The Fed Pauses Rate Cuts, but the Bigger Story Is What Comes Next

Investors can be forgiven for missing the Federal Reserve’s most recent rate decision, which saw them holding the benchmark fed funds rate at 3.50% to 3.75%. Markets were almost universally expecting a pause, which removed any newsworthiness from the announcement.1

But that doesn’t mean the meeting was irrelevant.

Parsing through some of the Fed governors’ framings and positionings, it was clear that the Fed’s stance had shifted. In prior months, the debate had centered more on whether inflation was gradually moving back toward target. In the April meeting, the Fed appeared to be emphasizing renewed upside risks, particularly from energy. The “wait-and-see” mindset was more prevalent than it had been in recent meetings.

This distinction is notable as the Fed approaches a leadership transition. Kevin Warsh is poised to take over as Fed Chair in June, and he appears likely to bring a different framework to how the Fed operates, particularly around communication, inflation measurement, and the size of the Fed’s balance sheet. The media swirl around Warsh’s nomination may make it seem like these changes could be disruptive, but I don’t think that’s the case at all.

For starters, the Fed is not a one-person institution. A chair can shape the debate, set the tone, and guide the committee. But monetary policy is still made by a group of governors and regional Fed presidents, many of whom appear reluctant to move quickly while inflation remains above target and energy prices are rising.

That committee structure also helps explain why the more extreme concerns about Fed independence did not come to fruition. There had been worries that the Fed’s institutional structure could be disrupted or that leadership changes could alter the balance of power inside the central bank. None of that happened. Recently, the regional Fed presidents’ terms were extended, high-profile personnel changes did not materialize, and the Fed remains a committee-driven institution. For markets, the uncertainty around these somewhat political issues has all but faded, in my view.

The Fed will probably look more like business as usual, but I do foresee a gradual shift in emphasis. One area where Warsh’s views are especially important is the Fed’s balance sheet. Warsh served as a Fed governor under Ben Bernanke during the 2008 Global Financial Crisis, when the Fed dramatically expanded its use of quantitative easing. Warsh is often associated with the view that the Fed should have emergency balance-sheet powers, but that the bar for using them should be high.

The Fed’s balance sheet remains very large, at more than $6 trillion, even after several years of runoff from its pandemic-era peak. Warsh has argued in the past that the Fed’s balance sheet should be smaller, and a Warsh-led Fed may place more emphasis on reducing the central bank’s footprint in Treasury and mortgage markets. In my view, however, Warsh is likely to proceed cautiously. Balance-sheet runoff is a form of liquidity tightening. If the Fed drains reserves too quickly or reduces its holdings too abruptly, it can put upward pressure on longer-duration interest rates. That could create issues for mortgages, corporate borrowing costs, and equity valuations—none of which Warsh will want.

To offset the effects of balance sheet tightening, we may see more coordination with the U.S. Treasury and an effort to push regulatory reforms that allow banks to hold fewer reserves. Adjustments to liquidity requirements or related bank regulations could, in theory, make it easier for the Fed to operate with a smaller balance sheet. This will be the thing to watch during Warsh’s term, in my view.

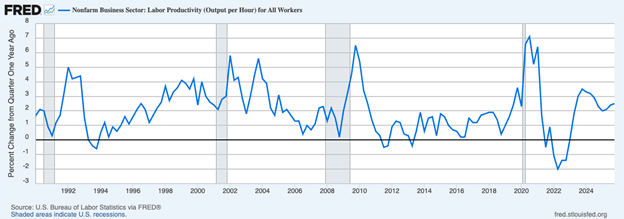

To be sure, I still think Warsh will make the case for lower interest rates. His argument will likely be that the recent oil shock is a supply-side issue, not evidence of demand-driven inflation. He may also point to improving productivity as a disinflationary force, especially if artificial intelligence and other technologies allow businesses to produce more output with fewer cost pressures. In the 1990s, stronger productivity growth helped the economy grow at a healthy pace without generating the kind of inflation that might otherwise have forced the Fed into a more restrictive stance. If productivity is rising again, which it currently is (see chart below), Warsh may argue that the Fed should not focus only on backward-looking inflation data.

U.S. Labor Productivity, % Change from Quarter 1-Year Ago

Warsh may be more inclined to look through supply-driven inflation, but the committee may not be ready to do the same. And in my view, that’s not necessarily a negative. If growth remains positive, earnings continue to expand, and inflation does not accelerate materially, stocks do not necessarily need Fed cuts to move higher.

Bottom Line for Investors

The Fed’s decision to pause rate cuts was expected, but the bigger story is the policy environment taking shape for the rest of 2026 and beyond. A Warsh-led Fed may bring a different framework to monetary policy, with more attention paid to productivity, supply-driven inflation, and the size of the Fed’s balance sheet. Worries about collapsing Fed independence or a Fed doing the bidding of the executive branch are overblown, in my view. The Fed remains a committee-driven institution, and many voting members will likely want clearer evidence that inflation is moving back toward target before easing policy. For investors, the key point right now is that markets appear to have already adjusted to the possibility of no rate cuts this year. That lowers the risk that a prolonged pause becomes a major negative surprise. In my view, the next phase of Fed policy may be less about whether the Fed cuts by 25-basis points, and more about how it manages liquidity, inflation expectations, and the long end of the yield curve.

Disclosure

2 Fred Economic Data. May 7, 2026. https://fred.stlouisfed.org/series/PRS85006091

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security's U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities. An investor cannot invest directly in an index.