3 Crucial Insights from Q2 2023 Earnings Season

It’s possible that the Q2 2023 earnings season will be remembered as a turning point in this business cycle.

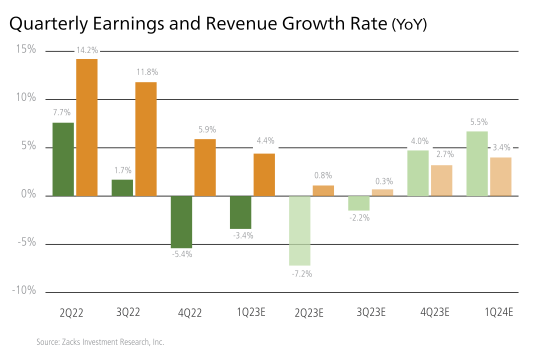

S&P 500 earnings were negative in aggregate (year-over-year) for the quarter, following a pattern we’ve seen play out since Q4 2022. But there are also emerging signs that Q2 2023 could mark a trough in the declining earnings trend, as we saw many companies and analysts shift back to a mode of positive revisions.1

Among buy and sell-side analysts, there’s debate over whether earnings will flip back to positive (year-over-year) in Q3 or Q4 2023. But a broad look at company-level and analyst estimates makes one point fairly clear: companies are positioned to earn more in the second half of the year. The question is how much more, and whether or not those earnings meet or beat expectations.2

As with any earnings season, it’s important to peel back the layers to gain a clear understanding of how companies are performing and what trends are emerging. Q2 2023’s reporting season delivered many such insights—below, I share what I thought were the three most crucial ones.

Insight #1: Earnings Were Largely Better-Than-Expected

The S&P 500 index posted a strong rally in June and July, and I think better-than-expected earnings was a key reason why.

Analyst expectations for earnings had been going up throughout reporting season, but the number of companies that exceeded sales and earnings still managed to stay high from a historical perspective. 79% of S&P 500 companies reported a positive earnings-per-share (EPS) surprise and 64% of S&P 500 companies posted a positive revenue surprise, both of which were above historical averages. That’s important.

Some may point out that the year-over-year earnings decline for the S&P 500 was a weak -4.1% in Q2, but it’s also true that the Energy and Materials sector were major drags on the aggregate figure. When stripping those two out, earnings were roughly flat. The big and notable gainer for the quarter was Consumer Discretionary, which leads into the second earnings insight.

Insight #2: U.S. Consumers are Still Holding On

The leading S&P 500 sector from an earnings perspective was Consumer Discretionary, with spending in hotels, restaurants, and leisure more than doubling from Q2 2022’s growth rate. For all the reports that consumers have spent through pandemic-era savings and were tapping out, it’s simply not showing up in the numbers yet.

The sentiment on earnings calls also indicated that management remains fairly optimistic about the U.S. consumer. We saw many reports in the travel/hospitality/restaurant segment including language indicating “improving trends,” “momentum,” and an underlying feeling of surprise at consumers’ resilience.

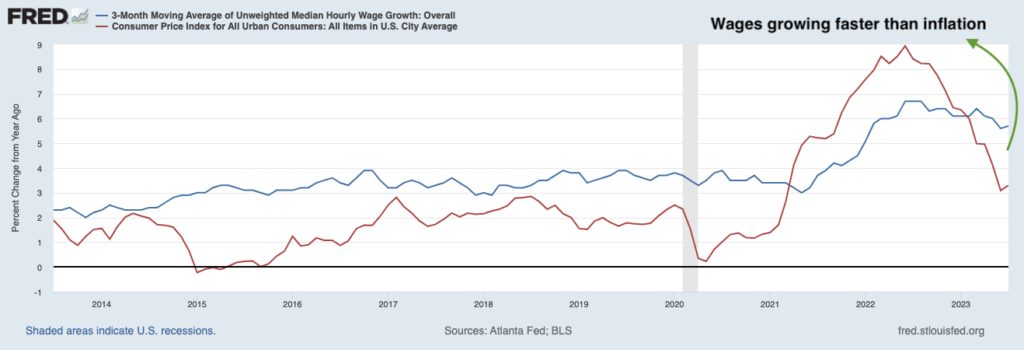

An important driver here, in my view, is that wage growth is now outpacing inflation. In the chart below, I look at the past 10 years of wage growth (3-month moving average, blue line) and inflation (consumer price index, red line). As you can see, there was a period following the pandemic when inflation was rising much faster than wages, but that’s not the case anymore. This generally means that the impact of higher prices is affecting consumers less than it was six months’ ago, which is improving purchasing power and may be driving decision-making around discretionary spending.

I do want to be cautious here, however, as neither strong wage growth nor a tight labor market are assured going forward. It’s also important to note that mortgage rates are higher, consumer credit interest rates are higher, and household debt rose to $17 trillion in Q2 (according to the New York Fed). Credit card balances have also been on the rise, and student loan payments are set to resume in October.

Insight #3: Earnings Forecasts and Recession Forecasts Don’t Align

The final insight from the Q2 2023 earnings season has to do with the second half of the year, i.e., what companies and analysts expect from S&P 500 companies going forward.

My colleagues at Zacks Investment Research see a Q3 2023 earnings decline of -1.5%, but a major caveat is that they think earnings would be positive if not for the Energy sector drag. This in my view is a signal that the earnings rebound is underway now, which again points to Q2 2023 as the trough/turning point in the cycle.

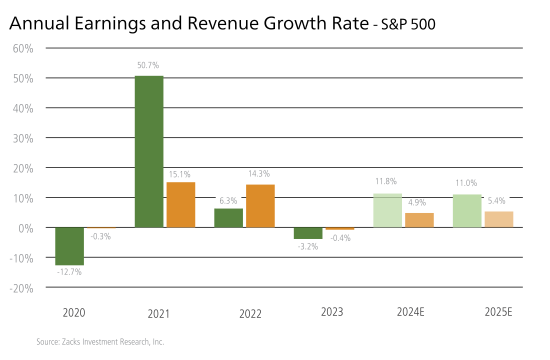

The other takeaway here is that the long-feared U.S. recession is not evident in 2023, if you take your cues from corporate earnings estimates. It’s difficult to fathom anything more than a very mild recession if earnings are trending higher, but I just don’t think it is in the cards this year. A big-picture view of corporate profitability on a long-term basis doesn’t leave much room for a recession either, as you can see in the chart below.

Bottom Line for Investors

Another important takeaway – which I think just serves to reinforce my three insights below – is that estimates for Q3 2023 are holding up quite well at the moment, i.e., nothing has transpired so far this quarter that leads analysts or company management to believe that Q3 will be weaker-than-expected.

In a typical quarter, analysts generally reduce estimates in the first two months, usually in an effort to hedge market expectations. In the past 10 years, this earnings estimate reduction has averaged -2.7%. But in Q3 2023, the opposite has been happening – estimates have been going up, which is the first time we’ve seen that since Q3 2021. And that was a very strong patch for S&P 500 earnings

Disclosure

2 Fact Set. September 1, 2023. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_090123.pdf

3 Fred Economic Data. August 9, 2023. https://fred.stlouisfed.org/series/FRBATLWGT3MMAUMHWGO#0

4 Zacks Investment Research. 2023. https://www.zacks.com/commentary/2142658/a-positive-earnings-revisions-trend-emerges

5 Zacks Investment Research. 2023. https://www.zacks.com/commentary/2142658/a-positive-earnings-revisions-trend-emerges

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.