The Fed’s Window for Rate Cuts Just Got Smaller

For much of the past year, the market debate has centered on when the Fed would resume cutting interest rates. The June meeting, held this week, was circled as a distinct possibility for a pivot in monetary policy with Kevin Warsh as the new chairman.

What we saw instead was a case study for why it rarely makes sense to try and predict Fed policy.

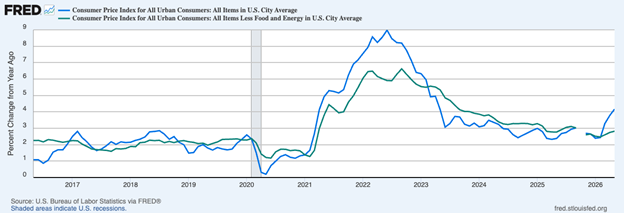

The first factor has been volatility in the inflation data. The latest Consumer Price Index (CPI) report showed headline inflation rising to 4.2% year-over-year in May, up from 3.8% in April. A CPI reading with a 4% handle makes it very difficult for the Fed to justify easing policy, even if the underlying details are more nuanced than the headline suggests (more on that below). Core CPI rose 2.9% year-over-year in May, which showed that even without the energy wild card, inflation remains well above the Fed’s 2% target.

What the Fed’s Outlook Means—and Doesn’t Mean—for Investors

The Fed’s latest projections suggest some policymakers are becoming more open to higher rates than lower ones. But does that mean rate hikes are back on the table?

Our latest Stock Market Outlook Report2 examines what’s driving inflation, what the Fed’s projections are really saying, and what it could mean for investors.

Inside, you’ll get insight into:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

IT’S FREE. Download our latest Stock Market Outlook Report2

With this data released a week prior to the Warsh’s first meeting as Fed chair, the market had essentially ruled out a rate cut. What came as more of a surprise, however, was the general sense of a shifting posture amongst Fed officials, with updated projections signaling a growing appetite for tighter policy. Nine officials now see at least one rate increaseby year-end, which is a substantial shift from earlier in the year.

But as I mention earlier in this piece, investors should avoid concluding that higher rates are a given. Fed projections change, economic data change, and market expectations change alongside them. So, even though the market sold off on the day of the Fed meeting, I really don’t see much insight to glean from it looking ahead. It’s a short-term response to a long-term unknown.

The CPI report itself shows why the picture remains complicated. Energy prices did much of the lifting in the headline number, but energy-driven inflation is not the same as broad-based inflation. For inflation to become a more serious market problem, higher energy costs would need to spread into wages, services, goods prices, inflation expectations, and corporate pricing behavior. But we haven’t seen much of that at all.

Core CPI rose only slightly on a year-over-year basis, from 2.8% to 2.9%, and on a month-to-month basis, core inflation actually cooled from 0.4% to 0.2%. Core goods inflation did not show a broad acceleration, food price increases slowed, and some services categories looked less heated than the headline number implied.

To be sure, inflation is still too high, and the Fed has little reason to make a case for monetary easing. But it also does not look like the return of an inflationary regime, like the 2021–2022 inflation environment. That inflation surge followed a sharp expansion in money supply and fiscal support, which helped fuel demand and gave consumers and businesses more capacity to absorb higher prices. Today, money supply growth is far more subdued, and consumers appear more selective and price-sensitive.

From here, investors should watch whether inflation remains concentrated or starts to spread. Core services, wage growth, inflation expectations, and corporate margins will be especially important. If energy-driven inflation begins showing up across a wider range of goods and services, the Fed may have a more serious problem. If it does not, worries that the Fed may tighten this year are probably overblown.

Bottom Line for Investors

Higher inflation coupled with the Fed’s latest projections shows that some officials are now more open to hikes than cuts. But investors should be careful not to turn that into a firm forecast.

The same lesson applies now that applied when markets were pricing-in cuts: Fed policy is difficult to predict because it depends on data that can change quickly. The more important takeaway, in my view, is that while inflation remains sticky, it is not clearly resurgent. Energy is lifting the headline number, while core inflation has not shown the kind of broad acceleration that would suggest a return to the 2021–2022 inflation regime.

Rate cuts may be off the table for now, but that does not automatically mean the Fed is headed into another aggressive tightening cycle. As long as inflation pressures remain contained and earnings hold up, markets can work through a higher-for-longer rate environment. The key is to avoid building an investment strategy around the next Fed meeting; it does not matter as much as many investors tend to think it does.

The bigger challenge is separating short-term market narratives from long-term investment fundamentals.

In our latest Stock Market Outlook Report3, we take a closer look at the themes driving markets today, why valuation still matters, and the factors investors should keep in mind moving forward.

Inside, you’ll find:

- Asset allocation guidelines for today’s market environment

- Expert forecasts for inflation, rates, and economic trends

- Industry tables and rankings to help you spot opportunities

- Buy-side and sell-side consensus insights at a glance

- And much more!

If you have $500,000 or more to invest, claim your complimentary copy of the report and see how shifting market trends could influence opportunities in the months ahead.

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

3 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security's U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities. An investor cannot invest directly in an index.