Investors are navigating a market environment that continues to shift beneath the surface. In this week’s Steady Investor, we break down some of the biggest developments and trends investors may want to watch, including:

- Global bond yields rise

- Grid infrastructure limits AI growth

- Federal Reserve shifts toward hikes

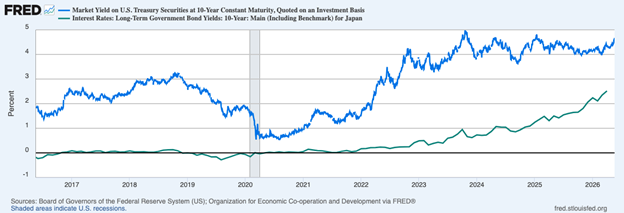

Global Bond Yields are Creeping Higher – Global bond yields moved higher this week, with the 10-year U.S. Treasury bond crossing the 4.5%—a level that in recent years has caused some consternation in equity markets. Pressure on yields has also been a global phenomenon of late. In Germany, 30-year yields reached 3.71%, the highest in 15 years, and Japan saw some of the sharpest moves with its 30-year government bond yield climbing to the highest level since the maturity was first introduced in 1999.1

U.S. and Japanese Bond Yields Have Been on the Rise

Is Your Retirement Plan Prepared for Today’s Market Environment?

Today’s financial landscape is increasingly uncertain, with inflation, market volatility, and shifting interest rate expectations creating new challenges for retirees and pre-retirees alike.

To help you plan for uncertainty, we’re offering a free Crisis-Proof Retirement Guide3. It provides practical steps for building a retirement strategy that can better withstand life’s unexpected turns, including:

- How to diversify across time, tax treatment, and income sources

- Which overlooked risks pose the greatest threat to long-term security

- How to build flexibility into your withdrawal and investment approach

- Why annual reviews are essential for staying on course

- How a research-driven advisor can help reinforce durability

- And more…

If you have $500,000+ to invest, download our free guide to discover strategies and help protect your retirement against market shocks and life’s unexpected events.

Get our FREE guide: How to Build a Retirement Plan Designed for Uncertainty3

Bond yields can rise from a number of factors, but this in case we think the market may be starting to price a longer tail to the energy shock. Since higher oil prices can feed into transportation, production, and consumer costs, bond investors tend to react quickly when energy shocks raise the risk of another inflation flare-up.But it is important to distinguish between short-term inflation pressure and a broad, lasting inflation cycle. Higher energy prices can certainly pinch consumers and businesses, but they do not automatically create persistent economy-wide inflation. For that to happen, businesses generally need enough pricing power to pass higher costs through broadly and repeatedly. Today, broad money supply growth has returned closer to pre-pandemic norms, which suggests the current environment is different from the post-Covid inflation surge.

AI’s Power Demand Is Becoming a Grid Story – U.S. data center power demand is projected to rise from 31 gigawatts in 2025 to 41 gigawatts in 2026, then to 66 gigawatts in 2027. Put differently, power demand from data centers could more than double in just two years, driven largely by the rapid buildout of AI computing capacity. The construction pipeline is significant. Planned additions are especially large in the Mid-Atlantic, Texas, and Mid-Continent power markets, but grid readiness varies widely by region. The Mid-Atlantic, Mid-Continent, and Northwest markets face elevated reliability risks because planned generation capacity may not be enough to meet rising data center demand. Texas and Georgia appear better positioned, with more new power generation capacity in the pipeline. For investors, the takeaway is that AI’s impact is extending well beyond software and semiconductors. The buildout is creating new demand across utilities, power generation, grid equipment, construction, and energy infrastructure. AI demand may be powerful, but data centers still need permits, power, labor, equipment, and grid access. In our view, that makes the next phase of the AI story less about whether demand exists, and more about whether the physical infrastructure can keep up.4

Fed Minutes Show More Openness to Rate Hikes – For much of the past two years, the Federal Reserve’s debate centered on when to cut interest rates. That conversation appears to be changing. Minutes from the Fed’s April policy meeting showed that a majority of officials believed “some policy firming” could become appropriate if inflation continued to run persistently above the central bank’s 2% target. The Fed ultimately voted to hold rates steady, but the minutes showed growing discomfort with language, suggesting the next move was still more likely to be a cut than a hike. Markets have taken note. Interest-rate futures recently priced the probability of at least one quarter-point rate increase by year-end at nearly 50%, a sharp shift from earlier expectations that cuts were the more likely next move. But there is another side to the argument. Treasury Secretary Scott Bessent has maintained that underlying inflation was declining before the Iran conflict and could resume that pattern after one or two more months of higher prices. If that proves right, incoming Fed Chair Kevin Warsh may inherit a challenging but manageable situation: near-term energy-driven inflation, but not necessarily a lasting inflation cycle, as we cited above.5

Prepare Your Retirement for the Unexpected – Market volatility, inflation, and unexpected life events can quickly disrupt even the best retirement plans.

I recommend taking a look at our free Crisis-Proof Retirement Guide6 from Zacks tax experts, which outlines strategies designed to help investors withstand uncertainty. Inside includes:

- How to diversify across time, tax treatment, and income sources

- Which overlooked risks pose the greatest threat to long-term security

- How to build flexibility into your withdrawal and investment approach

- Why annual reviews are essential for staying on course

- How a research-driven advisor can help reinforce durability

- And more…

If you have $500,000+ to invest, download our free guide to discover strategies and help protect your retirement against market shocks and life’s unexpected events.

Disclosure

2 Fred Economic Data. May 20, 2026. https://fred.stlouisfed.org/series/DGS10

3 Zacks Investment Management reserves the right to amend the terms or rescind the free How to Build a Retirement Plan Designed to Withstand Uncertainty offer at any time and for any reason at its discretion.

4 Goldman Sachs. May 20, 2026. https://www.goldmansachs.com/insights/articles/us-data-center-power-demand-projected-to-double-by-2027

5 Wall Street Journal. May 20, 2026. https://www.wsj.com/economy/central-banking/fed-minutes-reveal-support-for-rate-hikes-if-inflation-proves-persistent-97e63b1c?mod=economy_lead_story

6 Zacks Investment Management reserves the right to amend the terms or rescind the free How to Build a Retirement Plan Designed to Withstand Uncertainty offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.