Why Rising Pessimism May Ultimately Be Good for Stocks

Uncertainty is running high at the moment, and it’s making investors more skittish about economic growth and the direction of markets.

I think that’s a good thing.

Investors are not wrong to be cautious. The war in Iran has pushed oil prices sharply higher and raised fresh questions about inflation. Software stocks have stumbled as investors reassess just how much future growth is already priced in. And the latest jobs data raised a few eyebrows, as U.S. nonfarm payrolls fell by 92,000 in February and the unemployment rate ticked up to 4.4%. All told, job growth has averaged just 6,000 over the past three months.

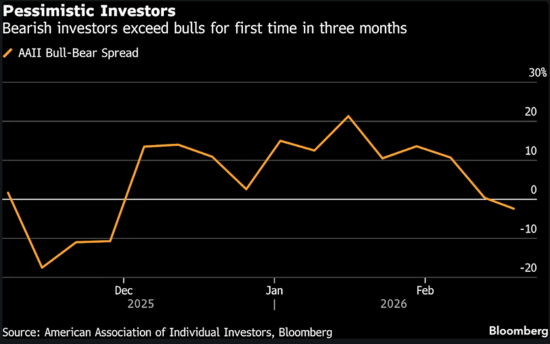

Taken together, this confluence of events has unsurprisingly resulted in rising pessimism. As seen in the chart below, bears now outnumber bulls for the first time in several months, while other measures show professional equity positioning has turned more defensive. On its face, this may seem like bad news.

But markets have proven to us time and again that they rarely rise in an atmosphere of total comfort. More often, markets move higher while investors remain skeptical and quick to focus on what could go wrong next. And in my view, that best describes the current environment.

Expectations have dropped quickly amid the flood of war headlines, meaning markets may not need especially good news to react positively. Markets only need outcomes that are less severe than investors currently fear. This is why any time you see a hint that the war may end soon, or that shipping through the Strait of Hormuz is expected to resume, oil prices plummet and stocks rally.

To be fair, we saw the flip side of that dynamic this week when the International Energy Agency (IEA) announced a record 400-million-barrel emergency release from strategic reserves, with several tankers in the Strait coming under attack the following day. Even though the IEA was adding supply, both moves were interpreted as signs that supply disruptions may be more serious and longer-lasting than previously hoped. But this reaction just gives me more conviction that investors are trading on sentiment, with consensus essentially trying to predict how bad it might get, instead of pricing based on known fundamentals and a longer-term view.

A fundamental trade in the current environment would be long, in my view. The U.S. services sector (as measured by the ISM services index) rose to 56.1 in February, its highest reading since mid-2022. New orders climbed to 58.6, 14 of 18 service industries reported growth, and export orders also improved. These numbers suggest business activity is still expanding fairly broadly.

Credit trends also look very strong. Across the developed world, loan growth is accelerating, with banks in the U.S., U.K., Eurozone, and Japan lending at the fastest pace seen in several years. I think this trend could hold for some time, given that yield curves across major developed markets are upward sloping. Banks can borrow at lower short-term rates and lend at higher long-term rates with attractive spreads. In the U.S., companies are also finding ample financing in bond markets, with investment-grade issuance topping $208 billion in January, one of the few times monthly borrowing has ever exceeded $200 billion.

To be fair, the biggest risk investors are focused on is still Iran. Namely, that the war drags on, the Strait of Hormuz stays disrupted and/or closed, and oil prices remain elevated longer than expected. This outcome would surely be impactful, as higher energy prices can pressure household budgets, push up headline inflation, and complicate the growth outlook. But it is also worth keeping the consumer impact in perspective. Gasoline is highly visible, but it makes up only about 2.9% of the CPI basket. That’s not large enough on its own to dictate the direction of the economy or stock market.

The U.S. economy is also far less vulnerable to oil shocks than it used to be. Americans consumed about 4% less gasoline in 2025 than in 2007, even as real GDP was roughly 42% larger. Energy’s share of household consumption has fallen from 5.7% to 3.7% over that span, and the shale boom has turned the U.S. into a net petroleum exporter. So while higher oil prices can still pinch consumers, they also support producers and investment in ways that were far less true in past oil shocks. I don’t mean to suggest oil can’t or won’t become a bigger problem. But I think it is fair to rule out a replay of the 1970s energy crisis and bear market, even if oil pushes past $100 and this conflict draws out for a few more weeks.

Bottom Line for Investors

Investors have good reason to stay alert. The war in Iran, higher oil prices, weakness in some high-flying stocks, and softer jobs data have all added to uncertainty, and as long as those crosscurrents remain in place, short-term volatility is likely to continue. Markets may stay choppy as investors react to each new headline on oil, shipping, inflation, and the broader growth outlook. But short-term volatility and medium-term market direction are not the same thing. Markets rarely need a calm, comfortable backdrop to move higher. In fact, some of the strongest advances occur when expectations are subdued, optimism is limited, and investors are constantly bracing for bad news. And that is what today’s setup looks like to me.

Disclosure

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.