Another year, another debt ceiling showdown.

Some investors and readers may feel like it’s Groundhog Day with headlines of “catastrophic” consequences if the U.S. government fails to pay its bills. And let me be clear: I agree that failure to pay interest and/or principal on Treasury bonds would have severe economic and market consequences.

I just don’t think the U.S. will get there.

The debt limit was created in 1917 and has been raised over 100 times, with numerous instances where a political standoff made its fate unclear. Some would say the current political environment makes a negative outcome more likely with both parties dug into their respective positions – a fair point. But even the most extreme form of brinkmanship would not likely result in the U.S. defaulting on debt, which has never happened in history.1

One widely under-reported reason is that a debt default is unconstitutional, as per the Supreme Court’s 1935 interpretation of the 14th Amendment’s Public Debt Clause. “The validity of the public debt of the United States…shall not be questioned,” the Supreme Court wrote in a ruling, which has long been interpreted as meaning that default is simply not an option.2

Download Our Exclusive Stock Market Outlook Report

While there are a lot of uncertainties impacting the market like inflation, debt, and more, focusing too much on these fears and uncertainties could negatively impact your investments.

Instead of focusing on worrisome headlines, it’s better to focus on the facts and data when it comes to making future decisions! To help you do this, I am offering all readers our just-released Stock Market Outlook report.

This report will provide you with insights to consider such as:

- Setting U.S. return expectations for 2023

- Zacks forecasts at a glance

- What produces 2023 optimism?

- What’s alive for 2023 pessimists?

- Is it time to buy stocks?

- And more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

IT’S FREE. Download the Just-Released February 2023 Stock Market Outlook3

But another source of confusion in the debt ceiling debate is: what constitutes a “default?” This is a point the media – and even Treasury Secretaries – often deliberately fail to explain clearly.

In the media, there are obvious advantages to skipping the technical, granular, boring details of how the debt ceiling and bond principal and interest payments work. It’s easier to just say that failing to raise the debt ceiling automatically triggers a default, which is not the case.

As for government communications, the acting Treasury Secretary – in this case Janet Yellen – almost always resorts to conflating government obligations, like Social Security payments or government worker wages, with defaulting on U.S. debt. Just last week, Treasury Secretary Yellen said, “A failure on the part of the United States to meet any obligation, whether it’s to debtholders, to members of our military or Social Security recipients, is effectively a default.” Ms. Yellen had to use the word “effectively” in her statement because the actual definition of default singularly means failing to pay interest or principal on U.S. Treasuries.

Being late on—or missing—a Social Security payment or a child tax credit payment is not the same thing as missing a principal payment and/or interest payment on a Treasury bond. The former is an unfortunate lapse in a government entitlement program; the latter is “default” in the true sense of the word.

A little-known fact is that the last time the debt ceiling issue came to a head, in 2011, the Federal Reserve and Treasury officials privately made a plan to make on-time payments on Treasury debt while delaying payment on other government bills. A review of Fed transcripts at the time makes it clear that while the rhetoric almost always focuses on default – likely an attempt to influence public opinion and exert political pressure – behind the scenes government officials were ensuring a default would never happen. Markets understand this point.

The actual risk of not raising the debt ceiling would be missing entitlement payments and payments to other government programs—which, again, is not the same thing as defaulting on debt. Missing entitlement payments is not good, and a lapse can weigh heavily on sentiment, credibility, and potential markets. But Congress’s failure to act would not necessarily trigger an actual default or credit event in financial markets, as is often framed in the media.

A natural follow-up question is, how can the Federal Reserve and U.S. Treasury keep making on-time principal and interest payments without a raised debt ceiling? It happens in two ways. For bond principal payments that come due, the U.S. Treasury is authorized to issue new debt to refinance a maturing bond—no Congressional approval needed.

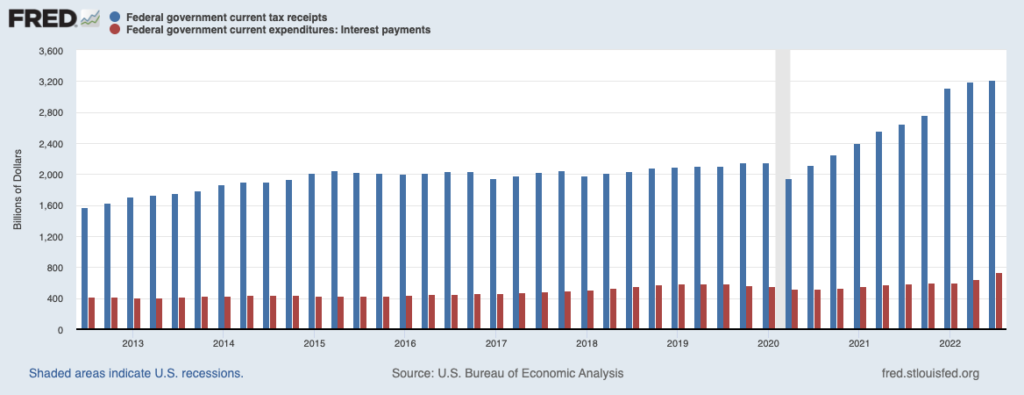

For bond interest payments due, the Treasury receives far more in monthly tax receipts than it owes in monthly interest payments. As of the end of fiscal 2022, interest payments due on U.S. Treasuries accounted for just 9.7% of total tax revenue. This is akin to making $10,000/month in salary and having a $970/month mortgage payment, which would of course be easily manageable.

The U.S. Treasury Receives Enough in Paid Taxes (blue bars) to Cover Interest Payments on Debt (red bars)

Bottom Line for Investors

In my view, markets have seen enough debt ceiling standoffs – especially in recent years – to be able to price in some of the likely outcomes. According to the Treasury Department, there are enough funds available to pay all government obligations (Social Security, wages, etc.) and payments due to bondholders until June, even without the debt ceiling being raised. This runway may mean we’ll have to spend months hearing about debt ceiling infighting in Congress, but it may also mean the actual threat of missing obligations is low assuming Congress can work out a deal in that time. For reasons explained above, it’s these obligations that investors should weigh from a market’s standpoint, not a default.

To better protect your investments in this market, I am offering all readers our Just-Released February 2023 Stock Market Outlook Report. This report will provide you with key forecasts along with additional factors to consider, such as:

- Setting U.S. return expectations for 2023

- Zacks forecasts at a glance

- What produces 2023 optimism?

- What’s alive for 2023 pessimists?

- Is it time to buy stocks?

- And more…

If you have $500,000 or more to invest and want to learn more about these forecasts, click on the link below to get your free report today!

Disclosure

2 Wall Street Journal. January 24, 2023. https://www.wsj.com/articles/janet-yellen-takes-measures-to-ease-debt-ceiling-woes-11674581734?mod=hp_listb_pos4

3 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

4 Fred Economic Data. December 22, 2022. https://fred.stlouisfed.org/series/W006RC1Q027SBEA#0

5 Zacks Investment Management reserves the right to amend the terms or rescind the free-Stock Market Outlook Report offer at any time and for any reason at its discretion.

DISCLOSURE

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly blue-chip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.

The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell. The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaq-listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index is a modified market capitalization weighted index composed of preferred stock and securities that are functionally equivalent to preferred stock including, but not limited to, depositary preferred securities, perpetual subordinated debt and certain securities issued by banks and other financial institutions that are eligible for capital treatment with respect to such instruments akin to that received for issuance of straight preferred stock. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.