What Bank Lending Data Reveals About Risk and Opportunity in Today’s Market

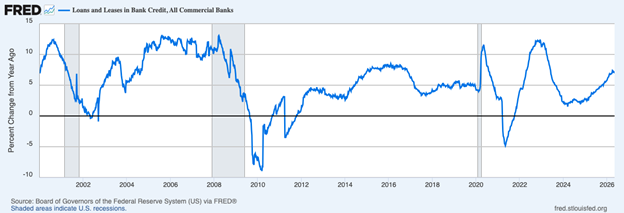

Commercial and industrial lending by U.S. banks surged 12.7% in the first quarter, the fastest pace of growth since 2022. I think there are fundamental and regulatory reasons bank lending is growing, which is what I mean by “opportunity” in today’s market. I’ll explain more below.

But the “risk” piece of the equation might be the more insightful part of the story, given that bank lending is growing as private credit is pulling back.1

Indeed, as bank lending expanded in Q1, private credit lending volumes fell 14% year-over-year. Fundraising for private credit vehicles has also fallen sharply, with new capital raised by non-listed business development companies (BDCs) down roughly 60% from a year ago. Investors also redeemed more than $15 billion from those funds during the quarter, contributing to a meaningful slowdown in new loan activity.

Commercial Lending Is Rising. What Could It Mean for Investors?

As bank lending activity accelerates and private credit markets begin to slow, investors may be seeing an important shift in today’s financial landscape.

Our latest May Stock Market Outlook Report2 explores how changing credit conditions, interest rate expectations, and evolving market leadership could impact portfolios in the months ahead. Inside, you’ll learn:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

IT’S FREE. Download our latest May Stock Market Outlook Report2

To give readers some background, private credit has become one of the fastest-growing corners of the financial system over the past decade. Private credit funds have filled a gap created by tighter post-financial crisis regulation, which made banks less willing to extend riskier corporate loans. In a relatively short period of time, private credit grew into a roughly $1.8 trillion market and has become an important source of financing for middle-market companies, leveraged buyouts, and private equity-backed transactions.

Yields from private credit vehicles have been attractive to investors in recent years, but these investments typically involve higher fees, less transparency, and more limited liquidity than traditional public securities—as I’ve written before. Shares may only be redeemable at certain intervals, withdrawals can be capped when demand is high, and reported values may not adjust as quickly as public market prices. Many investors who were not fully aware of these terms have been caught off guard recently.

There has been some chatter in financial media that cracks in private credit markets could potentially lead to contagion of some kind, or even a recession. But that’s not an argument I would make right now, especially given the bank lending data I cited above. Commercial banks dwarf the private credit market in size, with U.S. banks currently holding roughly $13.7 trillion in loans outstanding. That’s more than seven times the size of the private credit industry. Even modest increases in bank lending can therefore have a much larger impact on overall credit availability than declines in private lending volumes.

Bank Credit, % Change Year-Over-Year

Which brings me to the “opportunity” in today’s market. Banks are benefiting from modest regulatory easing that is allowing them to compete more aggressively for leveraged loans and other corporate financing opportunities. Earlier this year, the Office of the Comptroller of the Currency indicated it was open to relaxing some post-crisis leveraged lending constraints in an effort to help banks regain market share from private lenders.

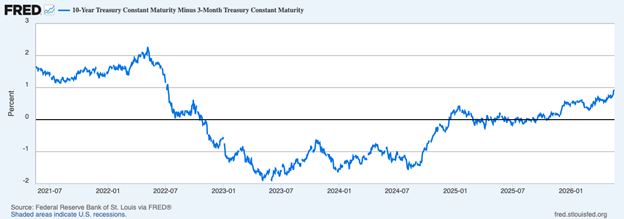

At the same time, banks may simply be in a stronger position to lend than they were in recent years. A steeper yield curve has improved lending economics, while deposit bases provide banks with cheaper funding than many private credit firms currently enjoy. In March, syndicated bank loans were being issued at spreads roughly 100 basis points lower than comparable private credit loans.

The 10-Year / 3-Month Yield Curve Has Been Steepening Over the Past 6+ Months

I would argue that this trend, if it holds, is just better for the economy and markets generally. Traditional bank lending generally operates within a more transparent and heavily regulated framework than large portions of the private credit universe. While some worry that easier lending standards could eventually encourage excessive risk-taking, the broader takeaway today is that credit continues flowing through the financial system rather than contracting.

Ultimately, it’s credit that helps fund business expansion, acquisitions, capital investment, and hiring. If one corner of the lending market slows while another accelerates, the net economic impact may be far less negative than some of the recent private credit headlines imply. In that sense, what we may be witnessing is less a deterioration in credit conditions and more a shifting balance between private lenders and traditional banks.

Bottom Line for Investors

Companies borrow to expand operations, finance acquisitions, invest in equipment, and hire workers. While we’re seeing a decline in private credit coincide with a pickup in bank lending, that may ultimately be beside the point. Credit availability—not the specific source of the loan—is often the more important driver of future business investment and economic growth.

And right now, the broader lending backdrop still appears constructive. Bank lending is accelerating, corporate default rates remain relatively contained, and businesses continue to access capital despite growing caution in parts of the private credit market.

For investors trying to navigate this evolving environment, our latest May Stock Market Outlook Report5 breaks down the market and economic trends we believe could shape the months ahead. Inside, you’ll learn:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

3 Fred Economic Data. May 15, 2026. https://fred.stlouisfed.org/series/TOTLL

4 Fred Economic Data. May 18, 2026. https://fred.stlouisfed.org/series/T10Y3M

5 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security's U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities. An investor cannot invest directly in an index.