For the first time, stock buybacks by companies in the S&P 500 are on track to surpass $1 trillion in a calendar year. Authorizations for buybacks had already reached $220 billion by mid-February, which firmly set the pace for this new record.1

The surge in stock buybacks marks a sharp contrast from corporate activity in the fourth quarter of 2022. Based on Q4 earnings reports from about 90% of S&P 500 companies, companies were largely using their cash to boost dividend payments to shareholders and to increase capital expenditures. Dividend payouts rose by 9% in Q4 while investment (capex) jumped by 18% year-over-year.

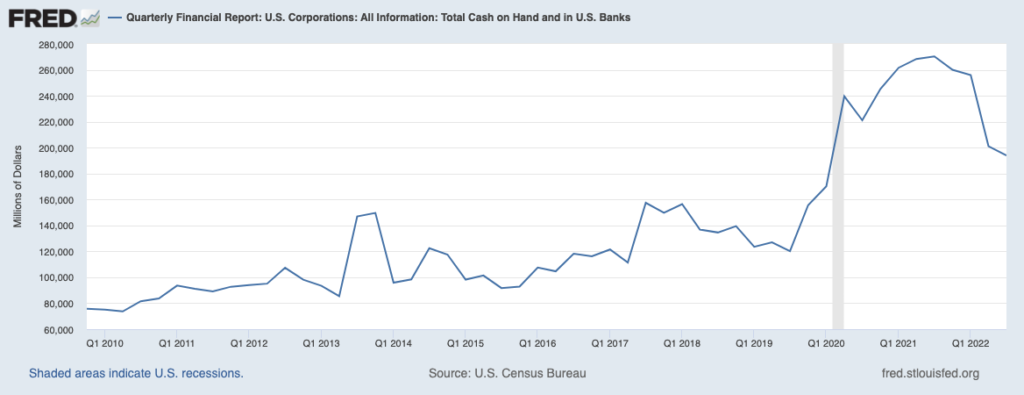

There are two observations I’d like to point out from this Q4 data. The first is that U.S. corporations are still flush with cash, as evident from the chart below showing total cash on hand and in banks:

The second observation is that companies appear to be largely unfazed by the new 1% federal tax on net stock buybacks, which took effect on January 1. We were watching closely to see if U.S. corporations would rush to pull forward share buybacks late last year in an effort to avoid the tax, but that didn’t happen. Interestingly, share buybacks fell by -18% in Q4 from the year before, but then surged in Q1 2023 once the tax had taken effect. There may be a few ways to interpret this behavior, but the bottom line is that the new tax doesn’t appear to be having an impact on corporate decision-making – a good sign, in my view.

There are three key reasons companies will opt to buy back shares, and investors should consider these when they encounter companies authorizing buyback programs (which many major U.S. companies are).

- Demonstrate confidence in the business.

When a company buys back their shares, it is often a move by management to demonstrate they are still confident in the business and its forward-looking prospects. Buying back shares when there is a significant amount of economic uncertainty and weak investor sentiment – as we’re arguably seeing now – is a way to signal strength and optimism to shareholders.

- Return capital to shareholders.

More so than any time dating back to 2017, shareholders want companies to return capital – either through buybacks or dividends. A company’s decision to authorize a share repurchase plan is in many cases a response to what shareholders are asking for.

A key feature of stock buybacks is that they do not accrue additional taxes for shareholders, unlike dividend payments which are taxed as income. In this sense, buybacks are a way to return capital to shareholders without triggering a taxable event. Companies also sometimes like using buybacks versus dividends because they can more easily adjust buyback amounts/schedules as market and economic conditions change, unlike dividends and capex which is less flexible once initiated.

- Improve earnings-per-share and potentially boost the share price.

Finally, when companies buy back their own shares, they are essentially reducing total share count – which can mean giving an instantaneous boost to earnings per share. Think about it this way: if earnings stay the same but the number of shares decreases, then EPS goes up without the company having to generate any additional net income. In Q4, less than 70% of S&P 500 companies exceeded earnings expectations, which is a low beat rate relative to history. Share buybacks can improve the EPS picture.

Buybacks can also boost a company’s share price. Since stock prices are determined by supply and demand – and share buybacks are a method for reducing supply – they inherently put upward pressure on prices. It doesn’t always work out that way, since demand is constantly changing as well, but it does provide support.

Bottom Line for Investors

Share buybacks are not always a positive or bullish sign for a company. In some cases, share buybacks can signal a company is getting desperate to prop up their stock price, which investors should heed as a warning signal. Using cash for buybacks also means having less cash available to fund operations, new investments, hiring, and so on, which can resurface as a risk later on. Investors should look at a company’s buyback plans on a case-by-case basis.

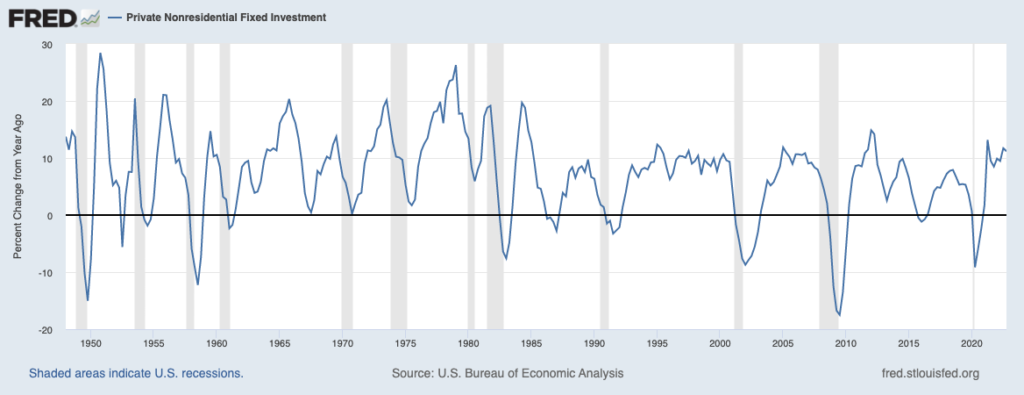

One of the largest criticisms of share buybacks is that companies should be using their extra cash to invest in new jobs and new growth, not on repurchasing shares just to potentially boost the share price and prop up EPS numbers. It’s a fair debate to have, but in my view, it does not necessarily hold water when companies are repurchasing shares and spending solid amounts on new investments. As seen in the chart below, private nonresidential fixed investment (capex) is still running at strong levels, even as buybacks gain momentum.

Disclosure

2 Fred Economic Data. December 22, 2022. https://fred.stlouisfed.org/series/QFRTCASHINFUSNO#

3 Fred Economic Data. February 23, 2023. https://fred.stlouisfed.org/series/PNFI#0

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI ACWI ex U.S. Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global equity opportunity set outside the U.S. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.