Growth stocks have been on a tear. Over the last 10 years (through 2020), the Russell 1000 Growth Index has delivered an annualized return of around +17%, while the Russell 1000 Value Index has annualized about +10% over the same period. Strong performance in both categories, but a clear winner in growth.

Many readers know where this outperformance is largely stemming from – technology stocks. It may surprise many readers to remember, but the first iPhone didn’t hit the market until June 2007. Netflix’s streaming service has only been around for that long, too. For many (myself included), it feels like iPhones and Netflix streaming have been around forever, but it’s really been no time at all. As smartphones became ubiquitous and consumers and businesses rapidly moved online, growth stocks widely outperformed value counterparts. It makes sense.

__________________________________________________________________________

Instead of Timing the Market, Focus on These Key Data Points

Leadership shifts frequently in the equity markets. Sometimes growth outperforms value, sometimes small beats large. But you cannot time the market or know exactly when one stock will outperform the other. So instead of getting caught up in short-term, emotional decisions, I recommend maintaining a diversified portfolio and focusing on key data points that can positively impact your investments in the long term.

To help you do this, I am offering all readers our just-released Stock Market Outlook report. This report contains some of our key forecasts to consider such as:

- S&P 500 earnings growth

- Outlook for underlying U.S. economy?

- U.S. returns expectations for 2021

- What produces 2021 optimism?

- Is it time to buy U.S. stocks?

- Update on U.S. fiscal stimulus

- And much more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released March 2021 Stock Market Outlook1

__________________________________________________________________________

But while the past decade has ushered-in strong sales, rising user growth, and big stock gains for many technology companies, it has also led to stock prices increasingly disconnected from underlying earnings. Today, there are a record number of public companies with zero or negative earnings, and many of them are technology companies trading at very high (sometimes astronomically high) P/E ratios. Many investors thought the technology surge of the late 1990s would never end, but we all know what happened then.

Indeed, since 2007, the outperformance of growth relative to value is approaching levels not seen since the 1930s and the dot com bubble. In fact, the spread between the price-to-earnings (P/E) ratio on growth and the P/E ratio on value stocks is the highest it has been since 2000, when the bubble burst on many growth names. This is not to definitively say that 2021 will be the year we see a reality check for many growth names, but in my view, it is just a matter of time before investors rotate capital away from growth and towards value.2

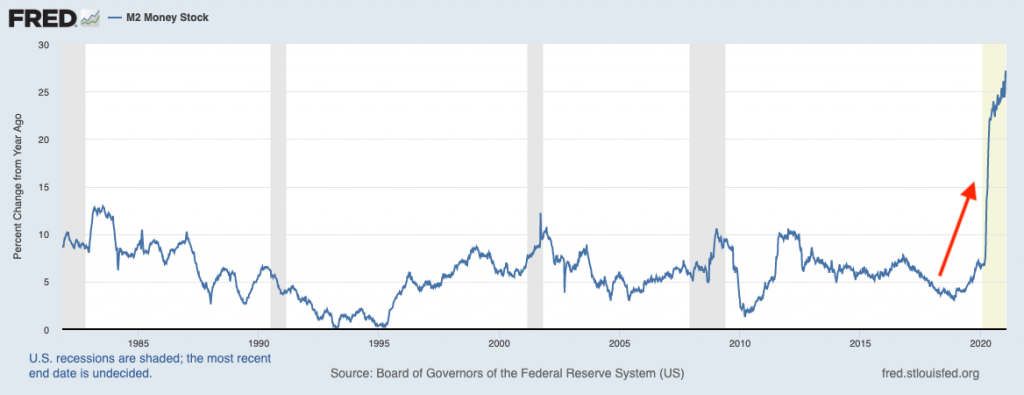

The above argument is based largely on mean reversion, but there is also the inflation factor. Over the last twelve months, the federal government and Federal Reserve have taken extraordinary measures to prop-up the economy during the crisis. Unlike in 2008/9, when fiscal and monetary stimulus largely ended up parked in bank reserves, the fiscal and monetary stimulus of 2020/1 has taken the form of direct transfers, such as stimulus payments to American families, as well as ‘PPP’ and ‘Main Street’ lending directly to businesses. The end result is that a historic amount of liquidity is sloshing around the capital markets, and M2 money supply (chart below) has risen at an unprecedented 25% year-over-year rate. This rate of change is even faster than during the inflationary period of the 1970s.3

M2 Money Supply’s Surge Could Lead to Inflation

Historically, there is a fairly tight correlation between M2 money supply and inflation. As M2 goes up, inflation usually follows. The writing for inflation is on the wall, and that’s not great for growth stocks.

