Another year, another showdown in the U.S. over raising the debt limit. For many readers, it may feel like we’re having the same conversations, rehashing the same talking points, and navigating the same risks on the debt ceiling as we have in past years past – a form of economic déjà vu.

Speaking from an economist and investor’s viewpoint—and also as a columnist that has covered these debt ceiling standoffs on numerous occasions over the past several years—I can confirm that the debate itself is the same. It’s the balance of power in the U.S. government that changes.

Before diving in, there is an important starting point in framing the debt ceiling issue, which is: raising the debt ceiling does not authorize Congress to initiate any new spending.1

On the contrary, raising the debt ceiling simply allows the U.S. Treasury to borrow in order to pay existing obligations. Thinking of it a different way, it would be similar to making the decision to buy a car, signing a contract to finance the purchase, and then debating several months later whether or not you should make the monthly payments. Other than Denmark—where the debt ceiling matter has yet to become a political flashpoint—no other developed country operates this way.

There is a perfectly fine and fair argument that the U.S. should have never “bought the car” in the first place, i.e., that there’s been too much borrowing and spending on programs and entitlements in recent decades. With both parties responsible for big spending programs and deficits over this period, these are conversations worth having. But the debt limit is not the arena for it – instead, lawmakers should bring the debate to the federal budget, when tax and spending levels are determined.

Regardless, in this latest installment of the debt ceiling issue, the Treasury Department has warned that the U.S. could begin missing payments as early as June 1st. Other forecasts suggest the U.S. government may have until early August. It is unclear which payments would go unpaid first, but there’s a strong indication that the Treasury could prioritize debt payments over obligations like government wages, VA benefits, Social Security, and the host of other payments owed – akin to a government shutdown, which has happened before.

Being late on—or missing—a Social Security payment or a child tax credit payment is not good, but it is also not the same thing as missing a principal payment and/or interest payment on a Treasury bond. The former is an unfortunate lapse in a government entitlement program; the latter is “default” in the true sense of the word.

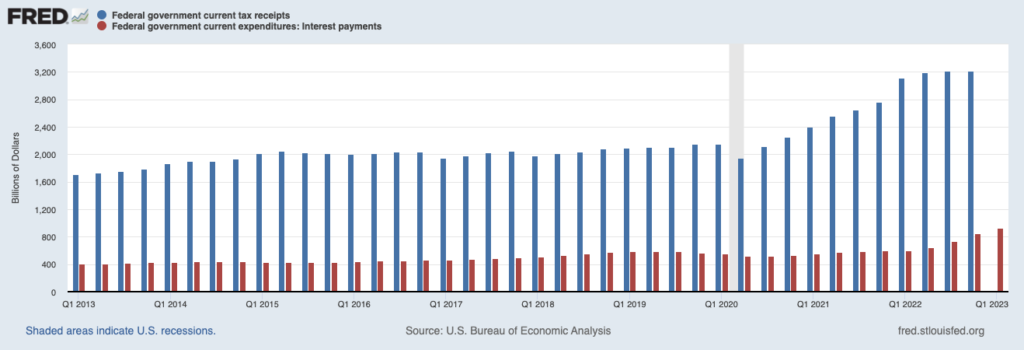

I do not think the issue of missing a debt payment is on the table for this summer, despite media reports to the contrary. For bond principal payments that come due, the U.S. Treasury is authorized to issue new debt to refinance a maturing bond—no Congressional approval needed. For interest payments, the Treasury can almost certainly prioritize these payments over the obligations described above, and they’d have plenty of cash available to do so. As seen below, current tax receipts (blue bars) are far higher than debt interest payments due (red bars), so technically speaking the Treasury could stay current on debt payments without a debt ceiling increase:

Source: Federal Reserve Bank of St. Louis2

No one can predict how the current drama will unfold. Failure to pay obligations in relation to government shutdowns has historically contributed to short-term volatility for equity markets. The 2011 “fiscal cliff” scare dragged on for long enough that Standard & Poor’s lowered the U.S.’s credit rating from AAA to AA. According to the Government Accountability Office, the lowered credit rating cost the U.S. about $1.3 billion for that fiscal year, which is small but still represents an avoidable cost. The stock market also endured a real correction in 2011, falling some -19% from the intra-year peak (though it ultimately finished flat for the calendar year and rose +13% in 2012).

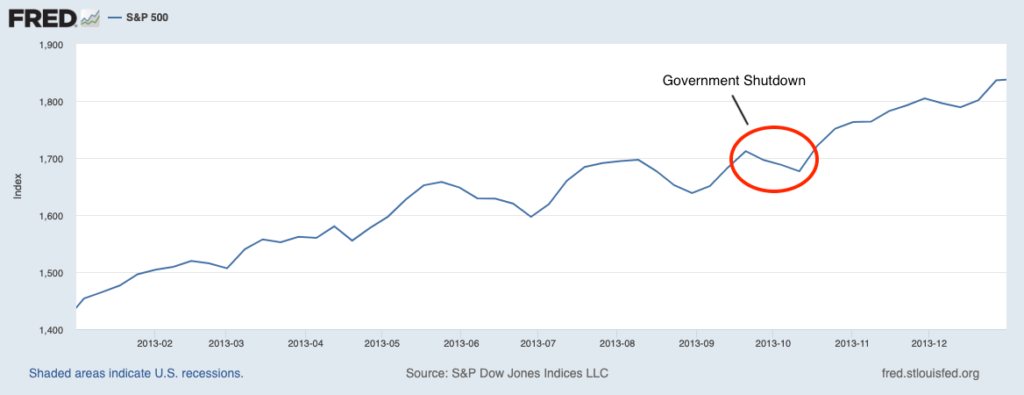

In 2013, the standoff led to a U.S. government shutdown that lasted 16 days (from October 1 to October 17). In that instance, the stock market response was far more muted. The S&P 500 pulled back slightly during the shutdown (chart below), but did not waver from its overall upward trend for the year. The index finished up +30%.

Source: Federal Reserve Bank of St. Louis3

Bottom Line for Investors

We should reasonably expect short-term volatility the longer the debt ceiling debate drags on, but I would stop short of worrying about the possibility of dire economic and financial market outcomes – which are almost always overstated. In all ‘down-to-the-wire’ government funding situations in recent years, 11th hour deals have always found a way to get done.

I would agree that politics has gotten uglier and more hostile over the years, but I do not foresee a scenario where the U.S. government would be allowed to default on its debt. Such an outcome benefits no one, and it would only serve to disrupt financial markets and raise borrowing costs – an outcome neither political party wants. History shows a willingness to bring the U.S. economy to the brink – which is unfortunate – but never over the edge. The debt ceiling has been modified over 100 times since World War II, and it will be raised again.

Disclosure

2 Fred Economic Data. March 30, 2023. https://fred.stlouisfed.org/series/W006RC1Q027SBEA#

3 Fred Economic Data. May 9, 2023. https://fred.stlouisfed.org/series/SP500

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI ACWI ex U.S. Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global equity opportunity set outside the U.S. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.