China’s wild volatility is back. Investors were greeted in the New Year with a replay of last summer’s Chinese markets drama and big single day downswings in the first week of trading.

The source of the turmoil can be traced to two factors, both of which predictably disturbed the markets because of what they have in common: they are both examples of unwelcomed market interventions. Markets – whether they are for stocks, currencies, commodities or otherwise – like to be left alone. Volatility usually accompanies uncertainties over new regulations or a government’s intervention in the capital markets. China, unfortunately, did both of those things.

The question that logically follows in volatility’s wake is: will it spread to the broader global markets?

Will Chinese Volatility Impact Global Stocks?

It would be unfair to dismiss the effect of China’s volatility on global and U.S. stocks. The impact is real, and the volatility is contagious. But, last summer the market shook it off quickly and I think we’ll see a replay this time around again. It is easy for investors to get swept up in the emotionality of media coverage and the ‘red on the screen,’ but don’t let that drive your investment strategy. Ask yourself: has China’s episode somehow changed the outlook for U.S./global growth, inflation, corporate earnings, or interest rates? Not for us it hasn’t. The impact of this kind of rapid fire volatility is almost always short-term, and the downside ends just as quickly as it begins. Stay steady.

Let’s look at what actually happened. Two factors coincided – the first was the government’s decision to devalue the yuan by another -0.5%. In August last year, they moved it -5% and that likely triggered the quick correction we saw in the month after. The knee-jerk reaction this time was probably a “here-we-go-again” response to what looked like a desperate move from China’s government to stoke economic activity. It also caught the market by surprise, which markets loathe.

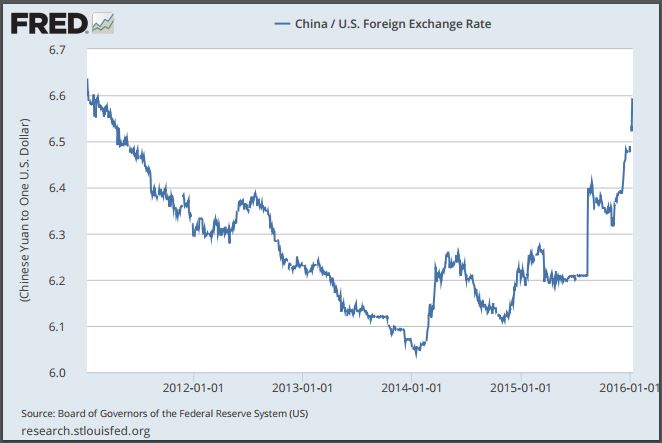

But a relative look at how China’s currency, the yuan, has traded against the U.S. dollar shows that we’re not in unchartered territory here:

China’s Currency is Actually Just Returning to 2011 Levels – Nothing Alarming

While it’s true we’d prefer China’s government to allow the exchange rate to float and for them to ‘stay out of it,’ a 0.5% move also isn’t an earth (or market) shattering event.

The second factor that aggravated markets was the implementation of so-called ‘circuit breakers’ at the turn of the year. The government created and installed circuit breakers in the markets with a design to curb a run on stocks. The idea was that the circuit breaker would kick-in and stop trading after a -5% decline, for 15 minutes. If, upon re-opening, the market fell further to -7%, trading would be shut down for the day. What a terrible idea this was! Circuit breakers ended up making the selling worse and never gave bargain hunters the chance to buy up shares and fuel a rally. The good news is that government officials saw how silly the idea was in practice and shut it down, but not before some hefty damage was done. Hopefully, they also learn to stay out of the way – the sooner China’s market trades like a normal developed market (allowing full foreign participation with substantially less oversight), the faster it will start to correlate more closely with the world.

Bottom Line for Investors

The key implication in my last sentence is that China does not currently correlate very closely with the world. China has experienced three bear markets since 2009 (the world has experienced zero) and its economy has continued to grow throughout. Bear markets with no recessions?! Welcome to China! A big part of the issue is government intervention, but there’s also the fact that China’s main stock market is essentially closed-off from foreign participation. It’s almost entirely traded by Chinese nationals who buy and sell on margin and were influenced into the market through propaganda. In that sense, the Chinese stock market isn’t a great barometer for the Chinese economy, and it’s a worse indicator for the direction of global stocks and the global economy. We think the global economy will do just fine this year and we see this China hysteria as a replay of last year. If anything, it adds a few more bricks to the wall of worry – a good thing.

Disclosure

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. The information contained herein has been obtained from sources believed to be reliable but we do not guarantee accuracy or completeness. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.