In today’s Steady Investor, we explore why gloomy economic headlines haven’t derailed the stock market and what that could mean for investors going forward, including:

- Labor market remains resilient

- Consumer debt pressures build

- Tariffs remain a key risk

Labor Market Strength in May, With Some Soft Spots Worth Noting – Jobs data for the month of May points to a labor market that is cooling in some areas, but still broadly healthy.

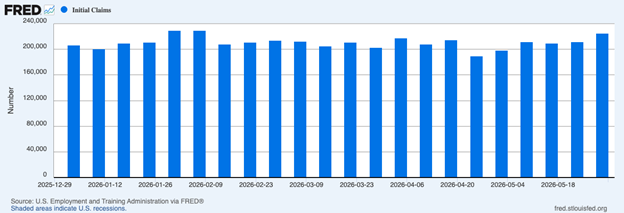

Initial jobless claims rose to 225,000 for the week ending May 30, up from 212,000 the prior week and above economist expectations. But that level remains consistent with a stable labor market, not one showing signs of widespread layoffs (see chart below of initial claims in 2026 to date). Continuing claims also held steady at 1.78 million, suggesting that workers who lose jobs are not yet struggling to find new ones in a more meaningful way.1

Initial Jobless Claims, 2026

A Clearer Way to Invest Amid the Noise

Investors are navigating a steady stream of headlines on tariffs, consumer sentiment, labor market trends, and household finances. While these developments can create uncertainty, reacting emotionally to every new data point can make it harder to stay focused on long-term goals.

Our complimentary guide, Three Steps to Overcoming Investment Behavioral Bias3, offers practical strategies to help you stay grounded and make clearer decisions. Inside, you’ll find insights, such as:

- The two main types of biases that affect investors: Cognitive and Emotional

- Specific examples of biased decision-making that can negatively impact your portfolio

- Three essential actions you can take to counteract the natural investor tendencies toward bias

If you have $500,000 or more to invest, simply click on the link below to get your copy today!

Download Zacks Guide, Three Steps to Overcoming Investment Behavioral Bias3

Private-sector hiring also remained solid in May. ADP reported that U.S. businesses added 122,000 jobs during the month, topping expectations and improving from April’s gain of 105,000. Hiring was led by education and health services, but the gains weren’t limited to one corner of the economy. Trade, transportation and utilities, construction, and financial services also held up pretty well. The softer spots in the labor market can be found in the Tech sector. Challenger, Gray & Christmas reported that U.S. employers announced 97,006 job cuts in May, with technology accounting for the largest share. AI was cited as the leading reason for job cuts for the third consecutive month, reflecting how companies are beginning to restructure around technology. But the important point for investors is that AI, at least to date, is not triggering a broad labor-market downturn. Overall job cuts are still down sharply from last year, and unemployment claims remain low by historical standards.

Credit Card Balances are Rising. Are U.S. Households in Trouble? According to the Federal Reserve Bank of New York, the share of credit-card balances at least 90 days delinquent rose to 13.12% in the first quarter, the highest level in 15 years. Total credit-card balances also stood at $1.25 trillion, up from $1.18 trillion a year earlier.Higher interest rates are one reason the pressure feels more intense. Average credit card rates have risen sharply in recent years, which means households carrying balances are paying more to service the same amount of debt. For some consumers, especially those already stretched by higher costs for food, housing, healthcare, and insurance, credit cards have become a financial pressure point.But there is an important distinction between pockets of household stress and broad economic implications. In aggregate, household balance sheets are still in much better shape than they were before the 2008 financial crisis.As seen in the chart below, debt-service costs as a percent of income remain manageable when viewed across the full economy.4

Financial Soundness Indicator: Debt Service and Principal Payments as % of Income, U.S.

Rising delinquencies can tell us where financial strain is building, but they do not automatically mean consumers are “tapped out” or that a recession is imminent.

The Tariff Story Keeps Coming Back – The Supreme Court decision striking down the IEEPA tariffs felt like the end of the tariff story for the U.S. economy. It was not. The administration is now moving to rebuild tariff policy through a different legal route, with the Office of the U.S. Trade Representative recently proposing new tariffs of at least 10% on many U.S. trading partners. The official notice cited concerns that foreign governments have not done enough to block imports tied to forced labor. The European Union, U.K., Canada, Mexico, and several other economies would face this 10% tariff, while countries including China, Japan, and India could face a 12.5% rate. Goods from Canada and Mexico that comply with the U.S.-Mexico-Canada Agreement would be exempt. The legal mechanism is Section 301 of the 1974 Trade Act, which allows the U.S. to impose duties in response to unfair trade practices that burden U.S. commerce. It is considered a more durable tool than the emergency authority the administration previously used, though legal challenges remain likely. For investors, the important point is that tariffs remain a moving variable for inflation, corporate margins, and global trade. According to the Tax Foundation, the Supreme Court ruling brought the average U.S. tariff rate down from 14.9% to 8.2%, but subsequent measures lifted it back to 11.7%.6

Three Steps to Overcoming Investor Bias – Market volatility isn’t the only challenge investors face. The constant flow of headlines, opinions, and market narratives can influence decision-making in subtle ways.

Recognizing common behavioral biases and maintaining a structured investment process can help investors stay focused on their long-term goals.

To help guide your current investing decisions, I’m offering our guide, Three Steps to Overcoming Investment Behavioral Bias7, designed to help you spot emotional traps, recognize market patterns, and respond with confidence instead of reaction. In this guide, you’ll learn:

- The two main types of biases that affect investors: Cognitive and Emotional

- Specific examples of biased decision-making that can negatively impact your portfolio

- Three essential actions you can take to counteract the natural investor tendencies toward bias

If you have $500,000 or more to invest and are ready to learn more, click on the link below to get your copy today!

Disclosure

2 Fred Economic Data. June 4, 2026. https://fred.stlouisfed.org/series/ICSA

3 Zacks Investment Management reserves the right to amend the terms or rescind the free Three Steps to Overcoming Investment Behavioral Bias offer at any time and for any reason at its discretion.

4 Wall Street Journal. May 29, 2026. https://www.wsj.com/personal-finance/credit/us-credit-card-debt-af5c7c77?mod=economy_trendingnow_article_pos1

5 Fred Economic Data. March 19, 2026. https://fred.stlouisfed.org/series/BOGZ1FL010000346Q

6 Wall Street Journal. June 3, 2026. https://www.wsj.com/economy/trade/u-s-proposes-at-least-10-tariffs-on-trading-partners-after-probe-into-forced-labor-511511f5?mod=economy_feat2_trade_pos1

7 Zacks Investment Management reserves the right to amend the terms or rescind the free Three Steps to Overcoming Investment Behavioral Bias offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable.

Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

It is not possible to invest directly in an index. Investors pursuing a strategy similar to an index may experience higher or lower returns, which will be reduced by fees and expenses.

The ICE U.S. Dollar Index measures the value of the U.S. Dollar against a basket of currencies of the top six trading partners of the United States, as measured in 1973: the Euro zone, Japan, the United Kingdom, Canada, Sweden, and Switzerland. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.