U.S. GDP contracted at an annual rate of -1.6% in Q1 2022, and according to the latest GDPNow estimates from the Atlanta Fed, the economy contracted another -2.1% in Q2. The Atlanta Fed’s GDPNow tool is not known for precise accuracy, but all signs point to two consecutive quarters of negative growth – the technical definition of a recession.1

If this data holds up and hindsight confirms a recession in the first half of 2022, it would be vastly different from the past 12 recessions the country has experienced since World War II. In every postwar recession, economic output fell while unemployment went up.

But that’s not what is happening now.

______________________________________________________________________________

Recession Worries? Protect Your Investments in the Meantime!

Whether or not data confirms that we are already in a recession, I advise that investors take control of their investments right away. No matter the state of the market – you should be prepared financially!

There have always been factors (such as high inflation and unemployment) that have heavily shifted the market in the past, but over time there has also been a positive return. So, instead of focusing on short-term choices, I am offering all readers our just-released Stock Market Outlook report that contains some of our key forecasts to consider such as:

- U.S. Macro Outlook

- What fundamentals are U.S. stock markets pricing in with ‘22 and ‘23?

- What of U.S. GDP Growth?

- Zacks forecasts for the remainder of the year

- Zacks rank S&P 500 sector picks

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released July 2022 Stock Market Outlook2

________________________________________________________________________

Over the past six months, the unemployment rate has fallen from 4% to 3.6%, and demand for workers in the private sector remains strong. There is a good argument that the jobs market today is more robust than it was before the pandemic. In the years before the Covid-19 outbreak – when the economy was largely considered to be in great shape – there were an average of 1.7 million Americans collecting federal unemployment benefits. Today, that figure stands at 1.3 million. For context, during the 2008 Financial Crisis, there were over 6.5 million unemployed Americans receiving benefits.

The decline in output appears to be tied to households and businesses altering spending and investing plans based on shifting supply, demand, and price dynamics. Companies are struggling to manage inventories while consumers are grappling with rising prices. But it’s also true that households are experiencing gainful employment and higher wages, while businesses overall want to retain or hire employees – not fire them. There have been over 10 million open jobs in the U.S. every month of 2022, which is nearly double the number of typical job openings in years before the pandemic.

Household finances also remain historically strong. At the end of Q1 2022, Federal Reserve data shows households had $18.5 trillion in cash in checking accounts, savings accounts, and money market funds. Before the pandemic, that figure was $13.3 trillion.

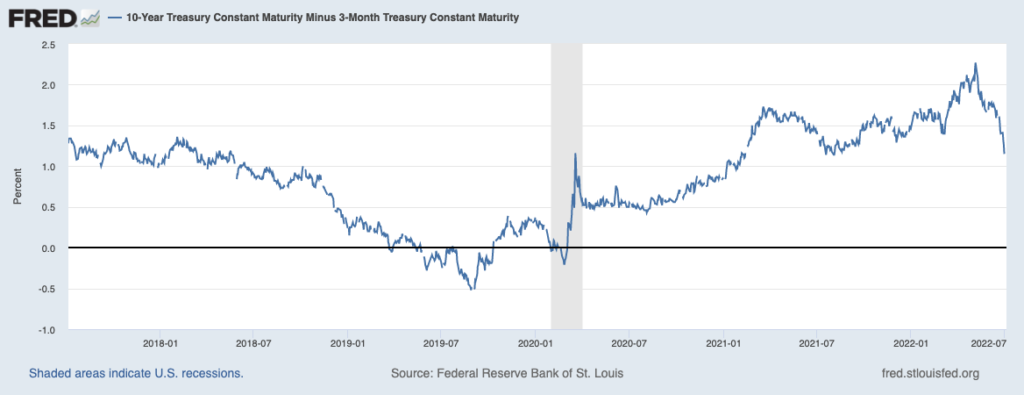

Banks are also not showing any signs of duress. The latest round of Fed ‘stress tests’ found that banks could easily handle the unemployment rate soaring to 10% and a collapse in the stock market and commercial real estate that would wipe out over $600 billion. Even with those unlikely shocks, banks would have capital ratios of 9.7%, which is over double the 4.5% required by law. An upward sloping yield curve also suggests that banks can lend profitably in the current environment:

In my view, a technical recession in the first half of 2022 should not be taken as a sign that the economy is collapsing. Inflation pressures have certainly introduced headwinds that are altering consumer behavior and fundamentally slowing growth trends. But there are also major adjustments happening at the business and fiscal level that have muddied the GDP calculation but do not necessarily signal plummeting demand.

In Q1, for instance, surging imports subtracted from the GDP print even though many businesses were importing more goods in response to strong consumer demand. The overlooked metric is total trade, which went up solidly in Q1 with imports rising 11.5% and exports rising 7.2%. Inventories were also a major drag in Q1, as businesses stocked up in Q4 and pulled back substantially in Q1. And finally, as expected, government spending fell at a -2.7% annualized pace in Q1, which subtracted -0.48% from the headline GDP figure. These are not the types of fundamentals that worry me about the economy.

Bottom Line for Investors

Historically, recessions are best characterized by a marked decline in production and output, a rupture in the credit markets and household finances, and a significant amount of job loss. So far, we’re only seeing one of these conditions (decline in output), which I think is more tied to the ongoing pandemic and war-related adjustments in business and consumer behavior – not to a systemic crisis.

To be fair, U.S. consumers started to pull back in Q2, which is a metric that should be watched closely going forward. Rising producer prices could also start to squeeze historically high corporate profit margins in the second half, which is where we might start to see more hiring freezes or even layoffs. These are the fundamentals to watch going forward, but I think the setup is tilted far in favor of experiencing a positive surprise, not a negative one.

During this time of uncertainty, I recommend that investors continue to protect their investments by focusing on key data points. To help you do this and be better prepared for any market outcome, I am offering all readers our Just-Released July 2022 Stock Market Outlook Report, which contains key forecasts, such as:

- U.S. Macro Outlook

- What fundamentals are U.S. stock markets pricing in with ‘22 and ‘23?

- What of U.S. GDP Growth?

- Zacks forecasts for the remainder of the year

- Zacks rank S&P 500 sector picks

- And much more

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

3 Fred Economic Data. July 5, 2022. https://fred.stlouisfed.org/series/T10Y3M#

4 Zacks Investment Management reserves the right to amend the terms or rescind the free Stock Market Outlook offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.