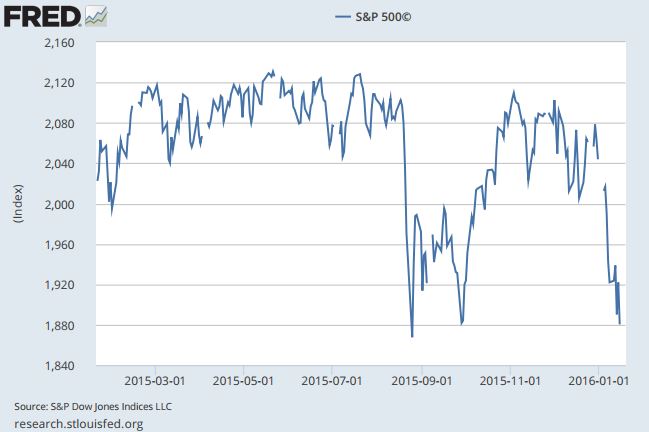

The market abruptly slipped into correction territory to start the year charting a virtual free fall from its December 29th level.

The S&P 500 is Retesting Correction Lows

Any relief gained from market rallies has been rendered obsolete in these first few weeks. The selling pressures have been fairly relentless and investors seem to be more spooked than ever about where the market is headed. A large portion of the emails and calls I’m getting are understandably worrisome in nature, wondering if it’s time to steer the ship away from equities for some time.

Corrections are Common but Never Easy

Corrections (drops in the 10% – 20% range) are normal, natural occurrences within bull market cycles. Plain and simple. In fact, since 1980 the market has suffered an average intra-year decline of -14.2%. Think about that… -14.2%! Nobody wants to experience that type of decline, but it’s almost always been a part of the investment experience. It comes with the territory. For patient investors, though, positive rewards also come with the territory – in 27 of the 36 years, since 1980, the market finished positive.

To be sure, the knowledge that pullbacks are frequent and normal does not make enduring them any easier. Investors dislike losses more than twice as much as they enjoy gains, so to see a drop in the value of a nest egg is gut-wrenching. I understand that completely. To make matters worse, corrections are almost always sharp, scary declines accompanied by what seems like catastrophic news. In this case, the potentially huge fallout from a slowing China and falling oil prices.

But, both of those are old stories – re-runs from fears we saw emerge throughout the last year. Neither of them should have the power to outright reverse the economic and earnings growth we expect this year. In fact, lower oil prices should ultimately help more sectors than it hurts – it just takes some time for the benefits to flow through.

The Single Most Important Feature of a Market Correction

Everything I’ve written above you’ve read before in some form. I’ve consistently made my views clear that I think we are still within a bull market cycle and that I see any pullbacks as temporary disruptions. But, in the context of the current downside volatility, I want you to think about it from another angle: if you were to come to me and ask, “Mitch, when would you say is the very best time to invest in equities? My answer would be that, in my experience, the best time to buy stocks is when economic fundamentals are strong and earnings are growing, but no one notices because fear dominates the headlines. Sound familiar?

If I see red all over the screen, notice an uptick in client calls and find that CNBC is non-stop calling for doomsday – yet nothing has changed with the fundamental outlook for the U.S. or global economy (which we still expect to see grow in 2016) – it makes me even more bullish. The ‘wall of worry’ grows when market activity and investor sentiment divorce themselves from the fundamentals, and that’s precisely what we are seeing now.

So, with that all being said, what is the single most important feature of market corrections? It’s that, by definition, corrections are short, sharp declines in the market that tend to emerge from redundant fears not associated with earnings and economic fundamentals. Call me crazy, but that is exactly what I see right now.

Bottom Line for Investors

Looking back on my personal history as an asset manager, I cannot show you a single time when market volatility didn’t cause clients to worry and want to change their asset allocations. In 1998 the market fell 19% mid-year because of the Long Term Capital Management implosion, yet the market finished up 27%. In 2010 and 2011 the market dropped sharply (-16% and -19%, respectively) on account of fears over the European sovereign debt crisis, yet the bull market pressed-on. History gives us dozens and dozens of similar examples, and in every single one there are investors who give-in to the fear-inducing headlines and abandon their long-term approach. We think a similar action in this environment would be the wrong course of action.

Of course, I can’t say with certainty that the bull market will work its way through this downside volatility. No one can ever forecast the direction of the market with certainty. But I also cannot imagine anyone convincing me to be bearish in the midst of a sudden and sharp decline when fears are dominating headlines and yet the fundamental outlook for growth, earnings, inflation, and interest rates remain favorable. That, to me, is about as far from bearish as it gets.

Disclosure

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. The information contained herein has been obtained from sources believed to be reliable but we do not guarantee accuracy or completeness. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.