Bank failures tend to happen in waves, with the biggest one occurring during the Great Depression. From 1930 to 1933, more than 9,000 banks failed across the country, with depositors losing some $1.3 billion (about $28 billion in today’s dollars). At the time, that was about 20% of all deposits – gone. Depositors were not made whole by the government, either. The FDIC didn’t exist.1

Deposit insurance and the FDIC came into existence in 1934, but it would take the agency the remainder of the 1930s to clean up the U.S. banking system. Between 1934 and the end of the decade, the FDIC closed about 50 banks a year, on average.

Fast forward to today, and readers may often hear that Silicon Valley Bank (SVB) and Signature Bank New York (SBNY) were the second and fourth largest bank failures in history, including all the major banks that failed during the Great Depression. With the more recent failure of First Republic Bank and ongoing pressure in the sector – namely on PacWest Bancorp – investors are rationally wondering if there’s more to this banking crisis than meets the eye.2

Some context is warranted. First, the statement that SVB and SBNY were the second and fourth biggest bank failures is only true if we do not adjust for inflation or scale the failures relative to GDP. Once we take inflation into account and also the size of the bank’s deposits relative to GDP, we find that Depression-era failures were substantially bigger.

The second factor to consider is that the most recent bank failures – at least to date – pale in comparison to previous waves of closures. As mentioned, more than 9,000 banks failed during the Depression era. During the savings-and-loan crisis that spanned much of the 1980s and early 1990s, just under 3,000 banks failed with collective assets of over $2.2 trillion. During the 2008 Global Financial Crisis, more than 500 banks were wiped out between 2007 and 2014 (this figure does not include the likes of Lehman Brothers, Bear Stearns, and others that were classified as investment banks).