Here’s why rising inflation could hurt growth stocks and help value stocks: upward inflation pressure may eventually put some pressure on the Federal Reserve to tighten monetary policy, which recent history suggests could give way to market volatility and “taper tantrums.” In my view, selling pressure in response to higher inflation and tighter monetary policy will most likely impact areas of the market with relatively high P/E ratios. This could mean a reality check for many high-flying technology and other growth names, and could trigger an investor rotation into value.

Higher expected inflation also implies upward pressure on the long end of the yield curve, as investors demand more compensation for holding longer-term bonds. To the extent inflation pressures also push up yields on the 10-year and 30-year U.S. Treasury bonds, we could see a steepening of the yield curve – a good outcome for Financials. It follows that Financials are the biggest component of the value index, and the sector has recently underperformed. In 2020, for example, the S&P 500 Financials sector delivered a return of -1.7%, while the S&P Technology sector was up +43.9%. I think the table is set for rotation.5

Bottom Line for Investors

Leadership changes hands often in the equity markets. Sometimes growth outperforms value, small beats large, foreign bests the U.S. And then the opposite becomes true for different periods. Timing each leadership change perfectly is near impossible.

So, even though I expect value stocks to have a strong run relative to growth in the medium to long-term, it does not mean I advocate shifting an investment portfolio entirely over to value. That’s the beauty of diversification – by maintaining exposure to most if not all key equity categories at all times, one can capture outperformance and limit volatility over time.

If you’re looking to increase your allocation to high-quality, value names, the Zacks Dividend Strategy actively invests in large and mid-cap value stocks with stable earnings, cash flows, and strong histories of dividend payments. It also ranks in the top 3% out of 729 managers in the Morningstar Large Cap Value Universe as of 12/30/2020.6

In addition to finding the right investment strategy, it is important in times like these not to give into emotional investing, but instead to focus on key data points and economic indicators that could impact your investments. To help you do this, I am offering all readers our Just-Released March 2021 Stock Market Outlook Report.

This report looks at several factors that are producing optimism right now and contains some of our key forecasts to consider such as:

- S&P 500 earnings growth

- Outlook for underlying U.S. economy?

- U.S. returns expectations for 2021

- What produces 2021 optimism?

- Is it time to buy U.S. stocks?

- Update on U.S. fiscal stimulus

- And much more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Forbes. November 12, 2020. https://www.forbes.com/advisor/investing/value-vs-growth-stocks-performance/

3 Fred Economic Data. February 11, 2021. https://fred.stlouisfed.org/series/M2#0

4 Fred Economic Data. February 11, 2021. https://fred.stlouisfed.org/series/M2#0

5 Strategas Quarterly Review in Charts. January 4, 2021.

6 These rankings may not be representative of any one client’s experience. In addition, they are not indicative of future performance.

7 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Returns for each strategy and the corresponding Morningstar Universe reflect the annualized returns for the periods indicated. The Morningstar Universes used for comparative analysis are constructed by Morningstar (median performance) and data is provided to Zacks by Zephyr Style Advisor. The percentile ranking for each Zacks Strategy is based on the gross comparison for Zacks Strategies vs. the indicated universe rounded up to the nearest whole percentile. Other managers included in universe by Morningstar may exhibit style drift when compared to Zacks Investment Management portfolio. Neither Zacks Investment Management nor Zacks Investment Research has any affiliation with Morningstar. Neither Zacks Investment Management nor Zacks Investment Research had any influence of the process Morningstar used to determine this ranking.

The Russell 1000 Value Index is a well-known, unmanaged index of the prices of 1000 large-company value common stocks selected by Russell. The Russell 1000 Value Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.