In today’s Steady Investor, we dive into current news and key indicators in the market that we believe investors should consider such as:

- Global shipping market slump

- A soft patch in U.S. manufacturing

- Status of U.S. bond market rout

- Rise in U.S. treasury bond yields

A Wild Reversal in the Global Shipping Market – In late 2020 and 2021, one of the biggest economic stories involved snarled supply chains and ships lined up at major U.S. ports waiting to unload goods. A resurgence of demand following global economic lockdowns – combined with U.S. consumers armed with pandemic stimulus money – led to a crush that pushed the price of shipping a box to the U.S. from China to $15,600. Today, the price has plummeted to about $1,200. A lot has happened in a year – U.S. retailers were able to build up inventories to rebalance supply with demand, and U.S. consumers started to shift spending from goods to services. The shift has led many retailers to a glut of goods, to the point where the volumes of imports needed have fallen dramatically. With falling demand comes falling prices. Reports indicated that China’s ports have empty containers stacked six high, with dozens of idle trucks parked along the highway leading to the major terminals. Major shipping companies now fear a price war could be at hand, i.e., who can go the lowest to attract more demand. But economic data coming from China in 2023 suggests a price war may not be necessary – in February, China’s manufacturing index rose at its fastest pace in over 10 years, and export orders also climbed for the first time in nearly two years. Business confidence is also at its highest point in two years, which signals that activity in the shipping sector is likely to pick up throughout the year.1

Why You Should Avoid Market Timing

Selling in and out of the market at the wrong times is a habit of an average investor, but what would happen if you changed the cycle?

To better help you avoid acting off emotions and fear, try downloading our guide, “How Market Timing Can Affect Your Retirement Plan2”. This guide explains these behavioral traps and offers potential solutions.

If you have $500,000 or more to invest and want to learn how you may be able to avoid these mistakes today, click on the link below to get your free copy:

Download Zacks Guide, “How Market Timing Can Affect Your Retirement Plan.”2

U.S. Manufacturing Remains in a Soft Patch – Following S&P Global’s business surveys released last week, the Institute for Supply Management (ISM) has confirmed that factory activity in the U.S. remains in contractionary territory. The ISM manufacturing index measured 47.7 in February, which marked the fourth consecutive month of weak activity (any reading below 50 is contractionary). Businesses that participate in the surveys largely indicated that February’s activity reflected decisions to slow output in anticipation of weak demand in the first half of 2023, but that expectations were in place for a growth pickup in the second half. Two data points within the factory activity release are also worth noting. The first is that a measure of input prices moved above 50 for the first time since September, a cautionary sign that price pressures could be creeping higher again. The second is that February’s 47.7 print was an improvement from January’s 47.4, which may signal that manufacturing is decelerating at a slower overall pace.3

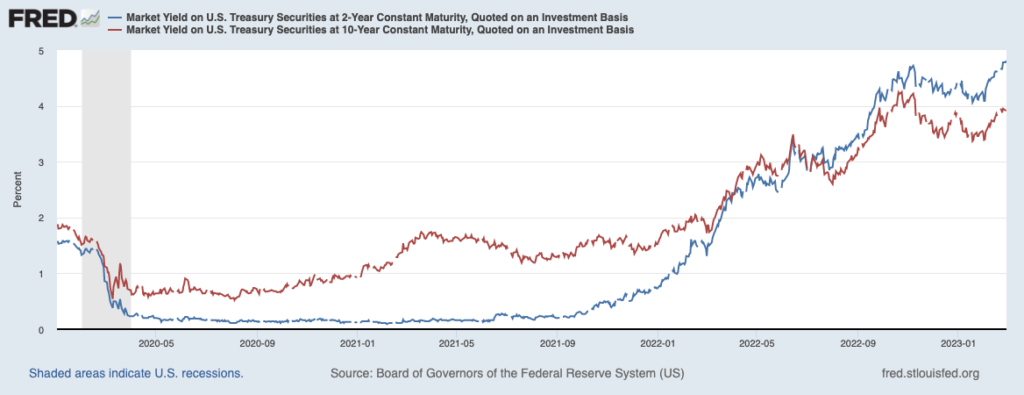

The U.S. Bond Market Rout Continued This Week – The yield on the 10-year U.S. Treasury bond crossed 4% for the first time since last November, as strong economic data and an unwavering jobs market shifted expectations about Fed policy throughout 2023. Investors are largely concerned that persistently strong economic data will give the Federal Reserve more leeway to raise rates to higher levels and perhaps keep them there for longer. Last year, investors appeared to settle on ~5% as the terminal fed funds rate in 2023, but strong economic data and signs that inflation is decelerating at a slower pace have shifted those expectations higher, which in turn has bid up yields across the Treasury yield curve. Rising yields (see chart below) have also arguably impacted the stock market, which slumped in February as yields have moved higher.4

U.S. Treasury Bond Yields Have Risen Sharply Since 2020

These factors listed above that change the state of the market could cause an investor to fall into the trap of trying to buy “at just the right time,” or sell stocks during a crisis out of fear.

Before making any big decisions, check out our guide, “How Market Timing Can Affect Your Retirement Plan.”6 This guide seeks to explain emotional and behavioral traps that investors can fall prey to and offers potential solutions to common mistakes that many self-managed investors make.

If you have $500,000 or more to invest and want to learn how you may be able to avoid these mistakes today, get your free copy by clicking on the link below:

Disclosure

2 ZIM may amend or rescind the “How Market Timing Can Affect Your Retirement Plan” guide for any reason and at ZIM’s discretion.

3 ISM Report. 2023. https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business?mod=djemRTE_h

4 Wall Street Journal. March 1, 2023. https://www.wsj.com/articles/10-year-treasury-yield-tops-4-for-first-time-since-november-d043cc?mod=djem10point

5 Fred Economic Data. February 25, 2023. https://fred.stlouisfed.org/series/DGS2#

6 ZIM may amend or rescind the “How Market Timing Can Affect Your Retirement Plan” guide for any reason and at ZIM’s discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.