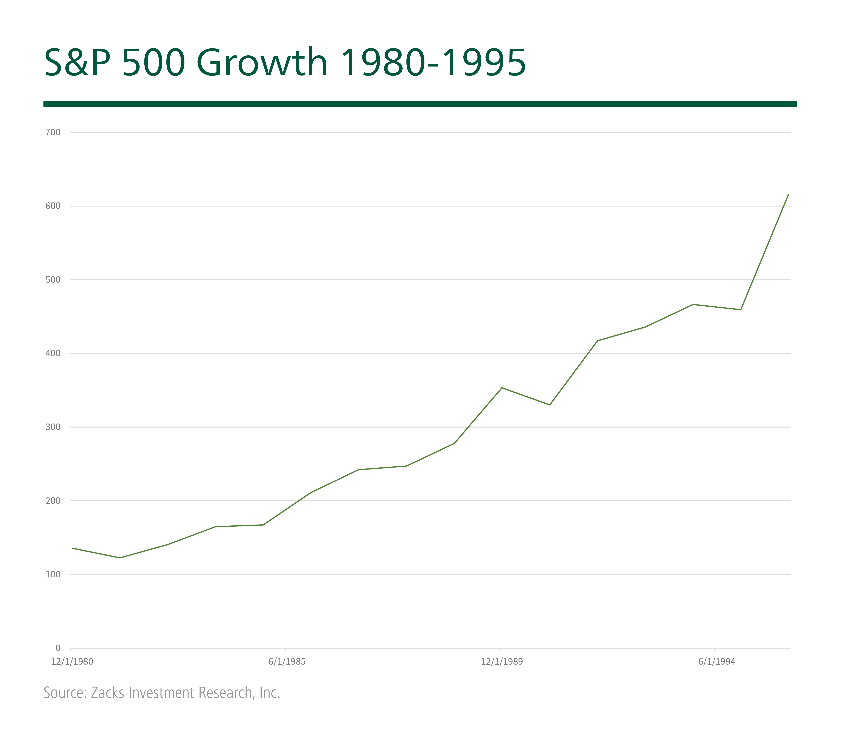

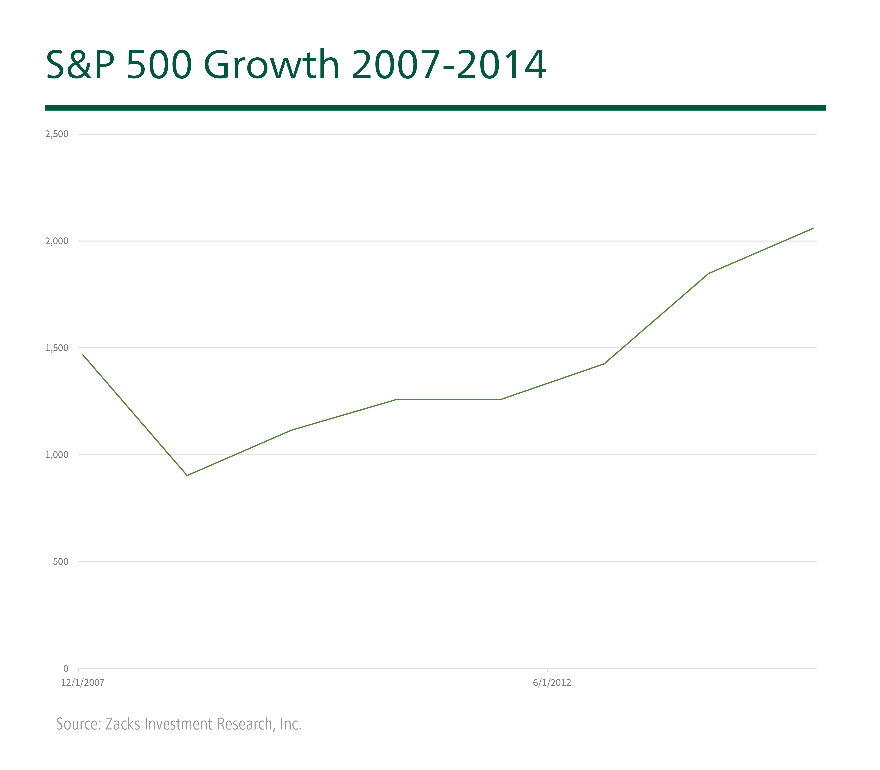

The stock market did not perform well during the Great Depression, as readers know. But then again, the economy didn’t either. The years during and after the savings-and-loan and 2008 financial crisis were different. As you can see in the performance charts for the S&P 500 below, the market overall continued to trend higher during the savings-and-loan crisis and also in the aftermath of the 2008 Global Financial Crisis. Bank failures no doubt had an impact on the economy and markets, but they didn’t drag on for years and years.

Zacks Investment Research3

Zacks Investment Research4

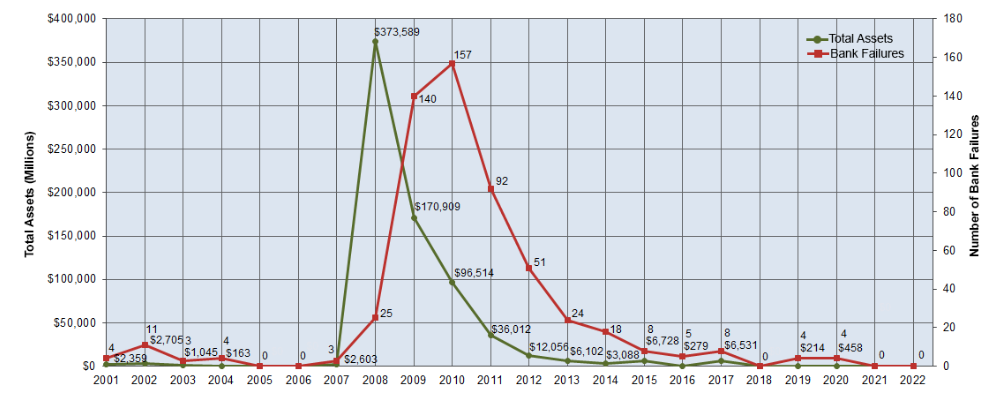

Today, the banking system is in much stronger shape than it was during those previous waves. In the two years leading up to SVB and SBNY’s closures, there weren’t any bank failures at all (chart below). From 2015 to 2020, total bank failures each year were in the single digits.

Source: FDIC5

The point here is that the high-profile failures of SVB And SBNY, in addition to the regional bank stress that continues today, may feel like a crisis that isn’t being taken seriously enough. But the other perspective—which I would argue is the equity market’s perspective—is that this string of failures is small and contained relative to what the U.S. economy has experienced historically. The fact that the market has been rising in 2023 may be telling us all we need to know about the scale of this banking ‘crisis.’

Bottom Line for Investors

Investor worries about the regional bank crisis – and its potential for economic disruption – may be entering a new chapter with PacWest Bancorp. In a security filing in early May, the bank reported losing 9.5% of its total deposits, most of which occurred on May 4 and 5 when news reports hinted at a potential sale. The stock has been pummeled.

For PacWest and other regional bank names, bond markets are demanding higher yields for regional bank bonds, and short sellers are eager to identify the next possible shoe to drop in the sector. These factors are adding additional pressure, which can easily rattle depositors and result in more failures. But considering the overall health of the U.S. banking sector and the so-far slow roll of these regional bank failures, I do not see the problem escalating the size and scale of previous waves, when hundreds and thousands of banks failed. The stock market seems to have arrived at the same conclusion.

Disclosure

2 Wall Street Journal. May 11, 2023. https://www.wsj.com/articles/pacwest-stock-sinks-25-after-disclosing-fresh-deposit-outflow-d5249168?mod=djemMoneyBeat_us

3 Zacks Investment Research.

4 Zacks Investment Research.

5 FDIC. 2023. https://www.fdic.gov/bank/historical/bank/

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI ACWI ex U.S. Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global equity opportunity set outside the U.S. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.