also given way to record household net worth in the U.S.:

Household Net Worth

Put these fundamentals all together, and you have a situation where the U.S. economy has what I would call a good problem: too much demand.

In my view, the biggest driver behind snarled supply chains and shortages of goods and services is not policy failures or systemic economic issues – it’s that the U.S. and global economy simply do not have the current capacity to meet this wall of demand. And that’s a good problem.

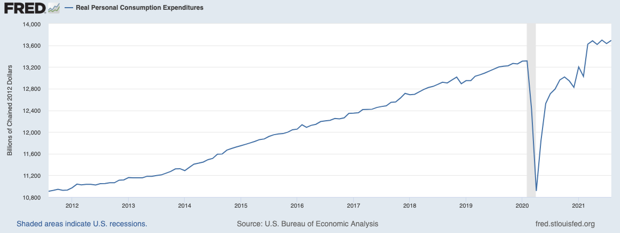

Consumers are showing few signs of slowing down. According to the Commerce Department, inflation-adjusted retail spending has soared by 14% in the last two years, which is a bigger increase than the previous seven years combined. Retail sales rose 13.9% in September from a year earlier, and sales at retail stores, restaurants, and online sellers were up nearly 1% month-over-month. The momentum favors even more spending – in the first week of October, retail spending was up 8.8% compared to the average week in September.

U.S. Consumption Expenditures: Still at or Near All-Time Highs

To be fair, the ‘good problem’ of too much demand does not automatically have a happy ending. Persistent supply chain issues could continue to drive prices higher, which could discourage spending and result in declining consumer sentiment for future quarters. The economic calculus is in determining which might happen first: inflation drives consumers away, or corporations and the global economy expand capacity and ultimately catch up to demand. In my view, it’s the latter.

Bottom Line for Investors

The U.S. consumer is in a historically strong position, and I would argue the current cash glut in the U.S. economy is a key determinant in supply chain issues. Simply stated, there is so much demand that supply can’t keep up.

In my view, this is a good problem. U.S. consumers’ financial position is not likely to change significantly in the next six months or so – if anything, it could get even better as more enter the workforce and wages continue to move higher. Meanwhile, corporations and supply chains are likely to find ways to catch up relatively soon, which should give way to sustained levels of higher spending. A good problem, with a good outcome.

Even with this positive outlook, it’s still important to prepare your assets for times when the market may not have such a good problem. We encourage investors to focus more on key data points and economic indicators that positively impact their long-term investments. To help you do this, I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- Zacks Rank S&P 500 sector picks

- Zacks view on equity markets

- What produces 2021 optimism?

- Zacks forecasts for the remainder of the year

- Zacks Rank industry tables

- Sell-side and buy-side consensus

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Fred Economic Data. October 1, 2021. https://fred.stlouisfed.org/series/DSPIC96

4 Fred Economic Data. September 23, 2021. https://fred.stlouisfed.org/series/BOGZ1FL192090005Q

5 Fred Economic Data. October 1, 2021. https://fred.stlouisfed.org/series/DSPIC96

6 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.