The easy monetary policies that boosted markets in 2020 and 2021 went away in 2022, with the Federal Reserve shifting from quantitative easing (QE) to quantitative tightening (QT) alongside aggressive rate hikes. Equity markets seemed to be highly responsive to Fed actions, with U.S. stocks rallying during the easy money years and declining for most of 2022 as financial conditions tightened. The “don’t fight the Fed” mantra served as a straightforward explanation for market action.

But then Q4 2022 and January 2023 happened.

In the fourth quarter, the Federal Reserve raised the benchmark fed funds rate by 75 basis points at the November meeting and by 50 basis points at the December meeting – very hawkish by historical standards. One might have expected stocks to tumble as rates kept moving higher, but they didn’t – the S&P 500 rallied by +7.4% in the three months ending December 31, 2022.

Stop Waiting on the Sidelines, It’s Time to Focus on Fundamentals!

In the current environment, many investors want to remain cautious until the Fed officially confirms it is pausing rate hikes, but I think by then it will be too late. The stock market is not likely to wait for confirmation, and I do not think investors should either.

Instead of waiting on the sidelines, I am offering all readers our just-released Stock Market Outlook report, which contains some of our key forecasts to consider such as:

- Setting U.S. return expectations for 2023

- Zacks forecasts at a glance

- What produces 2023 optimism?

- What’s alive for 2023 pessimists?

- Is it time to buy stocks?

- And more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released February 2023 Stock Market Outlook1

In January, the Fed again raised rates by 25 basis points and signaled that more hikes were coming. But the S&P 500 added another +6.18%, and U.S. small- and mid-cap stocks fared even better for the month, both rallying north of +9% as ‘risk-on’ sentiment came back into play.

In all, stocks went up close to +15% in a four-month period, while the benchmark fed funds rate rose by a stout 1.5%, and financial conditions tightened further.

The argument I’m making here is not to throw cold water on the “don’t fight the Fed” mantra. Lower interest rates increase the value of forward earnings; make capital more accessible for consumption and investing; and help drive credit, loan and economic activity. That’s good for the economy and generally great for stocks.

Tighter financial conditions and higher rates tend to work the other way, which can change investor sentiment towards risk assets and lower the multiples they’re willing to pay for them – a phenomenon we saw play out in 2022.

I agree that “don’t fight the Fed” is a useful tool in determining fundamental views of the economy and markets, but it’s also true that interest rates are not the only thing influencing business activity, consumer spending, corporate profitability, and the direction of the stock market. That’s why throughout history, there are myriad examples of interest rates marching higher while stocks also posted gains. The narrative today is basically that the Fed controls the fate of the stock market, but I do not think the relationship between the two is as tight as many are assuming.

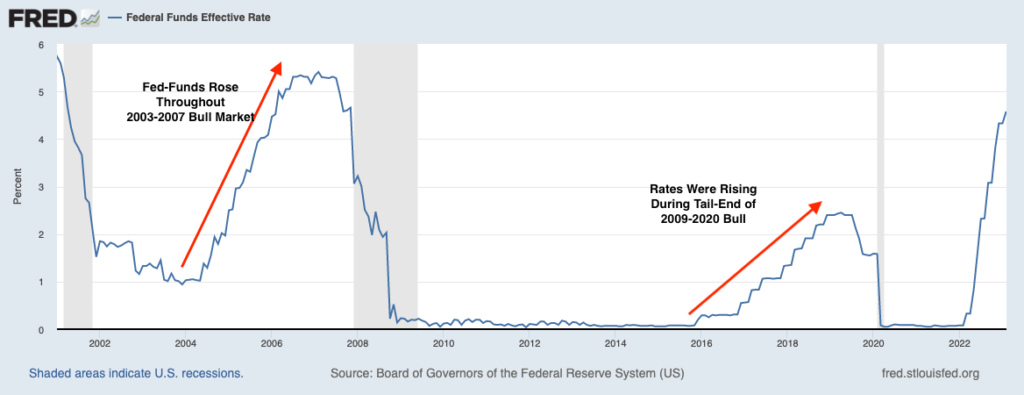

We do not have to go back very far in history to find a time when the Federal Reserve was raising interest rates and tightening financial conditions while stocks were also rising. As seen in the chart below, there was Fed hiking during the 2003-2007 bull market and again during the 2009-2020 bull market. Stocks and the economy performed very well in these periods, and ‘don’t fight the Fed didn’tplay out.

In the current environment, I’m seeing that many investors are preferring to wait until the Fed hits the pause button on rate hikes before turning bullish again. But to assume that stocks will only start to climb once the Federal Reserve cuts rates or pauses hikes is to assume that stocks move concurrently with economic news and Fed policy, which we know historically has not been the case.

Stocks are discounters of future economic and earnings conditions, which means they rarely wait for clear signals of good news to rebound. The past four months make this clear.

Bottom Line for Investors

There’s an argument that the market rally over the past four months has been in anticipation of the Fed nearing the end of the tightening cycle – a fair point. But the fact remains that stocks have rallied as fed funds have moved significantly higher, and as the Fed positions for another two, maybe three rate hikes well into the spring. Investors can hang onto “don’t fight the Fed” and remain cautious until the Fed officially confirms it is pausing rate hikes, but I think by then it will be too late. The stock market is not likely to wait for confirmation, and I don’t think investors should either.

Instead of cautiously waiting for confirmation, I recommend that investors use the fundamentals to help guide their investing decisions. I am offering our Just-Released February 2023 Stock Market Outlook Report, which will provide you with key forecasts along with additional factors to consider, such as:

- Setting U.S. return expectations for 2023

- Zacks forecasts at a glance

- What produces 2023 optimism?

- What’s alive for 2023 pessimists?

- Is it time to buy stocks?

- And more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Fred Economic Data. February 7, 2023. https://fred.stlouisfed.org/series/DFF#

3 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The MSCI ACWI ex U.S. Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global equity opportunity set outside the US. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.