Margaret E. from Conroe, TX asks: Hi Mitch, I’m seeing a new report every month about falling home sales and home prices. I purchased a house just a couple of years ago, so I have a good interest rate. But now I’m worried that home prices are going to crash like 2008, to the point where I would owe more on the house than it’s worth. What’s your take? Thank you.

Mitch’s Response:

Thank you for sending in your question! I’m sure your concerns are shared by homeowners across the country since you are right to point out that existing home sales and prices have fallen from peaks.1

In your case, however, having purchased a home a couple of years ago likely means you enjoyed rapid equity gains during the pandemic housing boom. Consider that according to the Urban Institute, total mortgage debt has risen by 15% since 2007, but home equity has risen by +131% over the same period. A meaningful portion of that equity run-up happened in 2020 and 2021.

In my view, people who bought a home in the past six months or a year may want to keep an eye on home prices relative to their outstanding mortgages, but at the same time, I think it’s prudent to have a time horizon of at least five years when buying a home. We may see more weakness in the housing markets as mortgage rates went from 3% at the beginning of 2022 to north of 6% now, but over time I think supply and demand dynamics support higher prices in housing.

How Reactive Are You to a Volatile Market?

Every investor tends to react differently to market downturns and volatility, but there is no right or wrong level of risk tolerance!

To help investors understand their reactions to market volatility to help future decision-making in the market, I am inviting you to take our new Market Volatility Quiz2.

In less than two minutes, you will get a better understanding of:

• How closely you watch market movements

• What level of volatility will prompt you to take action

• Your comfort level with your current asset allocation in relation to today’s market

If you have $500,000 or more to invest and want to get answers to the questions above, click on the link below to take our newest quiz today!

Take Our Market Volatility Quiz2

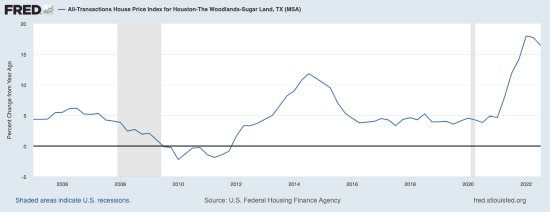

More specifically to your situation, I was able to pull home price data from the Houston area, which you can see below. Assuming that you purchased your home sometime in 2020, you likely captured solid equity gains in your first two years, whereby a pullback is happening from high levels.

Home Price Index for the Houston Area (Year-Over-Year % Change)

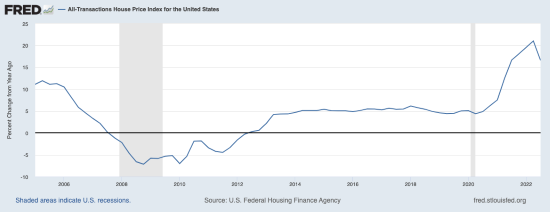

Home Price Index for the U.S. (Year-Over-Year % Change)

I think ongoing strength in the U.S. jobs market is likely to make any economic weakness in 2023 fairly mild, with a shallow recession a possibility. I would not expect anything close to the recession experienced in 2008-2009. But another reason I do not think housing is headed for a crash is that lending standards are now far more stringent than they were in the early 2000s.

A big driver of the housing crash that started in 2005 was that many mortgages were approved with little-to-no scrutiny of borrowers’ income, in some cases providing financing to people without seeing so much as a previous year’s W-2.

In the current market, obtaining a loan requires borrowers to provide an exhaustive accounting of income, liquid assets, liabilities, and other information needed to ensure the debt can be repaid. Additionally, the days of banks creating pools of risky mortgages and trading them as securities are largely over, with few of those securities in existence today. Given the runup in prices and high down payments, CoreLogic estimates that housing prices would have to fall between 40% and 45% to put the same percentage of people underwater on their mortgage as there were in the aftermath of the 2008 Global Financial Crisis.

We may see some more downside pressure on housing prices from here, but I think the U.S. economy and markets will prove more resilient than many expect. As long as you have a reasonably long-time horizon to be in your home (5-10 years minimum), I would not worry too much.

To help your future decision-making process in the market, I recommend taking a look at your investing habits when volatility occurs. I am inviting you to take our new Market Volatility Quiz5, which will help you get a better understanding of:

• How closely you watch market movements

• What level of volatility will prompt you to take action

• Your comfort level with your current asset allocation in relation to today’s market

If you have $500,000 or more to invest and want to get answers to the questions above, click on the link below to take our newest quiz today!

Disclosure

2 ZIM may amend or rescind the quiz “How Reactive Are You to a Volatile Market?” for any reason and at ZIM’s discretion.

3 Fred Economic Data. November 29, 2022. https://fred.stlouisfed.org/series/ATNHPIUS26420Q#

4 Fred Economic Data. November 4, 2022. https://fred.stlouisfed.org/series/USSTHPI#

5 ZIM may amend or rescind the quiz “How Reactive Are You to a Volatile Market?” for any reason and at ZIM’s discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.